TUC submission to the Treasury for Autumn Budget 2024

Summary

The Autumn Budget should mark a further decisive break from the country’s recent past. Fourteen years of Conservative government has done huge damage to our economy and public finances. The scale of Tory of failure becomes more apparent each day, as the extent of the crisis facing our public finances and our public services is uncovered.1

But this toxic legacy must not be allowed to define our future. Working people and their families have paid the price for failure for far too long. The Chancellor now has an important opportunity to support the economy, strengthen growth and start to rebuild living standards.

This submission sets out the scale of the economic and fiscal challenges the country faces and evidences the need for change.

It makes the case for the following priority TUC proposals:

- reforms that ensure higher investment, boosting growth now and expanding our future productive potential (section 2):

A significant expansion in public investment, to strengthen UK productivity and competitiveness and crowd in private capital. This shift will help achieve the government’s stated aims of securing a just transition for high-carbon workforces and 650,000 new good jobs in clean industries.

Fiscal rules and multipliers that support urgently needed capital investment.

Closer trading relations with the EU, based on high standards of workers’ rights.

- reforms that deliver higher pay and higher productivity, supporting growth and ensuring its rewards are fairly shared with working people (section 3):

Delivery in full of the government’s new deal for working people, as set out in its plan to Make Work Pay, with new employment rights to be implemented at pace and effectively enforced.

public services workforce commission tasked with developing a comprehensive, cross-government strategic plan to address urgent workforce challenges. The plan should serve as the foundation for departmental workforce strategies in every of area of the public sector, to bring an end to the recruitment and retention crisis.

Reinstatement of the Union Learning Fund, breaking down barriers to opportunity for the most marginalised workers and supporting businesses to grow.

Removal of the income eligibility rules and waiting days for sick pay at pace, alongside establishment of a new time-limited opportunity commission, which could seek to set short and medium-term priorities for social security spending across people’s lifetimes.

Fairer taxes, addressing the situation where wealth is taxed far less than work and providing urgently needed funds to support our public services.

Section 1: Failures of the past

The UK The last 14 years have been a failure for living standards and jobs, growth and the public finances.

Living standards and jobs

Workers have endured the worst pay crisis for two centuries. Even now real pay is still barely changed from where it was before the global financial crisis, and average annual earnings stand around £15,000 below where they would be had pre-financial crisis trends continued. A living standards squeeze of this scale is unprecedented across the last two centuries.

Compared with 2010 when the Tories took office, real pay in the private sector (in 2024 Q2) is up only 5.2 per cent. If the comparison is made using RPI instead of CPI, real pay is down 8.8 per cent. Over the same period real pay is down 3.6 per cent in the public sector on CPI and down 16.5 per cent on RPI.

While the pay crisis has been relentless, the latest three years have been particularly difficult as they have seen the worst price increases for forty years. The headline CPI measure of inflation has now returned to the 2% target, but the cumulative damage has been severe. Compared with the start of 2022, CPI inflation is up 20% and RPI up 27%: in effect, working people have experienced ten years of inflation in three (the worst inflation outcome of all advanced economies).2

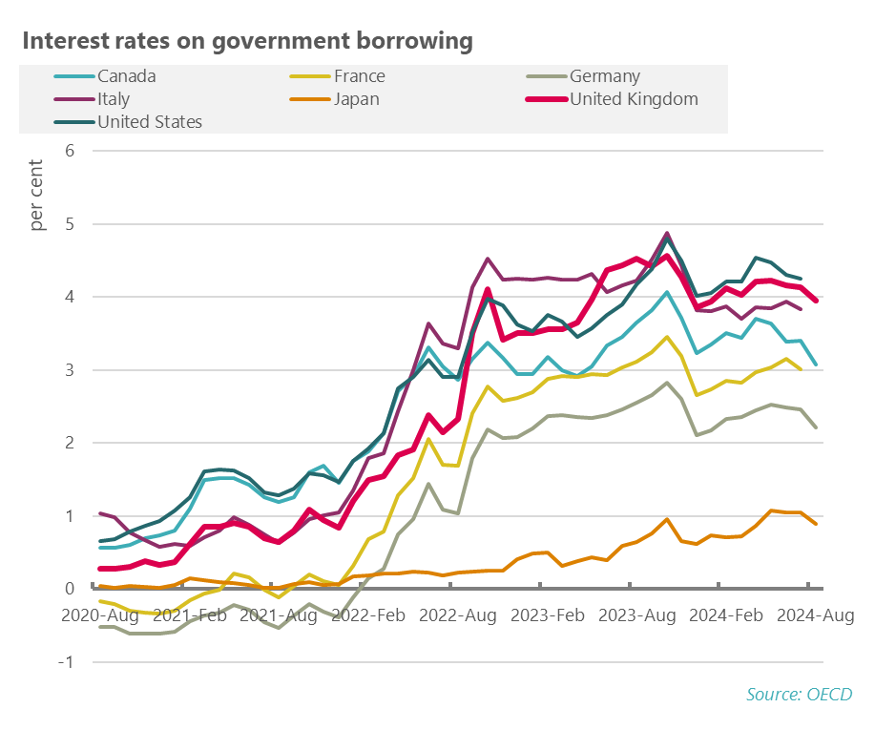

On top of this, households have endured an equally unprecedented rise in interest rates – described as ‘monetary austerity’ by Andrew Haldane the former chief economist of the Bank of England.3 The scale of this pressure was again exacerbated by the previous government’s failures, and had direct impacts for the public finances: following the Liz Truss mini-budget, government borrowing rates in the UK moved from the middle to the top of all G7 economies. Over the past three years, the rise in borrowing costs for the UK government has been higher than all other advanced nations. 4

- 1 https://www.gov.uk/government/speeches/chancellor-statement-on-public-spending-inheritance

- 2 https://www.tuc.org.uk/news/tuc-uk-suffered-highest-inflation-and-lowest-growth-g7-last-two-years

- 3 https://www.ft.com/content/b70b7a8f-cc1a-4be9-b51a-866f5d0dab23

- 4 Rise in rates in percentage points, July 2021 to July 2024: Canada: 2.2, France: 3.0, Germany: 2.9, Italy 3.1, Japan: 1.0; UK: 3.4; and US:2.9.

The Bank of England’s first rate cut at the start of August gave relief to millions of families and businesses and should be the first of many.

Economic failures have left the jobs market in a fragile position, with working people and their livelihoods left paying the price:

1.4 million people (4.2 per cent) are unemployed, up 100,000 from the recent low at the end of 2024.

Employment in the private sector has fallen by 250,000 since the end of 2023, according to the payrolls data on employees. The headline jobs figure has been held up by increases in public services.5

Vacancies have fallen by a third to 860,000 from the recent peak in 2022 of 1,300,000.

9.3 million people are economically inactive, close to the all-time peak of 9.5 million in 2011.

Economic inactivity due to long-term sickness is at record levels: averaging 2.8 million people over the first half of 2024, up sharply from 2.0 million five years ago and greatly higher than the previous peak of 2.4 million people in 1998.

Zero hours contracts remain close to record levels, with over a million workers employed on this basis.

A record 4.1 million workers are in insecure work:

0.99m zero-hours contract workers (excluding the self-employed and those falling in the categories below)

1.04m people in other insecure work – including agency, casual, seasonal and other workers, but not those on fixed term contracts

2.11m people in very low-paid self-employed (defined as those who earn less than two thirds of the median wage, £10.45 per hour)

1 in 8 workers in the UK are now in precarious employment.6 BME workers have borne the brunt of this change. 1 in 6 BME workers in the UK are trapped in precarious employment, compared with 1 in 9 white workers.

Growth and public debt

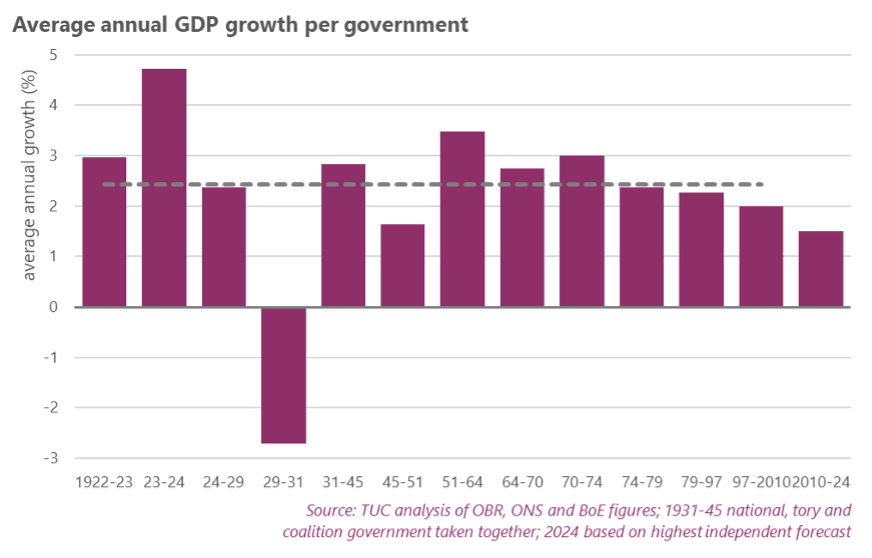

Over the Conservatives period in office, the performance of economic growth was disastrous. TUC analysis of official figures shows that over the past century growth has averaged 2.4 per cent a year. But between 2010 and 2024 growth averaged only 1.5 per cent. This is the worst performance since the Second World War – and second only to economic performance during the great depression of 1929-1931.7

- 5 It is not possible to adjust these figures for private sector employment in public service industries.

- 6 https://www.tuc.org.uk/news/number-people-insecure-work-reaches-record-41-million; NB the comparison begins in 2011 as the first full year for which the relevant data are available.

- 7 https://www.tuc.org.uk/blogs/worst-government-growth-modern-times

While the disastrous Truss mini-Budget caused an economic and household crisis, the worse growth performance since the great depression long predated these efforts.8

While the recent figures show stronger than expected growth at 0.7 per cent in Q1 and 0.6 per cent in Q2, the repercussions of the pay crisis remain and the recovery remains far from secure.9

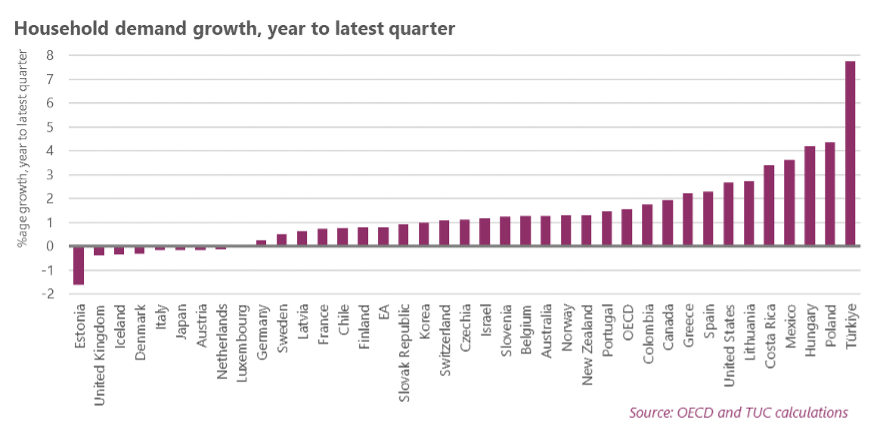

The expenditure measure of GDP shows household demand near flatlining, and business investment and trade are weak. At face value – and these figures are subject to uncertainties – the main area driving the growth we have had is government spending.

Stagnant consumer spending is unsurprising given the living standards crisis. While the ONS report overall GDP growth strong relative to other advanced economies, at -0.3 per cent on the year, household demand is still the second weakest in the OECD – as the below chart shows:

- 8 https://www.tuc.org.uk/news/tuc-conservatives-are-presiding-over-worst-period-economic-growth-1920s

- 9 Beyond the headline figures there remain wider underlying risks, in part related to the sharp increase in interest rates across the globe. The most commonly raised threats are geopolitical crises, the commercial real estate market, repercussions from (in some cases chronic, above all in Kenya) pressures on low-income countries and emerging market economies, the likely excessive valuation of technology companies and other financial engineering including (as the Bank of England have warned) private equity schemes.

Business investment also fell by 1.1 per cent on the year, with low consumer demand likely to be holding confidence back more generally. Fragile global conditions also mean trade is weak, with exports declining on the year by 1.1 per cent.

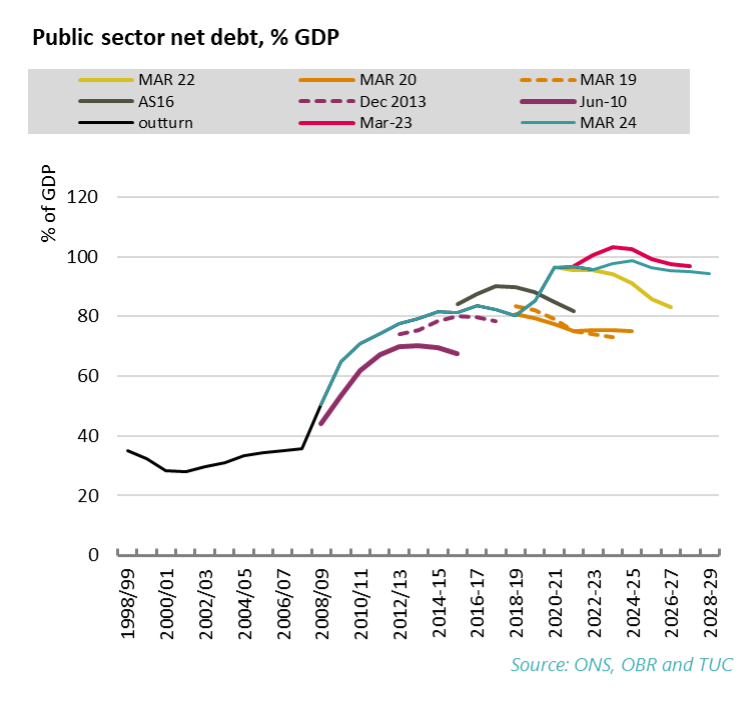

Sustained failures on growth have also had significant impacts for public debt. With our economy so much smaller than anticipated, government revenues have fallen below forecast and our debt has increased as a proportion of GDP. The chart below shows how far removed outcomes on debt have been from the course the Conservatives tried to set in June 2010. The plan was to reduce the ratio to 67 per cent by 2015-16. But instead in their March 2024 forecast the OBR reckoned the ratio to be 99% in 2024-25. While the latter figure has obviously been affected by the pandemic, TUC analysis showed the failure on public debt ahead of the pandemic the worst in at least a hundred years.10

Public investment and public service spending

A critical factor in this failure has been the approach the Conservatives took to public investment and public services. From 2010 public spending was severely restricted, at a time when the recovery inherited from Labour was likely still fragile.

Public investment alongside private investment matters for creating the assets and infrastructure that can grow our economy and create extra capacity for the future; as the OBR recently set out:

“[Public investment] can have a significant impact on the supply potential of the economy. As with private investment, public investment affects economy-wide potential output principally via its impact on the stocks of assets that support economic activity. These assets include infrastructure assets (such as the transport, energy, and water networks), public service assets (such as schools, hospitals, and public housing), and intangible assets (such as those created by research and development).” 11

In 2018 TUC analysis showed overall UK investment third from bottom of all OECD countries, and coming in the bottom half of OECD countries for all broad categories of investment: dwellings, other buildings and structures, transport equipment, ICT equipment and intellectual property product.12

Others have updated the analysis to show the dismal performance continuing. The IPPR show business investment “ranking a lowly 28th among 31 OECD countries” and the lowest in the G7 for three years running to 2022.13

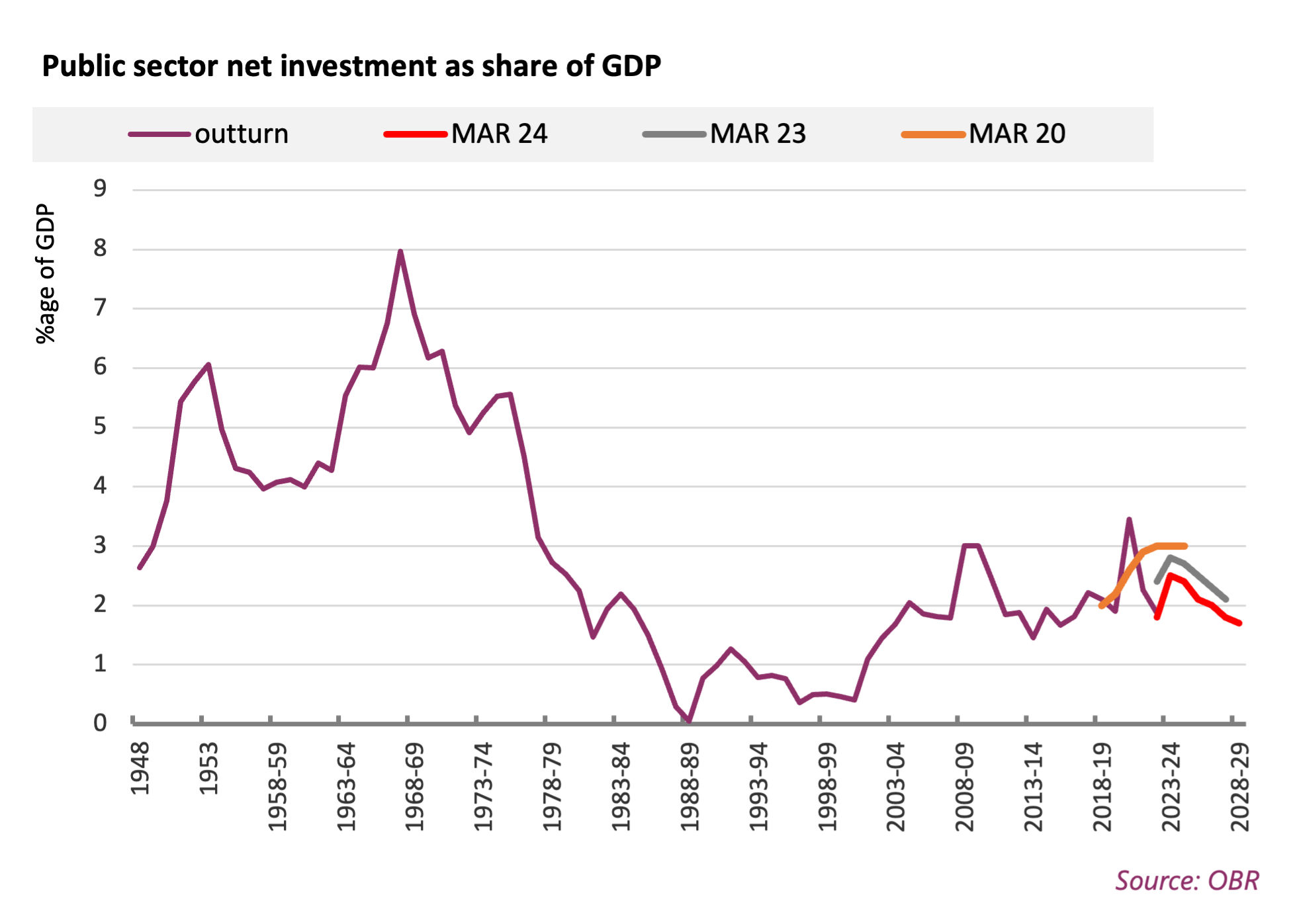

As is widely known, upon taking office George Osborne immediately attacked public infrastructure spending. The chart below shows public sector net investment averaged only 1.8 per cent over 2010-11 to 2014-15. Ahead of the pandemic, the government finally planned to increase public sector net investment to 3 per cent of GDP. But, instead, March 2024 OBR projections showed a gradual fall to 1.7 per cent – which would be the joint second lowest figure in 25 years.

Not only is this position far too low, continued volatility in public investment targets and ambitions has also had a negative impact on delivery, further undermining the state of our public infrastructure and our wider economic performance.

The IPPR have set out that ‘the consensus of investment is shifting – public investment can crowd in business investment’:

“Well designed, high-quality public investment can crowd in private sector investment and act as a foundation for equitable growth …. There is a large body of literature highlighting that public investment can boost economic potential of the economy ... by making the private sector more productive and by crowding in private investment. Moreover, public investment can act as a coordinating device and unlock network effects – for instance, when helping an electrical vehicle charging network take off …”14

We urgently need a reset that ensures strong growth in both public and private investment outcomes.

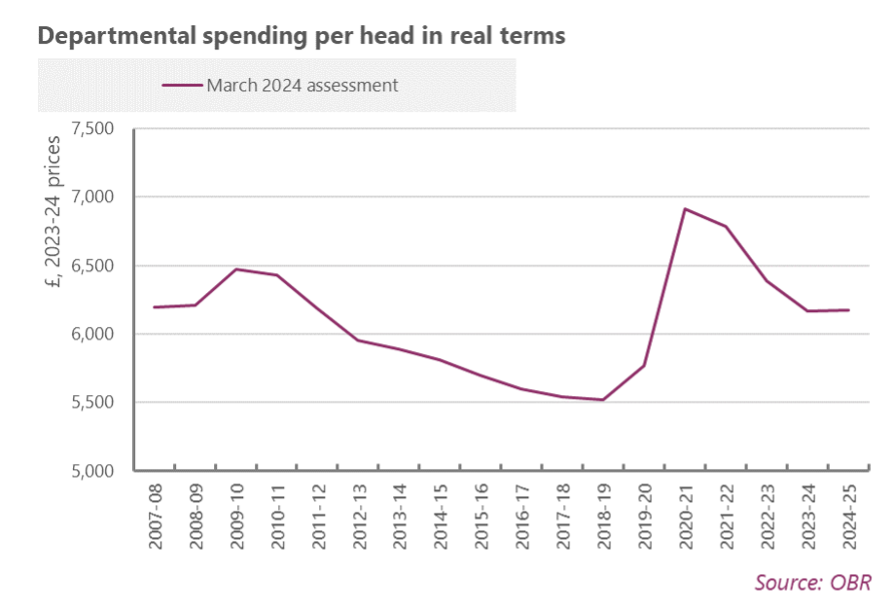

Spending on public services has also been decimated over the last 14 years. This has been disastrous for public services and has also held back the economy and in turn created further pressure on public debt. By 2018-19 the widely used real terms per head measure showed departmental spending down 15 per cent from £6,500 to £5,500. After an increase during the pandemic, spending was cut back sharply again and for 2024-25 is projected to be 5 per cent below the 2009-10 position.

The cumulative loss over the past 15 years has been immense. The Institute for Government public services’ performance tracker captures the scale of the damage: 15

“Public services that have for years been creaking are now crumbling. The public is experiencing first-hand the consequences of successive governments’ short-term policy making.”

Section 2: Investing for the future

After so many years of failure, it is time for change. The new government now has a vital opportunity to secure stronger growth. This section sets out the TUC’s policy proposals for ensuring the investment the UK economy desperately needs. Our priorities include:

An immediate boost to public investment, including through ambitious delivery of GB Energy and the National Wealth Fund.

Additional measures to boost business investment, including an Industrial Strategy Council with the ability and latitude to act, ensuring pension funds better support growth (while protecting members' interests) and improved trading relations with the EU.

Fiscal rules and models that support growth. Changes that could be considered include revised measures of the fiscal aggregates themselves, which could include ensuring the rules target public sector net worth rather than public sector net debt. The OBR should also review its models with a view to making a more realistic assessment of multipliers and the output gap.

Boosting public investment

Public investment is essential to strengthen UK productivity and competitiveness and achieve the government’s stated aims, including a just transition for high-carbon workforces and 650,000 new good jobs in clean industries. The TUC is highly supportive of the government’s manifesto commitments, including through the British Jobs Bonus, Warm Homes Plan, Great British Energy and National Wealth Fund.

These plans provide a welcome and significant first step. They can shift the country towards the investment levels needed to deliver TUC’s proposals for a broad programme of infrastructure upgrades.16

We also welcome government recognition of the wider synergies between private and public investment, 17 and of the importance of ensuring ownership models put the public good first. As new institutions are set up, to maximise their benefits it will be crucial to ensure that their governance structures reflect a clear mission, sufficient resource to enact it, and accountability. Ensuring representation in governance structures for the workforce and for devolved regions and nations will be an important part of this.

It will also be important that public investment comes with strong conditions to ensure good outcomes in terms of jobs, employment standards and local supply chains.

Great British Energy

We welcome the creation of Great British Energy with capitalisation of £8.3 billion, the intention to use the company to lead industrial growth across a range of technologies, and the mission to retain a public stake to deliver revenues for the UK public for generations to come. In order to fully realise the potential of Great British Energy, the government should:

Aim to grow GBE in line with European peers like EDF and Orsted over the long-term.

Enable GB Energy to borrow, and categorise its debts in line with practice of publicly-owned energy companies from other countries. This could be done by classifying its debts similarly to those of publicly-owned banks – i.e. excluding its debts from the existing PSNB ex and PSND ex measures.

National Wealth Fund

The new National Wealth Fund (NWF) has the potential to be a long-term policy instrument to protect and grow UK manufacturing industries, helping deliver the government’s vision of 650,000 new jobs alongside protecting the UK’s cornerstone industries like steel and automotive, and their supply chains. However, success will rest on the design and delivery of the Fund. We propose that:

The National Wealth Fund should function as an active policy instrument, a key lever in delivering and implementing a comprehensive industrial strategy.

The National Wealth Fund should be enabled to borrow, with its debts to be excluded as with the existing PSNB ex and PSND ex measures.

The NWF’s KPIs and goals should not be limited to crowding in additional private finance. Its KPIs should include:

Future-proofing high-carbon jobs, skills and industry.

Scaling up quality jobs and economic activity in new clean sectors in held-back regions.

A more dynamic, competitive and resilient manufacturing sector.

The Fund should take a proactive role in improving the governance, employment practices, and corporate responsibility of the companies it backs.

The NWF should be able to take public equity stakes, crowding in additional private capital financing and securing ongoing public returns.

Infrastructure

Additional financing decisions will also be needed to facilitate the upgrade of UK infrastructure that the country needs and expects. We believe that this should include:

approving financing without delay for new nuclear, including Sizewell C;

investing into future-proofing the UK’s foundation manufacturing industries.

The TUC’s ‘Invest in Our Future’ briefing outlines a broader programme of necessary public investment into infrastructure upgrades over the course of a Parliament.18

Transport

The TUC’s Public Transport Fit for the Climate Emergency report sets out an ambitious programme of investment aimed at renewing our public transport system, which is essential to growing the economy and meeting our net zero targets.19 Poor connectivity continues to undermine workers’ opportunities and weakens productivity.

We welcome the resetting of industrial relations in the transport sector. We also support plans to establish GB Railways and the £2.2bn savings identified as a benefit of nationalisation. Extending the plans to include nationalisation of the rolling stock companies would significantly increase the savings achieved.

The cancellation of phase 2 of HS2 by the previous government was a mistake and there has been major uncertainty on rail investment ever since. That uncertainty needs to end – starting with confirmation of the extension of HS2 to Euston and a clear plan for investment in northern England.

Building stock

The trade union movement strongly supports public investment into upgrading the UK’s building stock, to boost energy efficiency and reduce use of imported fuels. This should include the committed funding for the Warm Homes Plan, as well as renewing past funding programmes, including the Public Sector Decarbonisation programmes.

Government should also identify finance for the upgrades necessary to public buildings, including upgrading school buildings to both meet energy efficiency and temperature standards.

More pressingly, the government must address long-standing health and safety issues across the public estate, such as RAAC concrete and asbestos, that represent a threat to life. The TUC propose the government start by publishing a national risk register for all public buildings. People deserve to know the buildings they work in and use are safe. Where the government is unclear about the safety of buildings, they should ensure the appropriate persons take immediate action to carry out risk assessments, to be made publicly available.

Additional measures to boost business investment

Wider action is also needed to address the UK’s persistent failures on business investment rates.

Industrial strategy governance

This government has pledged that a strong, mission-led industrial strategy will guide its work to unlock a new era of economic growth that is good for workers and aligned with the UK’s climate commitments. The Industrial Strategy Council must have the ability and latitude to act, to support government’s implementation as a critical friend. It will need an ambitious and clear mission, should be sufficiently resourced to develop its own analysis and have metrics to provide oversight and accountability on delivery. Lessons could be drawn from the success of the success of the Climate Change Committee (CCC) and the Office for Budget Responsibility (OBR) in building stability and consensus. Trade union representation across the Council will be important. In our view this should at least improve on the baseline set by the previous government’s green jobs taskforce (where there were two business representatives for each trade unionist).

Pensions investment

The TUC supports the Chancellor’s efforts to ensure that pension funds better support UK growth, provided this is done without compromising those funds’ primary purpose of meeting the retirement needs of their members. Maintaining and enhancing levels of governance and member protections will be crucial to this. Pension schemes are scaling up and investments are increasing in complex, illiquid, and higher charging asset classes – and these investment decisions must ultimately rest with trustees. There is potential to channel more investment into the UK economy through the consolidation of defined contribution schemes and creation of new large scale collective schemes, together with increased contribution rates and support for open defined benefit schemes.

Carbon Border Adjustment Mechanism

Additional policy processes including the Carbon Border Adjustment Mechanism (CBAM), also have a role to play, and must be optimised to protect UK jobs in at-risk industries including steel. As far as possible, the UK CBAM regime should match the standards, thresholds and processes of the EU regime, to avoid:

creating double burdens on companies; or

creating a situation where lower standards in the UK enable importers to ‘dump’ cheaper, higher carbon goods in the UK.

This means, as far as possible, matching the timeline of the EU scheme which has already started to apply in some cases since 2023, and will be implemented in full in 2026.

The only exception to this that we would support would be to provide an exemption to CBAM for goods from certain lower income countries, in order to support international development goals and the ability of low-income countries to decarbonise their economies, as proposed by the Trade Justice Network. This should be done only where it is consistent with the goal of supporting UK based industry to decarbonise (e.g. should not currently apply to cheaper steel from India and China).

Corporate governance reform

Corporate governance reform is an essential part of delivering higher business investment and sustainable and inclusive company growth. Our current system prioritises the interests of shareholders over those of other stakeholders and the long-term success of the company, which encourages companies to prioritise short-term returns to shareholders over both wages and long-term investment.

The share of profits allocated to dividends has increased significantly over time, rising from 16 per cent in 1987 to reach at 52 per cent in 2018. It fell during the pandemic but then rose sharply once more, reaching 41 per cent in 2021. The opportunity cost of spending ever-higher amounts on dividends is significant. Between 2008 and 2019, dividends grew three times faster than wages; if pay had kept up with dividends over this period, in 2019 the average worker would have been £16,400 better off. In 1987, business investment was around four times higher than dividends, but his gap has narrowed over time and in 2021 they were close to parity.20

Research 21 suggests a direct link between higher levels of shareholder returns and low levels of investment. For example, an academic study of 182 companies in the FTSE 350 from 2009 to 2019 found that the top 20 per cent of companies in terms of shareholder returns to net income paid out 178 per cent of their net income to shareholders over the period. These companies also had the lowest growth in R&D, the lowest productivity increases, the lowest performance in terms of profitability and investment returns and the highest debt to equity ratio.

Corporate governance reform to require company directors to promote the long-term success of the company as their primary aim and promote worker directors on company boards to bring a workforce perspective to company decisions would help companies to deliver higher levels of R&D and promote long-term, sustainable company growth.22

Improved trading relations

The TUC welcomed the government’s announcement that it will reset the UK’s relationship with the EU to form a partnership based on mutual high standards on employment rights and environmental standards.

The UK-EU Trade and Cooperation Agreement (TCA) contains a commitment for the agreement to be reviewed in 2026, five years after it entered into force. This review, as well as other channels of dialogue, should be used by government to:

ensure the UK implements new employment rights that are introduced in the EU so UK workers do not fall behind;

remove barriers to trade between the UK and EU through close regulatory cooperation which is vital for encouraging investment;

link the EU and UK Emissions Trading Schemes so the UK does not get hit by Carbon Border Adjustment Mechanism tariffs;

secure UK-EU mobility agreement which does not involve short term visas for workers and allows UK creative workers to tour without barriers in the EU.

Building a closer relationship with the EU as our most important trading market, and one which respects high standards of workers’ rights should be the government priority - rather than pursuing trade talks with countries that are abusing fundamental human and labour rights. Agreeing trade deals with countries that do not respect fundamental rights puts good jobs at risk as domestic industries could be undermined by imports from countries that are cheaper due to prices being held down due to worker exploitation.

Fiscal rules and models that support growth

Fiscal rules and accounting standards must also be designed to support the growth and investment the country needs.

Under the Conservatives the rules were changed nine times 23 and the public finances still deteriorated to an unprecedented extent (as set out above). While the Chancellor’s recent statement on the country’s public spending inheritance rightly pointed to the disarray and negligence caused by previous governments, the lesson from past failure must also be that an overly restrictive household budgeting approach to the public finances risks being counterproductive. It is pro-growth policies that will permit our national revenues to improve, and in turn these must be enabled by our fiscal framework.24

Many commentators have set out how fiscal rules and accounting standards are operating to hold back growth. Former Bank of England chief economist Andrew Haldane has warned that “... Existing fiscal rules risk starving the economy of the very investment needed to boost medium-term growth and, ultimately, pay down debt and lower taxes”. Likewise, the National Institute of Economic and Social Research (NIESR) has argued: “Not only are these rules are not being met, but they are also inadvertently constraining the public investment needed to improve economic growth”.25

These and other contributions make the argument that certain government expenditures ultimately strengthen the capacity and capability of the economy. The most direct of these are expenditures are on infrastructure, as discussed in the previous section. But others also stress investment should be understood more broadly, not least social investment which is strengthened for example by spending on health, education and care services.26

Public service spending is also vital to the good operation of the economy, and in recent years the economic consequences of spending cuts have been stark. Declining outcomes in areas including health, education and crime bring with them wider economic impacts. In her pre-election Mais lecture, the Chancellor emphasised the economic costs of deteriorating population health:27

“And an economy built on contribution of the many means recognising that we don’t just need growth to fund strong public services. We need strong public services to support economic growth, including a serious plan to get the long-term sick – let down by ballooning NHS waiting lists, failing mental health support, an inflexible welfare state, and inadequate employment support – back to work.”

In July the Covid-19 Public Inquiry published the report from the Module One investigation into the resilience and preparedness of the United Kingdom. The report highlighted the devastating consequences of austerity in the decade that preceded the pandemic and set out that spending cuts had left the UK population more vulnerable to the impacts of the pandemic.28

The TUC are concerned that over recent years fiscal rules have become a barrier to growth, as the gains brought by public investment may not be accurately reflected in OBR assessments and/or in the five-year time horizon of their forecast. The OBR themselves have now detailed how the main (supply-side) gains from investment spending operate in their forecast as follows: 29

“we find that a sustained 1 per cent of GDP increase in public investment could plausibly increase the level of potential output by just under ½ a percent after five years and around 2½ per cent in the long run (50 years)”.

This may re-enforce the case for a changed approach to assessment or changed time horizons in the UK’s fiscal rules.

Others advocate changing the measures on which the fiscal rules are based. Changes that could be considered include revised measures of the fiscal aggregates themselves, which could include ensuring the rules target public sector net worth30 rather than public sector net debt. 31 There could also be value in ensuring that certain Bank of England transactions are excluded from the figures on which the fiscal rules are based.32

As set out in the previous section, immediately it is important to ensure that Great British Energy and the National Wealth Fund debts are excluded, as with the existing treatment of the publicly owned banks, within PSNB ex and PSND ex figures.

We are also concerned to ensure that expenditure multipliers within government modelling take accurate account of the economic benefits that government expenditure brings. Changed government spending leads to changed incomes for households which impact on spending overall, and the sum of the parts is changed economic output. But we are concerned that existing economic models underestimate these effects.

For example, it remains our view that Office for Budget Responsibility models have consistently understated the impact of government spending cuts on the economy (so-called multiplier effects).33 TUC (2019) analysis has shown that for all OECD countries where public spending was cut, the private sector contracted and there was a significant reduction in economic growth. 34

This view has also been taken by many other commentators, who agree with us that current models risk underestimating the multiplier effects that government spending has. A multiplier of 1½ was in line with the view of the Obama administration, and consistent with UK experience of austerity.35 But instead the OBR forecasts remained consistent with the monetarist view that private sector activity will be ‘crowded in’ by public sector cuts.

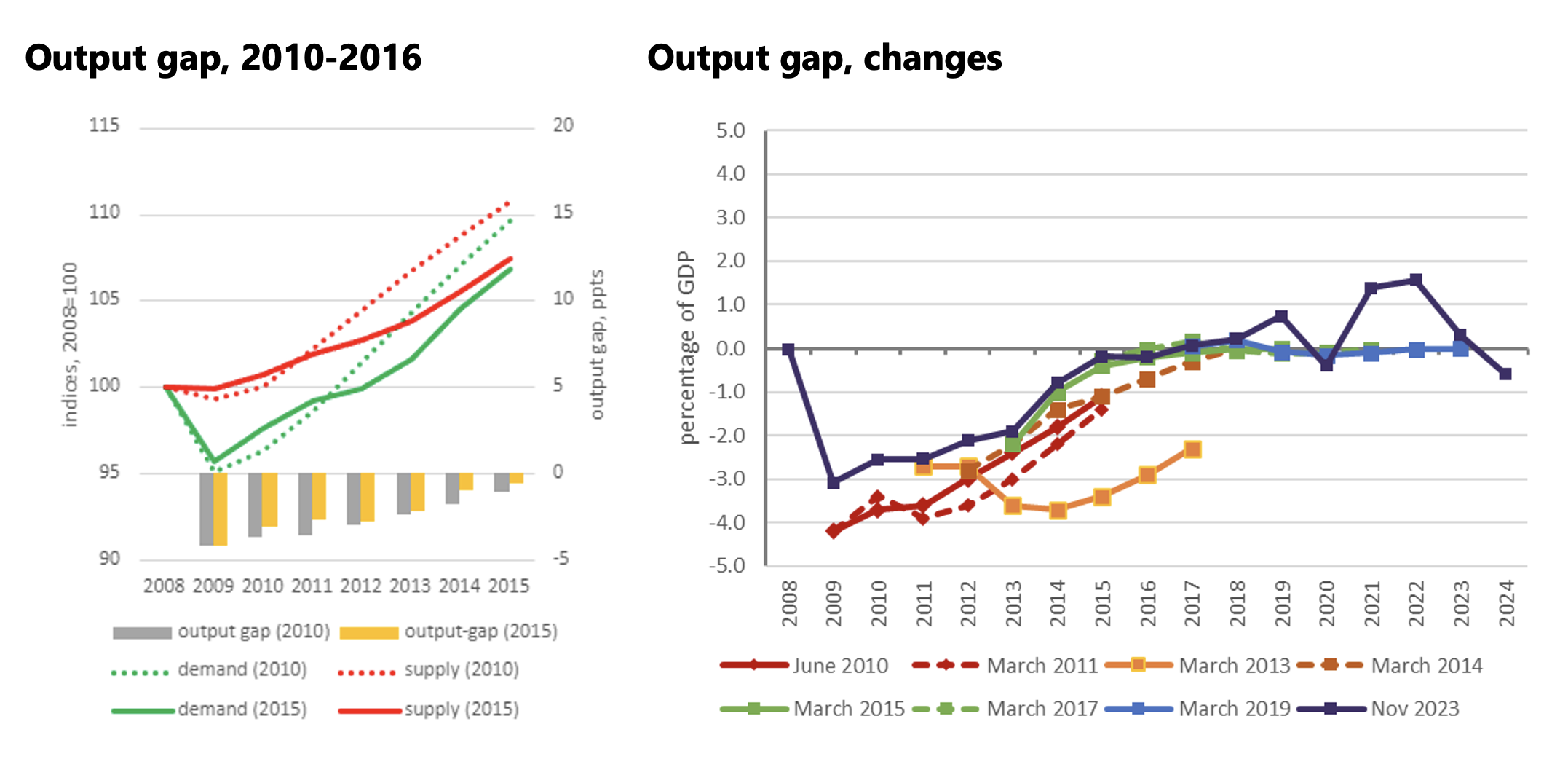

Modelling processes then compound the problem by wrongly interpreting weaker than anticipated outcomes. On a demand view, the shortfall follows the very material impact of government expenditure on aggregate demand and GDP growth: ‘potential’ was unchanged, and the output-gap widened. But instead, the OBR models have consistently judged that the failure was one of supply/potential. The left chart below illustrates the changed OBR assessment of the position in 2010 and then 2015; the right chart shows the supply judgement is a systemic tendency, with the overall trajectory of the output-gap little different now (in fact narrower) to the original assessment in 2010 – in spite of a vast shortfall in outcomes.

- 15 https://www.instituteforgovernment.org.uk/publication/performance-tracker-2023/summary

- 16 https://www.tuc.org.uk/research-analysis/reports/investing-our-future

- 17 https://www.ippr.org/articles/rock-bottom

- 18 https://www.tuc.org.uk/research-analysis/reports/investing-our-future

- 19 https://www.tuc.org.uk/research-analysis/reports/public-transport-fit-climate-emergency

- 20 These figures drawn from ONS data sources including National Accounts and are set out in full in TUC (2022) Companies for People How to make business work for workers, available at https://www.tuc.org.uk/research-analysis/reports/companies-people-how-make-business-work-workers

- 21 Colin Haslam, Adam Leaver, Richard Murphy, Nick Tsitsianis (29 June 2021) Productivity Insights Network Report Assessing the impact of shareholder primacy and value extraction: Performance and financial resilience in the FTSE 350, available at: https://research.cbs.dk/en/publications/assessing-the-impact-of-shareholder-primacy-and-value-extraction-

- 22 For further discussion of the case for corporate governance reform and the TUC’s detailed proposals, please see TUC (2022) Companies for People How to make business work for workers, available at https://www.tuc.org.uk/research-analysis/reports/companies-people-how-make-business-work-workers

- 23 https://www.theguardian.com/uk-news/2024/mar/05/uks-fiscal-rules-obr-treasury-budget-jremy-hunt

- 24 As Keynes put it, “There is no possibility of balancing the budget except by increasing the national income” (Collected Writings, Volume IX, p. 347).

- 25 NIESR, UK Economic Outlook, May 2024, ‘A Pre-Election Gloom’: https://www.niesr.ac.uk/publications/pre-election-gloom?type=uk-economic-outlook

- 26 https://wbg.org.uk/wp-content/uploads/2023/02/2023-01-Womens-Budget-Group-submission-to-HMT-budget-representation_Published.pdf

- 27 https://labour.org.uk/updates/press-releases/rachel-reeves-mais-lecture/

- 28 https://www.tuc.org.uk/blogs/austerity-crisis-covid-19-inquiry-highlights-uks-pre-pandemic-weaknesses

- 29 https://obr.uk/public-investment-and-potential-output/

- 30 https://www.resolutionfoundation.org/app/uploads/2019/10/Totally-net-worth-it.pdf

- 31 https://researchbriefings.files.parliament.uk/documents/CBP-9329/CBP-9329.pdf

- 32 https://www.ft.com/content/5198b1d8-8801-454b-b549-97e04687d5db

- 33 Most prominently in 2012 the IMF retracted its earlier view, on which the OBR multipliers were in part based (World Economic Outlook, October 2012). Other commentators resisted for longer but came round. In 2020 the ‘editorial board’ of the Financial Times finally recognised: “That consensus can be wrong was on display after the 2008 financial crisis, when many organisations — including this newspaper — advocated fiscal retrenchment”. “Cutting spending may have had a bigger negative impact than expected”, they grudgingly conceded [our emphasis]: https://www.ft.com/content/7b6242c5-8a25-4d98-ba0a-f9d9bd046085. Likewise the OECD were an early and forceful champion of austerity, but in 2021 the (then) chief economist Laurence Boone admitted: The mistake that we made was not a lack of stimulus during the trough in 2009 … the mistake came later in 2010, 2011 and so on, and that was true on both sides of the Atlantic”: https://www.ft.com/content/7c721361-37a4-4a44-9117-6043afee0f6b.

- 34 https://www.tuc.org.uk/research-analysis/reports/lessons-decade-failed-austerity

- 35 See section 5 of discussion in ‘From false multipliers to nonsense output gaps’: https://progressiveeconomyforum.com/publications/from-false-multipliers-to-nonsense-output-gaps/.

The supply-failure judgement is reinforced by dismal productivity statistics.36 Yet, as the TUC have repeatedly pointed out (following Bob Rowthorne and Bill Martin),37 over this period, low productivity outcomes are effect, not cause. The labour market adjusted to (austerity-driven) weak GDP growth through price / wages (including reduced quality) rather than quantity / jobs. The low productivity figure is simply a residual of these causal factors. Certainly there are decades-long supply-side failures, but from 2010 the critical factor in outcomes has been weak demand.

The sum of the parts has been the ‘doom loop’ where cuts hit the economy much harder than expected, meaning further damage to the public finances.38 At the start of 2023, TUC estimated that between 2010 and 2023 around £400bn of prosperity had wrongly been written off. But wrongly written of prosperity can be recaptured. Possibly £400bn is an upper bound, but the OBR should reassess the position taking as the starting point a more realistic assessment of multipliers and the output gap.39

Section 3: Stronger, fairer growth

The relationship between growth and fairness operates in both directions. While stronger growth supports higher pay and permits more expenditure on public services and social provision, better protections for workers and stronger public services also support growth. This section outlines key TUC priorities for improved public services through to a higher minimum wage, including:

Full implementation of the government’s plan to Make Work Pay, alongside early implementation and meaningful enforcement.

Establishment of a Public Services Workforce Commission and reform of the Pay Review Bodies to fix the sector’s recruitment and retention crisis, restoring our public services fuelling the government’s mission to deliver economic growth.

Partnership between trade unions and employers to implement a social care Fair Pay Agreement as a first step towards the creation of a National Care Service.

Reinstatement of the Union Learning Fund as a key strategic initiative within the government’s breaking down barriers to opportunity mission.

Removing the income eligibility rules and waiting days for sick pay at pace.

Establishment of a new time-limited opportunity commission, which could seek to set short and medium-term priorities for social security spending across people’s lifetimes.

Rapid implementation of the measures contained within the Pensions (Extension of Automatic Enrolment) Bill 2023.

A rebalancing of taxation away from work towards wealth, including through increasing capital gains tax to bring it into line with income tax.

Making Work Pay

The TUC supports full implementation of the government’s plan to Make Work Pay, with legislation within 100 days, early implementation and effective enforcement.

Employment rights in the UK are significantly weaker than most comparative countries. Recent analysis by researchers at Cambridge University for the TUC found that labour laws in the UK are half as protective as those found in France and significantly weaker than other large European countries such as Spain, Italy and Germany.40

The UK’s more limited protections bring detriment to working people, but also to our wider economic performance. In 2018 the OECD concluded “countries with policies and institutions that promote job quality, job quantity and greater inclusiveness perform better than countries where the focus of policy is predominantly on enhancing (or preserving) market flexibility”.41

This strong association between strong workers’ and economic gains is increasingly widely recognised. For example, analysis for the Digital Futures at Work Research Centre found that stronger labour protection is associated with higher employment and lower unemployment. The study also found that regulating working time, and employee representation, have positive productivity effects,42 concluding that:

“Where labour laws contribute to rising productivity, increasing employment, and a higher labour share of national income at the same time, they help ensure that the benefits of productivity growth are not exclusively retained by firms, but are shared more widely with workers and households, in the form of higher wages and a reduction in the time spent at work.”

New TUC and IPPR research 43 has also found that employers recognise the substantial benefits that improved employment protection will bring, improving workforce health, increasing retention, boosting productivity and profits.

To ensure these gains accrue to both working people and their employers, rights must be properly enforced. But for too long state enforcement bodies have been underfunded.44 Government plans to merge several of the bodies into a Fair Work Agency will only succeed will sufficient resources, and the tribunal system is creaking with parties having to wait on average nearly a year for even a preliminary hearing.45

So Make Work Pay must also be accompanied by a strong government commitment to funding these elements of the enforcement system, ensuring that the government’s promised changes to labour rights result in the desired improvements to the lives of working people and the broader economy.

A pragmatic, progressive partnership working in the public sector

For a new government, solving the issues facing the public sector workforce is crucial, particularly one focused on delivering economic growth. The economic cost of underinvesting in public services and their services is evident in the record levels of economic inactivity due to ill-health to recruitment and retention issues stemming from skills shortages.

A robust and thriving economy relies on strong and resilient public services, delivered by a skilled and motivated workforce. As the employer in the public sector, government is uniquely positioned to deliver on this, using the upcoming Autumn Budget as an opportunity to reverse the decline of public service delivery and address the severe workforce crisis the sector is experiencing.

We welcomed the Chancellor’s recognition of the vital role the workforce plays in public service delivery in her response to the 2024/25 pay review body process as well as her commitment to early and constructive engagement on the 2025/26 pay review body process.

To fully restore public services and address staffing crises, the government must demonstrate a long-term commitment to the public sector that extends beyond addressing immediate pay concerns. This entails enhancing public sector pay and working conditions through departmental-level negotiations with unions, while collaborating with public sector unions and employers to tackle strategic challenges faced by workers and the services they provide. We therefore recommend government:

1. Establish a Public Sector Workforce Commission: This commission, comprised of trade unions, employers, government and independent experts, should be tasked with developing a comprehensive, cross-government strategic plan to address urgent workforce challenges. The plan should serve as the foundation for departmental workforce strategies that should be jointly developed with unions in every area of the public sector.

2. Empower Departmental Machinery: Strengthen existing departmental structures and bargaining machinery to facilitate effective collaboration with unions on the development of fully funded workforce strategies. These strategies, implemented through collective agreement, will ensure departmental needs and worker concerns are effectively addressed, promoting the social partnership model unions advocate for. Workforce strategies should consider and address the needs of outsourced workers and identify strategic opportunities for insourcing.

3. Create a Public Sector Workforce Unit: A central unit within the heart of government, reporting directly to the Prime Minister, should be established to monitor the progress and impact of workforce strategies across departments. This unit should have the authority to hold departments accountable for strategy implementation, identify and resolve barriers, and ensure consistent progress towards workforce goals and alignment with wider governmental priorities.

4. Revitalise the Public Services Forum (PSF): This forum should provide a platform for ongoing dialogue between government, unions, and employers on long-term strategic challenges impacting public sector workers and service delivery. By fostering open communication and collaboration, the PSF will facilitate the development of effective, sustainable solutions, aligning with the call for greater union voice in strategic decision-making.

Pay setting in the public sector

Strong industrial relations are the cornerstone of effective pay determination. Between 2010 and 2024, the Conservative government systematically undervalued and neglected industrial relations and the public sector workforce, using the PRB process as a political football. As a result, we saw widespread industrial action in the years leading up to the general election.

In her statement on public spending inheritance, the Chancellor committed to “consider options to reform the timetable for responding to the Pay Review Bodies (PRB) in the future.” We welcome this commitment as a first step towards restoring trust in the pay review body process which is at an all-time low. Union concerns can be summarised as follows:

Lack of independence and government interference: PRBs are unduly influenced by government agendas.

Unequal weighting of evidence: Evidence from unions, employers, and the government do not carry equal weight in PRB decisions.

Rigidity and delays: The PRB process is inflexible, deadlines are missed, and pay awards are often delayed, causing hardship for workers and difficulties for employers.

We agree that a critical aspect of PRB reform involves establishing a fair and reasonable timetable that all parties must adhere to. Delays in pay awards, often caused by late submissions from government departments, have become a recurring issue. These delays have costly consequences for both workers and employers. Timely decisions are essential for workers' financial security and allow employers to plan their payroll budgets effectively.

A more balanced and equitable approach is necessary. PRBs should explore the possibility of multi-year pay deals, where appropriate, and building in adaptability to respond to unforeseen circumstances such as unexpected economic, social or health crisis such as the Covid-19 pandemic or periods of high inflation.

However, adjusting the timetable alone will not resolve the long-standing issues with PRBs. For instance, the piecemeal approach to devolution and lack of synchronisation between devolved funding decisions and the PRB timetable has complicated pay determination in devolved nations. In Wales, pay negotiations have still not started for the Agenda for Change workforce or teachers, despite the UK Government announcing the pay awards for both groups of workers on the 31 July 2024. Welsh government have pointed to the UK Government’s lack of clarity on whether there would be ‘Barnettised’ consequential funding for areas of devolved responsibility as the reason for the delay.

To address these concerns, restore trust and improve morale in the public sector, we recommend the Chancellor consider other aspects of the pay review body process. Fairness and impartiality should be the bedrock of the pay review body (PRB) process to instil trust and confidence amongst all stakeholders. The TUC recommend that pay review bodies and, where appropriate, the Office for Manpower Economics, should:

1. Strengthen stakeholder input: Allow for greater union involvement throughout the PRB recruitment and appointment process. Unions should be involved in preparing job specifications and form part of the recruitment panel. The Office for Manpower Economics, secretariat to the PRBs, should facilitate ongoing stakeholder feedback on board composition.

2. Diverse and representative boards: Appoint PRB members considering existing equality and diversity gaps, ensuring all viewpoints are represented, including those of the employee voice.

3. Independent process: PRBs should be autonomous and non-political. The PRB should begin proceedings each year, starting with a call for all three stakeholders – unions, government and employers – to submit evidence simultaneously. The government should not submit a remit letter separate from its evidence to the PRB, and the aspirations it sets out in its evidence should be given consideration alongside other factors.

4. Fair and transparent evidence: Conduct a comprehensive evidence gathering exercise, weighting all stakeholder evidence equally. PRBs should employ their own analysis of evidence and assess the impact of recommendations, including modelling the impact of their recommendations on workers with protected characteristics. Publish a transparent report with methodology and rationale behind weighting.

5. Broader considerations: In addition to recruitment and retention and affordability, PRBs should explicitly consider: longer-term pay trends for their respective workforce; rates of pay for comparator professions, including international professions; the long-term sustainability of services; and the impact of recommendations on service delivery. PRBs should consider each factor separately and not allow one feature to override others. The rationale for final recommendations should be fully explained in each of these regards.

6. Effective communication: Maintain open communication throughout, with regular updates. The PRB’s report and recommendations should be made public at the same time as they are delivered to government. This ensures all stakeholders have equal and timely access to information.

7. Timely process: Establish a clear and realistic timeline at the start of each year. Each PRB process should meet the needs of their respective pay rounds and bargaining group, and not be bound to other PRBs whose remit covers different bargaining groups. Once initiated, the process should continue without delay, even if a stakeholder misses deadlines. In exceptional circumstances, there should be a process to allow for mutually agreed adjustments to the timetable.

8. Devolved pay: Government and the Office for Manpower Economics should be clear about their approach to UK devolution, giving clarity over how they will manage and resource situations where pay for a particular PRB group is devolved/subject to devolved influence.

These recommendations are a starting point for strengthening and reforming the pay review bodies. PRBs should have a clear understanding of the role, functions, and priorities of any collective bargaining machinery in their respective sectors, and engage constructively with it.

Health and social care

Urgent action to tackle the acute recruitment and retention crisis in adult social care is critical to delivering quality care and support services for all who need them. Fixing the social care workforce crisis is also critical to address huge challenges in the NHS and tackle increasing economic inactivity. As the NHS Confederation highlights, adult social care and the NHS are ‘two sides of the same coin’ with social care workforce shortfalls having a significant knock-on effect on the NHS, with a long-term financial settlement critical to give long-overdue clarity and security to both sectors. 46

There is widespread consensus among the public, trade unions and experts that improving pay and conditions in social care is an essential first step towards fixing our broken social care system – recent polling shows that 77% of the public believe social care workers are underpaid.47

The TUC therefore welcomes the government’s commitments to implement a social care Fair Pay Agreement, create a National Care Service and take action towards improved and joined up health and social care workforce planning.

Aside from addressing poverty pay among care workers and helping ensure quality care service provision, investment in the social care workforce will generate significant economic returns. The TUC’s own analysis demonstrates that a sector-wide £15 per hour minimum wage would boost England’s economy by £7.7 billion, with the net cost substantially lower than upfront investment required given that the Treasury would benefit from higher tax returns and reduced in-work benefits payments, and from the economic impacts of the additional consumer spending.48 In addition, ensuring sufficient care and support would improve the employment prospects of disabled people and reduce the government’s carer’s allowance bill.50

Childcare

There is also a pressing need to improve access to affordable, accessible, flexible, high-quality childcare which enables families to work (especially women) and helps give children the best possible start in life.

The lack of affordable childcare puts significant financial strain on families, impacting parental, particularly maternal participation in the labour market. The UK has the second highest childcare costs among leading economies, and it is estimated that 1.7 million women are prevented from taking on more hours of paid work due to childcare issues 51 . Recent TUC research has found that women are nearly five times more likely to be out of the labour market due to caring responsibilities, this rises to six times more likely for BME women and nine times more likely for disabled women.

Skills and the economy

There is an urgent need to boost adult skills. Our economy demands a skilled workforce to navigate technological advancements, the green transition, and a constantly evolving global landscape. A decline in skills investment, participation and progression over the past 14 years has led to a skills crisis, harmed productivity and our economic wellbeing. Skills policy and decision making should be central to the government’s industrial strategy.

The TUC and our affiliated unions are committed to supporting the government’s ambitions to break down barriers to opportunity. We strongly advocate for reinstating the Union Learn Fund as a strategic initiative to achieve this objective.

For more than two decades, the Union Learning Fund secured a well-established reputation for reaching a broad spectrum of workers, particularly those who face limited access to conventional adult and workplace training programmes, supporting over 200,000 workers annually into learning and training. Unions played a pivotal role in facilitating employer match funding, demonstrating our unique capacity to bridge the gap between workers and employers.

By reinstating the £20 million Union Learning Fund we can significantly enhance basic and broader skill levels among the Department for Education’s priority groups. This investment is anticipated to yield a substantial economic return, comparable to previous funding cycles. For every £1 invested, we can expect a return of £12.87, with £7.56 accruing to individuals and £5.31 to employers. Considering associated costs, the total return on investment to HM Treasury would be approximately £3.60 for every £1 invested.

Social security

Working age benefits play an essential role in improving living standards and providing income security. The consequences for individuals and families of living in poverty and not having the resources to participate in everyday life, are far reaching.

The pandemic highlighted our broken sick pay system, and we support the government’s commitments to strengthen statutory sick pay (SSP).

Removing the income eligibility rules and waiting days for sick pay must happen at pace. Under current rules, employees would not qualify until they had been off for four days. Scrapping the three-day wait will mean that employees who are off for 1 to 3 days with a short illness will now get SSP. This will also boost the amount of SSP received for people who are off for longer than three days. Under the current system, an employee who typically works a five-day week receives just £46.70 if they’re off work for a week, as they’re only paid for two days. If the three-day wait is scrapped, they’ll get the full week’s payment of £116.75.

Scrapping the lower earnings limit will extend SSP to the 1.15 million employees who are not currently eligible due to being in work but not earning £123 per week (the lower earnings limit). The majority of those not eligible (69 per cent) are women.

We recognise that scrapping the lower earnings limit without wider policy action could, however create a situation where some employees would be better off on SSP than their usual wage. The TUC believes that this could be resolved by paying SSP at the usual rate, or the employee’s usual earnings, whichever is lowest. This would mean that no employee is better off on SSP, while also ensuring that low paid workers are not losing money when off sick. This would be similar to the system used for Statutory Maternity Pay (SMP), with mums receiving the lower of the SMP rate or 90% of their average earnings between the 7th and 33rd week of maternity leave.

Along with removing waiting days and the income eligibility threshold, the level of SSP must also rise. It is currently paid at £116.75 per week, which is just 18 per cent of the average weekly wage. The UK’s statutory sick pay is incredibly by low by international standards. OECD analysis at the start of the pandemic found it to be the lowest in any OECD country.

We also welcome the government’s recognition that Universal Credit needs to be reformed. The TUC has long campaigned on the need to address persistent policy failures in the design of Universal Credit. Our report A Replacement for Universal Credit sets out the breadth of reform that is needed, including proposals for non-digital application options, removal of the five week wait, and more regular payments and assessment periods.

The government’s opportunity mission sets out its commitment to breaking down the barriers to opportunity for every child, and the social security system has an important role to play in achieving this ambition as well as addressing poverty across the life course. After years of Conservative cuts, a system that was already towards the low end of generosity internationally has fallen further behind. So to support the government with rebuilding our social security system we have proposed the establishment of a new time-limited opportunity commission, which could seek to set short and medium-term priorities for social security spending, and to evidence the social and economic benefits that would accrue from different measures. We also support immediate action to remove the two-child limit which restricts access to Universal Credit to the first two children in a family.

Pensions

We welcome the government’s swift action in meeting its manifesto commitment to launch a review the pension system to provide greater security in retirement. Extending auto-enrolment (AE) to bring more people into the workplace pension system, and increasing the level of saving by raising minimum employer contribution rates needs to be central to this review. At present, 38-43% of working age people are not on track to meet the Target Replacement Rate retirement incomes set out in the Pensions Review.52

The 2017 Automatic enrolment review has already set out the first steps of lowering the AE age threshold from 22 to 18 and removing the Lower Earnings Limit so that contributions are calculated from the first pound of earnings. We believe these long-delayed measures, contained in the Pensions (Extension of Automatic Enrolment) Bill 2023, should be implemented as soon as possible.

The review should then focus on the £10,000 earnings threshold that excludes low-paid workers from workplace pensions – including many with multiple part-time jobs – and setting out a timetable to increase minimum contribution rates. The TUC believes the earnings threshold should be phased out, while a combined employer and employee contribution of 15% should be the target contribution, with two-thirds of this coming from the employer. As well as providing greater security for workers in retirement, these measures would significantly boost the government’s commitment to increase investment in the UK. Analysis has found that even increasing contribution rates from 8% to 12% would generate and extra £10bn a year in contributions to be invested.53

Employment support

As our analysis has set out, economic inactivity due to ill health, and growing youth unemployment, are major challenges facing our jobs market. The economic and human impacts of failing to act will be severe.

We support the recent announcement of the Government’s Back to Work Plan, along with recognition that support is required for those out of work rather than blame. As plans develop. It will be important that they are evidence-based and deliver meaningful interventions. For young people, we know that real experience of real work can be a decisive factor in enabling them to enter and progress in the job market. We also know that job guarantee schemes work. Evaluation of The Future Jobs Fund, introduced by the last government, showed the scheme delivered clear benefits for participants, employers and society. And these schemes are common across Europe.

Involving unions in the development of the Back to Work Plan will also be key. Unions represent millions of working people in hundreds of sectors across public, private and not-for-profit sectors. As experts in the world of work, unions should be considered key stakeholders when it comes to planning such schemes.

A higher minimum wage

We welcome the government’s commitment to make the minimum wage a genuine living wage and commitments to remove discriminatory age bands.

The TUC believes that the minimum wage should be at least £15 an hour, delivered through a minimum wage target set at 75 per cent of median wages. As this target is tied to median wages, it is important that this is underpinned by good general wage growth.

The government has already made positive changes to this year’s Low Pay Commission (LPC) remit by removing the previous government’s instruction that the minimum wage should be held at 66 per cent of median wages. Instead, the LPC has been entrusted to make a recommendation based on the evidence.

In future years the government should re-introduce an ambitious target set at 75 per cent of median wages. This is the best way to deliver increases to the minimum wage. Since 2016 the minimum wage has had an explicit target set by government at a percentage of median wages. The first target was set at 60 per cent of median wages by 2020, and the second was set at 66 per cent by 2024. Minimum wages have grown more quickly since targets were introduced, and both targets have been delivered without causing negative employment effects. This has strengthened the case that higher minimum wages are achievable. We should continue testing the boundaries of minimum wage policy with ambitious targets. We should not let up on the progress we are making.

Young people face the same cost of living pressures as other adult workers. The government is right to commit to ending discriminatory age bands in the minimum wage. This should be delivered as quickly as possible through the Low Pay Commission.

In recent years youth rates have fallen behind the main rate. When the minimum wage was introduced in 1999, 18-20 year olds were paid 83 per cent of the main rate and this was maintained until 2010, but by 2024 it has fallen behind to just 75 per cent. This trend needs to be reversed.

The evidence shows that most employers do not use the youth rates. Coverage is just 8 per cent for 18-20 year olds and 10 per cent for 16-17 year olds. Removing youth rates would level the playing field for good employers.

Fairer taxes

The provision of investment and high-quality public services relies on the fair taxation of people and companies. But the UK is taking proportionately less tax than our neighbouring countries, and those with the broadest shoulders can afford to pay more. Currently, income earned through working is generally taxed at a higher rate than income from investments or assets. It is time for a rebalancing of taxation away from work towards wealth.

Who pays tax, and how much they contribute, are political choices with direct impacts for our essential public services and our wider infrastructure. The government has made a good start: VAT on private school fees, crackdowns on tax loopholes for non-doms and private equity, levelling the playing field between on-line multinationals and high street retailers, and increased funding for HMRC.

To deliver the revenues our country needs, the TUC also proposes wider measures including:

Increasing capital gains tax rates to bring them into line with income tax, to generate an extra £10bn into the Treasury, to fund public services and public sector pay. Recent TUC polling found that around 3 in 4 (72%) think capital gains should be taxed at the same or higher than income tax.54

Reversing Conservative cuts to the bank levy and bank surcharge would raise £15 billion over 4 years.55

Closing inheritance tax loopholes, including allowances for agricultural and business land, and special treatment of AIM shares. These exemptions have meant that the average effective tax rate of estates valued at over £10 million is only 17%. It has been estimated that removing the business relief on inheritance tax for shares in small and medium sized businesses would raise £1.1 billion annually, and capping reliefs for agricultural and business land would raise £1.4 billion annually.56

Applying National Insurance to investment income so that all income is taxed at the same level.

Progress towards international tax cooperation including through a UN Convention.57

Further investment in HMRC is also vital to effectively tackle tax avoidance and evasion. HMRC has estimated that the tax gap – the difference between tax owed and tax collected – is almost £40 billion.58

Investment in HMRC now will deliver a substantial and direct return.

- 36 For example, the IFS analysis of the failures of the past decade immediately pivots to the productivity failure: https://x.com/TheIFS/status/1797613540804894907.

- 37 https://www.tuc.org.uk/sites/default/files/productivitypuzzle.pdf; see also: Bill Martin and Robert Rowthorn (2012) ‘Is the British economy supply constrained II? A renewed critique of productivity pessimism’, Centre for Business Research, University of Cambridge, May.

- 38 When last year the IMF acknowledged "On average, fiscal consolidations do not reduce [public] debt-to-GDP ratios" (World Economic Outlook, April 2023), this was in effect a recognition of the failure of austerity policies across the globe.

- 39 https://www.tuc.org.uk/news/uk-economy-has-missed-out-ps400bn-growth-under-conservative-government-2010; https://www.tuc.org.uk/research-analysis/reports/growth-plan-puts-work-wealth

- 40 TUC (2024). Falling behind on labour rights: Worker protections in the UK compared to the rest of the Organisation for Economic Co-operation and Development (OECD): www.tuc.org.uk/research-analysis/reports/falling-behind-labour-rights

- 41 OECD (Organization for Economic Cooperation and Development). 2018. “Good Jobs for All in a Changing World of Work: The OECD Jobs Strategy.”

- 42 Deakin, S. and Pourkermani, K. (April 2024) The economic effects of changes in labour laws: new evidence for the UK, Digital Futures at Work Research Centre

- 43 https://www.ippr.org/media-office/clear-majority-of-employers-support-governments-proposals-to-strengthen-rights-for-workers-polling-finds

- 44 TUC (2021). TUC action plan to reform labour market enforcement: https://www.tuc.org.uk/research-analysis/reports/tuc-action-plan-reform-labour-market-enforcement

- 45 Dowd, H. (3 October 2023). Employment tribunal backlog: the impact on businesses, People Management: www.peoplemanagement.co.uk/article/1839454/employment-tribunal-backlog-….

- 46 NHS Confederation. 2023. Adult social care and the NHS: two sides of the same coin | NHS Confederation

- 47 Hemmings N, Allen L, Lobont C, Burale H, Thorlby R, Alderwick H and Curry N. From ambition to reality. National policy options to improve care worker pay in England. The Health Foundation and Nuffield Trust; 2024. From ambition to reality: national policy options to improve care worker pay in England - The Health Foundation

- 48 TUC. 2023. £15 minimum wage for care workers would boost England’s economy by £7.7 billion. £15 minimum wage for care workers would boost England’s economy by £7.7 billion | TUC

Other economic analysis shows multiple positive returns to investing in a properly funded care system – by supporting people aged 50-64, currently unable to work because of caring responsibilities, to return to the labour market, with an increase of just 1% in the 50-64 age bracket ‘in work’ rate boosting GDP by around £5.7bn per year.

Future Social Care Coalition. 2024. Carenomics: Unlocking the economic power of care. Carenomics Report - Future Social Care Coalition - 50 Future Social Care Coalition. 2024. Carenomics: Unlocking the economic power of care. Carenomics Report - Future Social Care Coalition

- 51 https://wbg.org.uk/wp-content/uploads/2022/03/Childcare-and-gender-PBB-Spring-2022-1.pdf

- 52 https://www.gov.uk/government/statistics/analysis-of-future-pension-incomes/analysis-of-future-pension-incomes

- 53 https://www.thephoenixgroup.com/news-views/10-billion-annual-pension-contribution-boost-possible-from-increasing-the-auto-enrolment-minimum-to-12/

- 54 https://www.tuc.org.uk/news/we-must-end-grotesque-inequality-tory-era-tuc

- 55 https://www.tuc.org.uk/research-analysis/reports/bank-taxation

- 56 https://ifs.org.uk/articles/raising-revenue-closing-inheritance-tax-loopholes

- 57 https://www.ituc-csi.org/ITUC-welcomes-UN-progress-toward-international-tax-cooperation

- 58 https://taxjustice.uk/blog/40-billion-lost-to-the-tax-gap/

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox