Lessons from a decade of failed austerity

The view that the economy is at capacity not only constrains government expenditure, but also means periodic attempts to withdraw monetary stimulus. Governor Carney acknowledged earlier this year that central banks are torn between a ‘business’ and ‘financial’ view of the world.[1] At a global level, efforts to tighten policy (increase rates and withdraw QE) follow according to preconceived ideas of real capacity. The repeated abandoning of these efforts indicates the dominance of ‘financial’ constraints, more specifically constraints arising from high levels of indebtedness. At the time of writing (summer 2019), central banks have shelved 2018 plans to tighten monetary policy and are set for an increasingly expansionary policy, following collapsing asset markets and signs of fragility in the global economy.

The importance to crisis of debt inflation rather than (or as well as) price inflation is now widely recognised. The Bank of England observe “Countries that underwent sharp credit booms have often experienced a crisis”.[2] In 2008 this build-up of debt – with most emphasising mortgage debt – caused the global financial system to implode and led to the most severe global recession since the great depression in the 1930s. Since the crisis the instigation of ‘macroprudential regulation’ has been aimed at containing future financial excess.

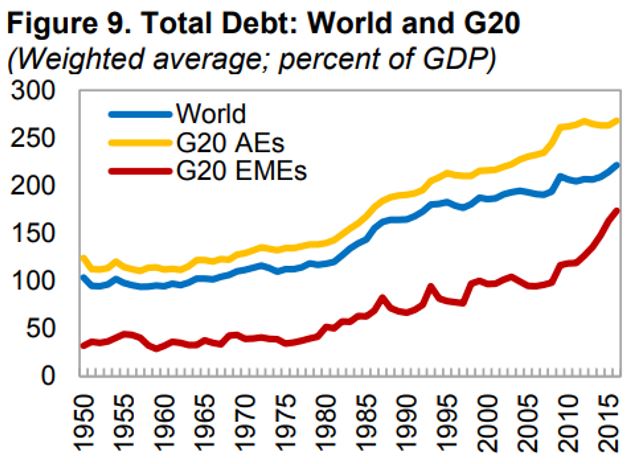

But these strategies have not prevented ongoing increases to private and public debt at the global level. In their 2018 assessment of the global economy, the IMF observed:

Compared to the previous peak in 2009, global debt is now 12 percent of GDP higher. That is, except for a short hiatus, no deleveraging has taken place at the global level since the onset of the GFC.[3]

Compared with 10 years ago, many … economies have higher levels of corporate and sovereign debt, leaving them more vulnerable. With geopolitical tensions also relevant in several regions, we judge that, even for the near future, the possibility of unpleasant surprises outweighs the likelihood of unforeseen good news.[4]

[1] ‘The Global Outlook’, 12 February 2019. www.bankofengland.co.uk/speech/2019/mark-carney-speech

[2] Bank of England (2018) Financial Stability Report, June (Chart A.28 p. 22).

[3] Samba Mbaye, Marialuz Moreno Badia, and Kyungla Chae (2018) ‘Global Debt Database: Methodology and Sources’ IMF Working Paper, May. www.imf.org/en/Publications/WP/Issues/2018/05/14/Global-Debt-Database-Methodology-and-Sources-45838

[4] IMF, op. cit. p. xv.

The Bank of England’s routine overview of financial stability emphasises UK non-financial corporate debt still elevated relative to historical standards, material risks from global debt vulnerabilities, US corporate debt now above pre-crisis levels (in part reflecting the growth of leveraged lending), falling commercial real estate prices, and vulnerabilities in open-ended investment funds.[1] Others warn that private debts have not been resolved but are merely hidden from sight. [2] With the regulatory authorities’ main focus on repairing the banking system, there are also concerns that exposures to debt have shifted to pension and other investment funds. The OECD warn of risks shifting to “more lightly regulated non-bank financial institutions”.[3]

At a global level, post-crisis policy appears to have exacerbated rather than resolved financial factors/imbalances.

First, austerity has not resolved the public debt. While policy was motivated by the (now discredited) threshold of 90% of GDP, on the IMF aggregate for advanced economies, a 70% debt ratio ahead of the crisis has given way to a ratio of above 100% in every year since 2011. No material fall is expected into the future.[4]

Second, monetary policy is supporting a failed fiscal strategy. In a June 2017 speech, Governor Carney illustrated how QE was integral to the present fiscal policy setting.[5] Over 2013-2017 new government bond issuance in G4 countries (UK, Japan, US and Europe) has matched almost exactly central bank asset purchases at around £1.5 trillion a year.[6] In a roundabout way, these purchases of government bonds means central banks are supporting the failure of austerity policies to reduce high levels and hence issuance of public debt.

Third is the consequent feedback to private debt. Under QE, central banks exchange financial institutions’ holdings of government bonds for deposits; these deposits are then re-invested in the UK private sector and/or in the private and public sectors of other countries.[7] In their 2016 assessment, ‘QE: the story so far’, the Bank of England chief economist Andy Haldane and others observed a “powerful international portfolio rebalancing channel”.[8]

As the headline figures for growth and employment show, the consequent flows of international capital are likely to have fostered very vigorous expansion in a number of countries. But these expansions are vulnerable to any reversal of such flows. In the wake of last year’s financial turbulence, some countries are now in serious economic distress. The largest such economies in near or outright recession are Turkey, Brazil, South Africa and Argentina.

Repeated backtracking on intended policy tightening, and virtually continuous quantitative easing (‘QE∞’) at a global level, suggest that the global economy is utterly reliant on monetary ease.

The global economy is not constrained by capacity and inflationary pressures; it is constrained by the need for finance channels to remain open in the high private debt environment. This is in fact the reverse of the inflationary situation. Corporate (and unsecured household) debt on a global level is the result of production going beyond incomes and so beyond purchasing power. The ongoing real-world consequence is an inability to raise prices; this may also be a factor in the dumping of excess production on western markets and consequent trade and geo-political tensions (perhaps as effect more than cause).

There is no danger of inflationary excess, the danger is of financial relations unravelling as they did in the great recession or worst. While post-crisis policy was allegedly aimed at a ‘new model’, fiscal restraint/monetary ease has simply restored a new variant of the pre-crash economy.

While this failure is deep rooted, it is not an inevitable condition. Faced with the same situation in the 1930s, a very different policy approach would gradually and very painfully emerge.

[1] Financial Stability Report, July 2019.

[2] Yannis Varoufakis in the Guardian: ‘ten years after the crash, have the lessons of Lehman been learned’, 18 September 2018. www.theguardian.com/commentisfree/2018/sep/14/the-panel-lehman-brothers-ten-year-anniversary-financial-crash

[3] OECD Economic Outlook, May 2019.

[4] IMF, Historical public debt database. www.imf.org/external/datamapper/datasets/DEBT/1

[5] Mark Carney, [De]Globalisation and inflation, speech, 18 September 2017

[6] And this is despite the main QE action shifting between the Fed., ECD and BoJ (section 3 above). Carney also discussed how Federal Reserve plans to reduce their holdings of government debt will start to put upwards pressure on interest rates. Over 2018 these plans became a reality as did the rise in global interest rates. But, exemplifying the contradictions in the present policy mix, the same reality triggered stress in financial markets. Interest rates are now rapidly falling.

[7] Michael McLeay, Amar Radia and Ryland Thomas (2014) ‘Money creation in the modern economy’ Bank of England Quarterly Bulletin, 2014 Q1

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox