From the doom loop to an economy for work not wealth

In spite of suffering the longest pay decline in modern history, the government and Bank of England are issuing calls for pay restraint, and workers are being told once more that they must be poorer still. Yet since austerity policies began wealth has expanded relentlessly. The economy and pay are in an unending doom loop of decline.

- TUC analysis published today shows that in 2023 the economy has lost around £400 billion of GDP compared with a projection of the forecast made by the OBR in 2010.

- Comparing with a projection from ahead of the global financial crisis, the loss forecast for 2027 approaches £900 billion or one third.

But austerity policies are only symptomatic of a model that has for more than 40 years put the interests of wealth ahead of work. On this longer view, comparing with pre-1979 trends:

- GDP has fallen short by £2 trillion or nearly half, but

- wealth (household net worth, adjusted for inflation) has gained £7 trillion and nearly trebled.

This paper outlines an alternative model to reset the balance in favour of work and away from wealth. These policies have a substantial international dimension, given inequalities and failures of work are no less apparent between countries as well as within them.

- North American and Europe account for only 10 per cent of the world population but 57 per cent of global wealth.

Kristalina Georgieva, IMF managing director, recognised in 2020 ‘A New Bretton Woods Moment’, and recalled the end of the Second World War and “the foundations for a more peaceful and prosperous post-war world”.1 These foundations were well laid:

- Ahead of 1979 (from 1948) more vigorous gains in UK GDP of 3.1 per cent a year were set against greatly more moderate gains in wealth of 1.8 per cent a year.

But over recent decades these foundations have been badly undermined. With too much emphasis on wealth, the performance of the economy has progressively deteriorated. Workers have lost out badly, and there is a sense of permanent financial instability.

This paper draws on the recent ‘New macroeconomics’ literature, that in turn recalls the historic contributions of J. A. Hobson (1858-1940) and J. M. Keynes (1883-1946). These emphasise the relation between a too high return to wealth and too low return to work, and theories of over-production and underconsumption. Rather than deficient supply the underlying problem of the world economy is excessive supply in the context of deficient demand. This situation translates in practice to a balance sheet inflation, with the counterpart to high household net worth likely excessive private debt. As the IMF and others recognise, this is vital context for the actions of central banks – but is ignored in practice.

But crisis should not be inevitable. Clement Attlee’s government effected the necessary rebalancing, and built a social infrastructure that endured to 2010. The call is to restore the global foundations for a labour internationalism, and in the UK to repair the infrastructure of the past and build a new green infrastructure for the future.

“But if we are going to sustain our public services and avoid a doom loop of ever higher taxes and ever lower dynamism, we need economic growth”,

- Jeremy Hunt, Autumn Statement speech, 17 Nov. 2022

“This government has forced our economy into a doom loop – where low growth leads to higher taxes, lower investment, squeezed wages, and the running down of public services. All of which hit growth again”,

- Rachel Reeves, response to Autumn Statement, 17 Nov. 2022

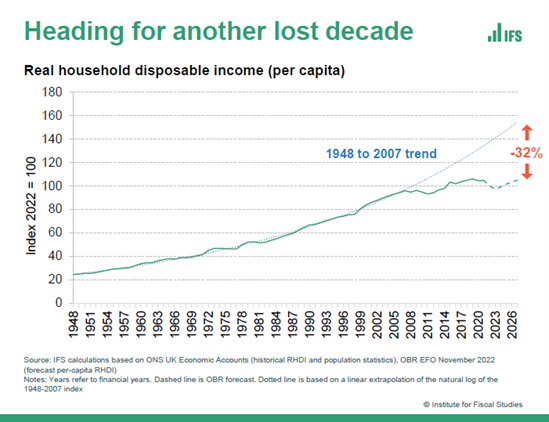

After the Autumn Statement the Institute for Fiscal Studies (IFS) reported that in 2027 real incomes per head of the population will be a third smaller than had they followed the post-war trajectory.1

- 1 Xiaowei Xu's slides, #3: https://ifs.org.uk/collections/autumn-statement-2022

In their commentary they commend the government for confronting “harsh fiscal realities”, but still warn of “reaping the costs of a long-term failure to grow the economy, the effects of population ageing, and high levels of past borrowing”.

According to the ‘doom loop’ argument, the vast erosion of around a third of the UK economy and the arrested standard of life for workers is a consequence of austerity policies in place since 2010. Inherent to these policies are critical and wrongheaded assumptions that are common across the institutional infrastructure of macroeconomic policy, both on a national and international level (though the international institutions have sometimes moderated their stance). These assumptions concern multipliers and the effects on capacity / the output-gap.

With these mechanisms identified, the lost prosperity can be restored. However to move forward decisively, outcomes need to be understood on a longer horizon, and on a broader view of policy beyond fiscal policy.

IFS-type metrics can be used to set present outcomes in a longer-run context, and confront dislocations in the economy that are fundamentally distributional in substance. Just as over the austerity period dire outcomes for GDP and work have been set against immense gains to wealth, the same divergence can be traced further back to 1979. Over the past 40 years economic activity has fallen short by almost half compared to pre-1979 trajectories, but wealth has expanded by almost three times. On this view the austerity decade is an episode in an arrangement of the economy that for decades has supported wealth not work.

The sections two to six therefore examine the doom loop and consequences for the economy and public finances since the global financial crisis in 2007-08. Sections seven to eleven address the failure on the longer view, and rehearse theoretical arguments and the associated policy infrastructure that might explain how the economy ahead of 1979 operated better for work and since 1979 has operated better for wealth.

Much of the broader argument turns on how the returns to work and wealth translates (to the good) to spending power and production, and (to the bad) to debt and speculative activity. Immediately the imperative is for increased spending power, when instead incomes are undermined on several fronts by high inflation, sharply higher interest rates and inadequate support from government. Moreover there must be concerns about the sustainability of the now extreme dislocation between asset values and the size of the economy. Signs of stress in markets with an element of speculation like technology companies and residential and commercial property may indicate a ‘correction’ is now underway that could mean a greatly more severe recession than presently admitted by policymakers. In a candid moment the IMF conceded “the level of risk we are flagging at the moment is the highest outside acute crisis”.2

.

Crisis or not there is a desperate need to reset the economy to give priority to production and work, and to heed calls heard in the wake of the pandemic for a return to the Bretton Woods mindset at the end of the Second World War.3

.

This imperative operates on both the domestic and international domains. For the dislocations evident at country level are potentially more extreme between countries. The ideal behind the Bretton Woods Agreement was to permit all countries the ability to set full employment polices, as well as to provide development aid to enable low-income countries better to catch up. With these inequalities now in front place in climate discourse, the whole approach of the post-war world merits re-examination

- 2 Press briefing for the Global Financial Stability Review, October 2022: https://www.youtube.com/watch?v=vSqSsMNv4Z8

- 3 In October 2020 Kristalina Georgieva, the managing director of the IMF, urged “… inspiration from a previous generation. William Beveridge, a former LSE Director, issued his famous report in 1942, which led to the creation of the UK’s National Health Service. And in 1944, John Maynard Keynes and Harry Dexter White led the establishment of the Bretton Woods system—including the IMF and the World Bank”: ‘The Long Ascent: confronting the crisis and building a more resilient economy’, 6 Oct. 2020 at the London School of Economics and Political Science: https://www.lse.ac.uk/lse-player?id=f40f2957-251e-4272-9b63-634a83f40ce5

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox