A new deal: TUC statement on the spending review

UK economic growth is now among the weakest of all major economies. The global revival that supported the economy after the referendum has retreated, and there are growing fears of global recession, Uncertainties as a result of the Brexit process leaves the UK particularly vulnerable. In the first half of 2019, GDP growth was lower than the UK in only Mexico and Italy.

Weak growth is a consequence of the government’s own decisions including prolonged austerity and the continued threat of a no-deal Brexit. But there is nothing inevitable about Britain’s weak economy. Investment in the skills and infrastructure Britain needs to transition to a cleaner fairer more productive economy would also boost economic growth and deliver better jobs.

The situation we face: a decade of weak growth

For the whole of the past decade, UK economic growth has been significantly weaker than long-term norms, with a further downwards step-change since the referendum. Since 2010 annual growth has reduced by a third, averaging 1.9 per cent compared to annual growth of 2.9 per cent ahead of the crisis. Growth in 2019 is weaker still. Quarterly figures are so far distorted by developments related to the original Brexit date of 31 March, in particular stockpiling and changed timing of closures in motor vehicle manufacturers. While GDP fell by 0.2 per cent in quarter two, this followed a erratically high rise of 0.5 per cent in quarter one; the Governor of the Bank of England expects “stagnant” (i.e. zero growth) into Q3.[1] Four quarter growth into quarter two is 1.2 per cent, and was last lower at the high of austerity in 2012.

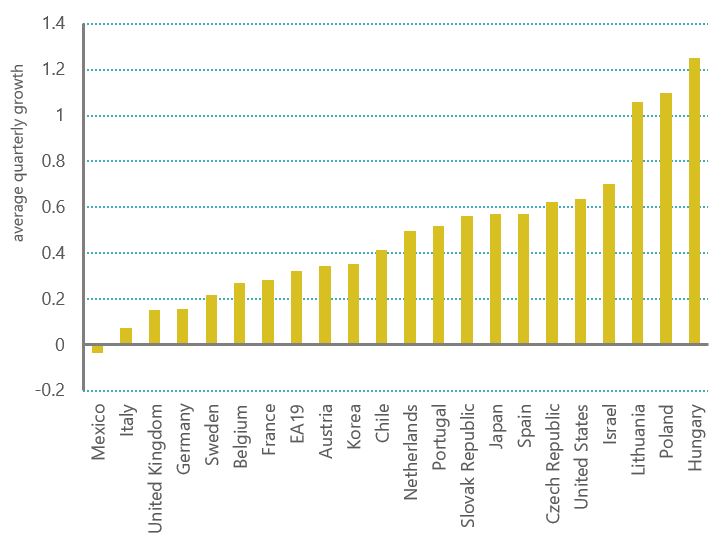

The UK performance in 2019 amounts to one of the weakest of all advanced economies. The chart below shows average quarterly growth across the first two quarters of the year: at less than 0.2 per cent, UK quarterly growth is well below the average of 0.5 per cent and third from last in the overall ranking (of countries available so far).

[1] ‘The Growing Challenges for Monetary Policy in the current International Monetary and Financial System’, speech at the Jackson Hole Symposium, 23 August 2019

Average quarterly GDP growth in the first half of 2019

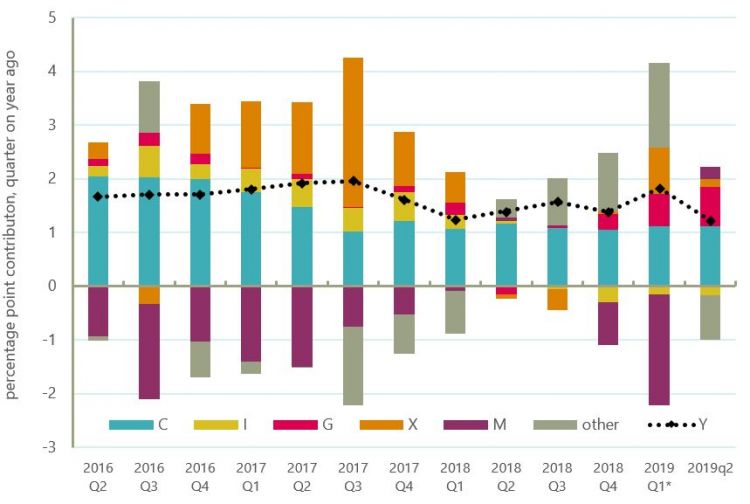

The following chart shows how the composition of (steadily lower) growth has shifted.

- Stronger export growth (X, orange) particularly over 2017 has evaporated from 2018 Q2.

- Household consumption (C, turquoise) has weakened since the middle of 2017 when higher inflation (driven by the fall in het exchange rate) kicked in

- Into Q3 2018 weak investment growth (I, yellow) became negative investment growth.

- Over the last three quarters, government spending (G, crimson) has supported activity; to this point such support was conspicuous by its absence.

Expenditure measure of GDP, contributions to four quarter growth

As we set out above, a no deal Brexit would pose an immediate threat to the economy.

This weak growth is in large part a consequence of a decade of austerity, which damaged growth and inhibited improvements in the public sector finances. .

The coalition government inherited an economy that was recovering from the global financial crisis: increased GDP meant increased government receipts and so a turnaround in the public finances.

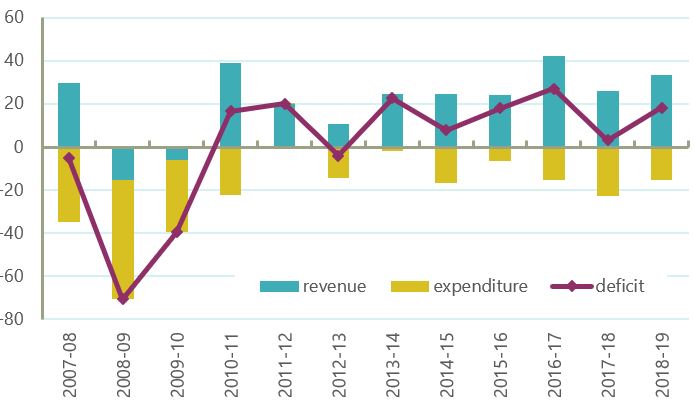

The following chart shows how the annual change in the deficit (public sector net borrowing) is made up of changed government revenues and expenditure (yellow: in this accounting presentation, scoring as negative). The worsening public finances during the global recession reflected a collapse in revenues rather than greatly increased expenditures. The improved finances in 2010-11 were then caused by a vigorous revival in government revenues not a reduction in government expenditure. The initial severity of austerity policies threatened to terminate both the recovery in GDP and the public finances, with revenue gains greatly down over 2011-12 and 2012-13. With austerity moderated (and wider monetary stimulus) revenues began to pick up again.

Changes in public finances, £ billion

But even in moderated form, austerity policies have continued greatly to contain economic growth throughout the coalition and the conservative governments. This has been increasingly problematic since the referendum as other sources of growth have faded. With weak growth sustained for a decade, improvements in the public finances have fallen greatly short of original plans.

The most obvious measure of the shortfall in terms of revenues is the public sector debt which is now reckoned to have peaked in 2016-17 at 85 per cent of GDP (£1.8tn) when it was originally expected to peak in 2013-14 at 70 per cent of GDP (£1.2tn).

Not least since the referendum, the government has failed to deliver a strategy that prioritises growth and the economy.

Rebuilding Britain: a new approach

The first step for the government must be to rule out a no-deal Brexit which would damage economic growth and find a solution to the Brexit crisis which protects jobs, rights and peace in Northern Ireland.

But a change of approach more broadly is needed to deliver a stronger economy that can secure greater jobs and wages across the country. As we set out above, the government’s approach to austerity has held back growth. And we show below how more funds are desperately needed to deliver stronger public services.

Government must also invest in the modern infrastructure we need to deliver the transition to a cleaner economy, and meet the commitment to net zero carbon emissions by 2050.

Raising UK public investment from 2.7% to the OECD average of 3.5% of GDP, so that the UK has the infrastructure needed to attract business and create well-paid jobs would require a £15bn boost to spending.

- As a first step, the Chancellor should set out a plan to raise investment to the OECD average, and show how this will be used to help meet the target of net zero emissions.

This transition to a cleaner economy can deliver better jobs, including in the places where they’re needed most. But this won’t happen automatically. Government needs to ensure a just transition including by:

- Setting up a cross-party commission on long-term energy and energy usage strategy, involving affected workers, unions, industries and consumers, to plan a path that will deliver a just transition to a clean, affordable and reliable energy supply for the future alongside reductions in emissions. As part of its remit, this commission should carry out a study of the social impacts of such a transition, its regional impacts and necessary mitigation measures.

- Using its procurement powers to ensure that jobs generated benefit workers in the local community and throughout the supply chain. It must also insist that jobs created provide workers with trade union recognition, and that employers have fair recruitment, industrial relations and pay policies for all workers. Companies winning government contracts must adhere to agreed standards of corporate behaviour; for example, contracts should not go to companies based in tax havens and companies must be registered in and pay tax in the UK.

Government must also invest in a major upgrade of Britain’s skills infrastructure.

Under-investment in adult learning and skills by government and employers has been a perennial and depressing feature of the UK labour market for many years. The scale of the skills crisis is growing apace due to the legacy of this under-investment and the major challenges arising out of the impacts of automation, Brexit and other significant trends.

Investment in Further Education (FE) and adult skills has declined dramatically. According to the Augar Review total government spending fell by 45% in real terms between 2009/10 and 2017/18 and there has been a 35% reduction in the number of adult learners during the latest 5 years.

Not surprisingly we compare very poorly with other European countries on adult skills, e.g., 40% of our 25-year olds do not progress beyond GCSE (or vocational equivalent) skills level.

There has also been a long-term decline in employer-led training with one research study[1] showing that the total volume of training halved between the end of the 1990s and the beginning of the current decade. The TUC commissioned Professor Francis Green of UCL to update this analysis. His new research[2], drawing on analysis of Labour Force Survey data, finds that the volume of workplace training fell by a further 10% between 2011 and 2018.

However, for some groups facing the brunt of an increasingly precarious and insecure jobs market, the rate of decline has been much greater. For example, since 2011 the amount of training that workers with the lowest-level qualifications (below GCSE/Level 2) are accessing has declined by 20% and for younger workers aged 16-34 the reduction was 16%.

There are a number of policy recommendations in the Augar Review that the TUC supports and which we believe would go some way to empowering more people to achieve an adequate skills level or to retrain for new jobs and careers. These include proposals to: establish skills entitlements for all adults to attain their first Level 2 and 3 qualifications; provide more maintenance grants and bursaries to lower-income FE students; increase operational and capital funding for colleges; and, deliver a new deal for the FE workforce.

While these recommendations are a good starting point and should be taken forward by government, the TUC is of the view that the challenges confronting us require a much more ambitious approach. In addition to a major funding boost for FE adult skills, we are calling on the government to:

- Set an ambition to increase investment in both workforce and out of work training to the EU average within the next five years

- Introduce a comprehensive package of adult skills entitlements that could be accessed through an expanded National Retraining Scheme and the introduction of lifelong learning accounts

- Give workers an entitlement to a mid-life skills/career review to consider their employment and skills trajectory going forward

- Reform the existing right to request time to train so that it is transformed into a new strengthened entitlement to paid time off for education and training.

[1] Green, F. et al (2016) “The Declining Volume of Workers’ Training in Britain”, British Journal of Industrial Relations, vol. 54 (2)

[2] Green, F. and Henseke, G. (2019) Training Trends in Britain, TUC (unionlearn research paper, no. 22)

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox