A growth plan that puts work before wealth

The Conservatives have led us into a situation where we face the longest recession for 100 years. And there are now widespread reports that the government are planning to slash public services, pay and social security in their upcoming fiscal statement.

But government has a choice. Will it repeat the disastrous and self-defeating errors of George Osborne, that hammered workers while rewarding the wealthy? Or will it put the needs of workers first with a plan for growth.

This short briefing sets out why the Chancellor can and must take an approach that puts work before wealth.

- The country faces the longest recession in a century. The government looks set to choose to make working people pay, with a million job losses as well as yet more cuts to real pay.

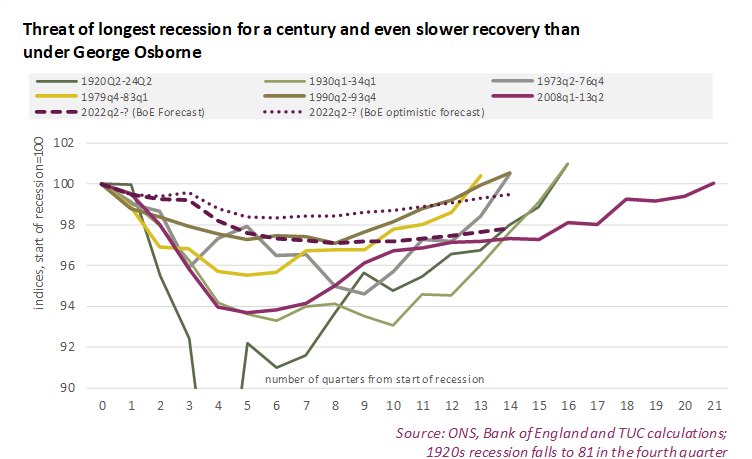

The Bank of England have warned of a recession longer than any other this century (see press conference here), as the chart indicates – with the low point coming after those for all other recessions (though basically matching the mid-1970s). Unlike previous recessions, the economy is not expected to be back to where we started in the coming three and a half years (the end of the Bank of England’s forecast).

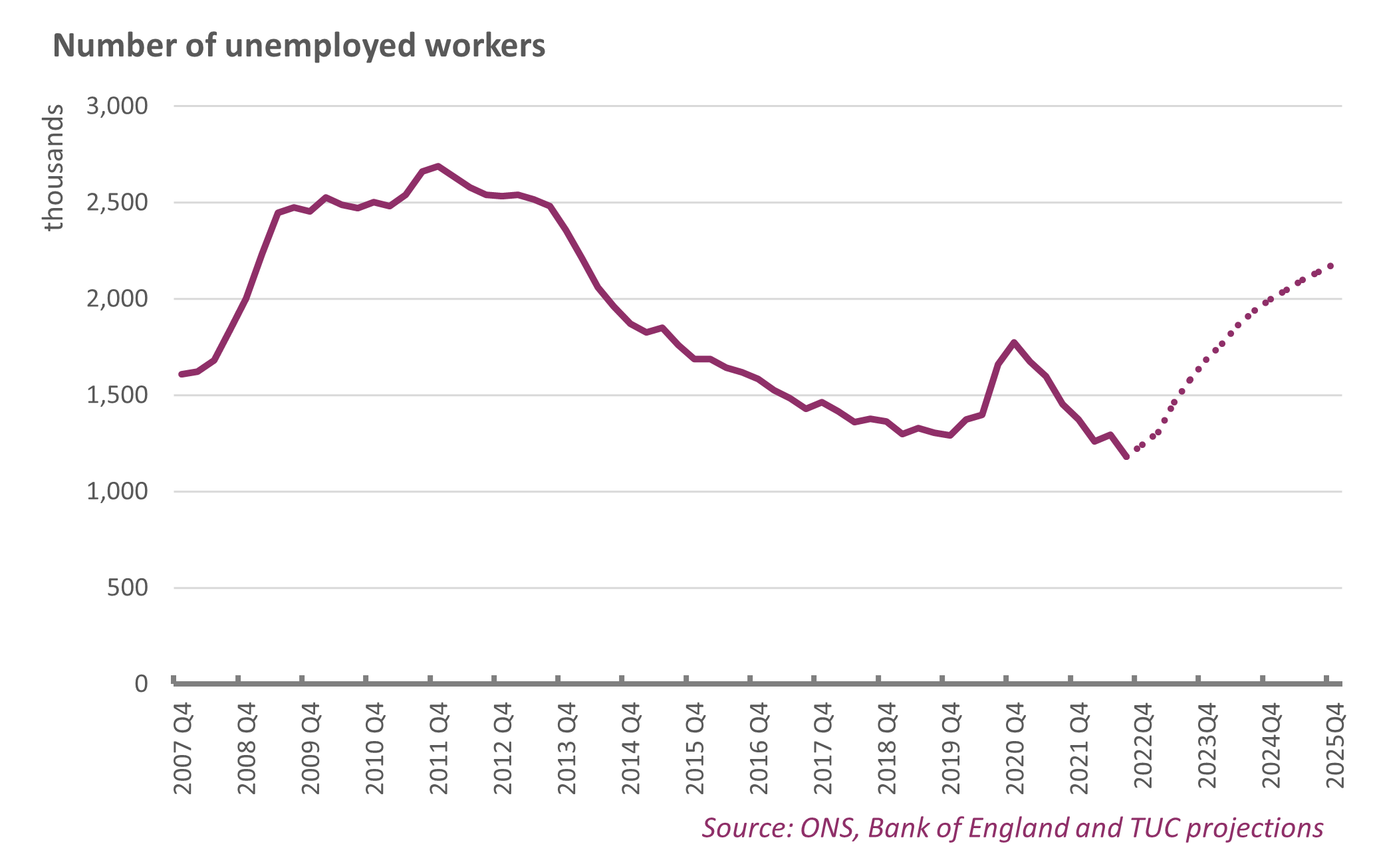

The Bank of England’s headline scenario puts unemployment on an upward trajectory to 2.2 million at the end of 2025, up from 1.2 million now.

- Rather than address the recession, Rishi Sunak and Jeremy Hunt appear to have given up on growing the economy and we are facing more of the same disastrously failed Tory economics. Government must take action to avoid a deep recession that will damage working people.

Rather than setting out a plan to tackle the recession, prior to the Autumn Statement Rishi Sunak and Jeremy Hunt, the Chancellor, have indicated that they plan deep cuts to public services, and real terms cuts to pay, pensions and benefits, in order to meet a self-imposed fiscal rule that says that the debt to GDP ratio must be falling by a defined year of the forecast period. This self-imposed rule risks leading the government to repeat the mistakes of George Osborne. Andy Verity of the BBC (based on analysis from economists Dr Jo Michell and Dr Rob Calvert Jump) reports how any claimed black hole “disappears entirely” under different definitions and better projections for growth and interest rates. In fact the economists rightly consider the idea of a 'fiscal black hole’ a ‘dangerous fiction’.

- Refusing to act is a political choice, not an economic necessity. As we saw through the austerity decade, cutting pay and public services makes workers poorer and economic growth weaker.

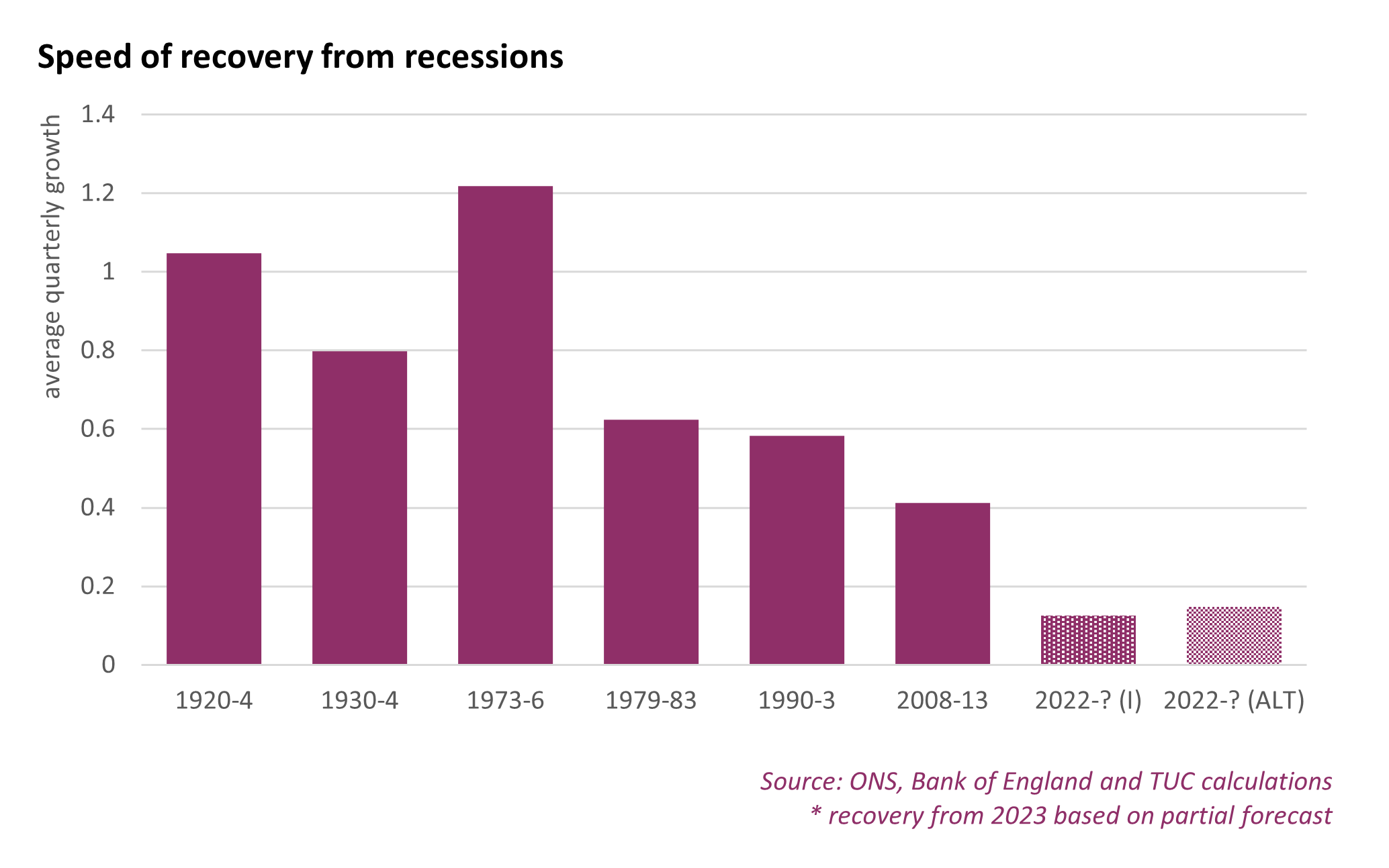

GDP data in the first chart show that the recovery from the 2007-09 recession (caused by the financial crisis) under George Osborne, who was chancellor from 2010 to 2016, and imposed deep cuts in public spending, was the slowest of all recoveries this century, by a long way. In fact before Osborne the average speed of recovery was 0.9 per cent a quarter, under Osborne it was under half that at 0.4 per cent a quarter. (Osborne was not in office throughout the whole of the recovery, but as is clear from the first chart he inherited an economy recovering at a good pace from Labour, and proceeded to slow growth to a near standstill.)

The Bank of England forecast the recovery from the present recession at a stunningly slow pace of between 0.1 and 0.15 per cent per quarter. This would be a sixth of the average speed before Osborne.

- Giving up on growth will mean making the public finances even more fragile.

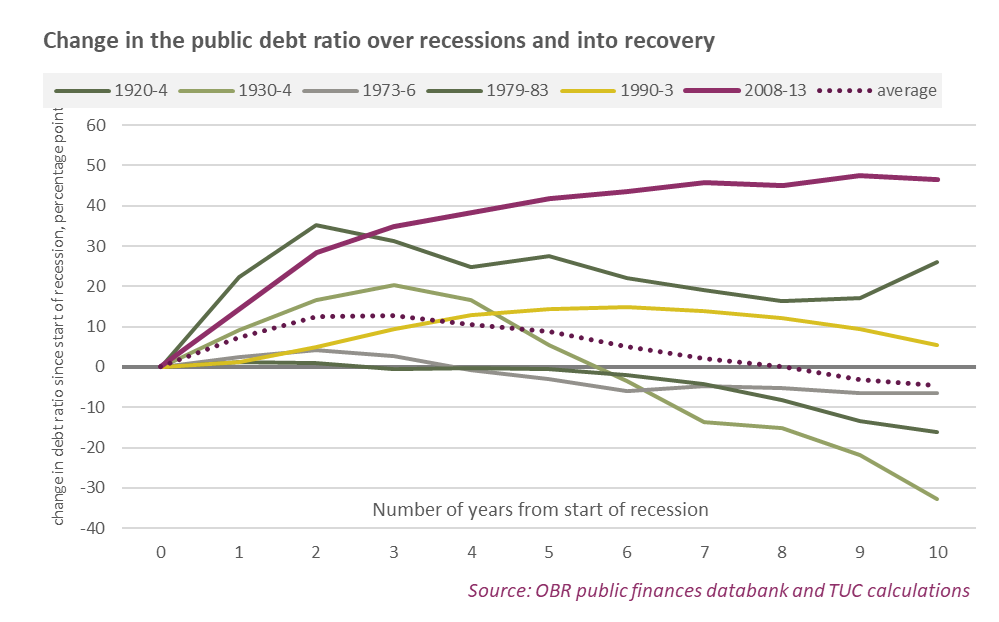

The decade of austerity did not repair the public finances, as the slower economic growth led to lower tax receipts for government. The ‘black hole’ that we should be talking about is in the economy – not in the public finances. George Osborne’s slowest recovery for a century meant the public finances deteriorated far more significantly than under any recession this century.

The chart below shows that in in most recessions this century the public debt ratio is on an improving trajectory on average after around three years. George Osborne’s policies prevented any improvement in public debt, as slow economic growth outweighed the impact of any spending reductions, and meant that ten years after the start of the recession debt was still up by 45 percentage points of GDP compared with the start of the recession. The average after ten years across all other recessions was for the public debt ratio to be 5 percentage points of GDP below the starting point.

Under Osborne the public debt ended up worse by 50 percentage points of GDP more than the average performance over the past century – in today’s money that’s more than £ one trillion.

- We’re in the longest wage squeeze since Napoleonic times, and our public services are crumbling. Meanwhile the wealthy have got even wealthier and companies are making windfall profits.

Research by the new economics foundation for the TUC shows an additional £43bn will be needed in the Autumn Budget just to ensure spending on public service stays the same in real terms, and pay keeps pace with CPI inflation. Funding shortfalls include £15.7 billon on health, £7.1 billion on education, £900 million on justice and £400m on environment food and rural affairs.

And as Frances O’Grady warned in her speech to the TUC Congress this year, Britain is on course for two decades of lost living standards, with pay still below the 2008 level in real terms and the squeeze forecast to last twenty years in total.

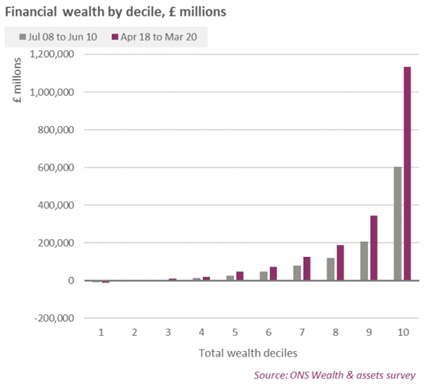

In the meantime TUC research shows dividends have been growing at three times the pace of nominal pay, when ahead of the global financial crisis they were only growing at two times pay growth. Likewise total financial wealth over 2008-10 to 2018-20 increased by around £0.9tn (80 per cent) from £1.1tn to £1.9tn. Some 61% of the increase went to the top decile, the (already almost insignificant) financial wealth of the lowest five deciles increased by only 3.7%.

- In the face of cost inflation originating overseas, tax changes and government action is a less blunt instrument than interest rate rises.

We know that rising food and other costs are placing huge stresses on workers. But they should not be forced to pay the price for this in terms of unemployment, and reduced wage growth that takes us even further away from where we were a decade ago.

Many firms can afford to raise wages without raising prices if they are prepared to accept lower profit margins and dividend pay outs. In this crisis, it should be the wealthy who pay their share rather than workers. Protecting those struggling simply to buy food and heat their homes will not increase inflationary pressures.

We need a plan to protect workers and grow the economy sustainably

- With food, energy and housing bills still high, we need a plan to share these costs fairly. That means more support for working households, while making sure the rich pay their fair share.

- And above all we now need a credible plan to grow the economy. That doesn’t come from tax cuts for the rich, but from a plan for investment in the services and infrastructure needs, and for decent work that puts money in people’s pockets. That's what will give workers, business and markets confidence in the UK economy.

- We have to have a new approach this time that puts first workers not wealth. That means

- Protecting workers through inflation beating rises in benefits, pensions, the minimum wage and public sector pay

- Protecting our public services and investment in the urgent necessity of tackling climate change. Public services require at least £43bn just to deal with the impacts of inflation and as this year has shown us more clearly than ever, we urgently need to be rolling out a rapid programme of home insulation and rapidly scaling up investment into a secure net zero carbon energy mix

- Taxing wealth and windfalls with a plan to equalise Capital Gains Tax and income tax rates, and to increase windfall taxes on those who have profited from the gas crisis, both to protect against inflation and so that those who have done so well from the past decade pay their fair share.

- And a review of policymaking institutions and processes that appear to have given too much priority to the interests of the city, finance and the powerful, and too little to those who work too hard for too little.

These proposals are spelt out more fully in our submission ahead of the last Conservative budget in September: On the side of working people.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox