As GDP evaporates, the need is for a pre-emptive boost to demand

Last week the FT reported that officials were considering measures that might boost the economy after Brexit. But it’s clear that even before we get to Brexit the economy needs an urgent boost in demand.

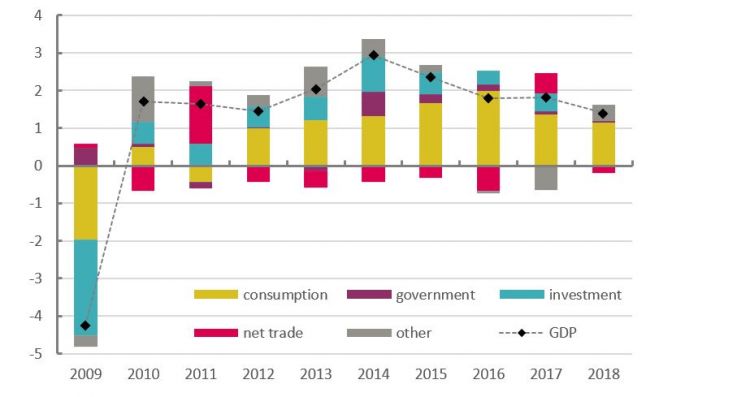

GDP

Quarterly GDP growth was only 0.2 per cent in 2018Q4. For 2018 as a whole growth was 1.4 per cent, the weakest figure since the economy was in recession in 2009 – as on the chart below.

Expenditure breakdown of GDP growth, percentage points

Global conditions

In 2017 UK GDP was supported by a revival in the global economy – in part as policymakers pumped still more money into the system. So, on the chart above, net trade (in crimson) was a significant upward factor. But in the second half of 2018 – in part as a result of policymakers withdrawing support for the economy (by tightening interest rates and in the US reversing quantitative easing) – financial markets freaked out and the global economy spluttered (see fuller discussion here). The support to the UK from trade turned negative, investment ground to a halt and we were left relying as usual on the consumer (in yellow - with the associated dangers from debt).

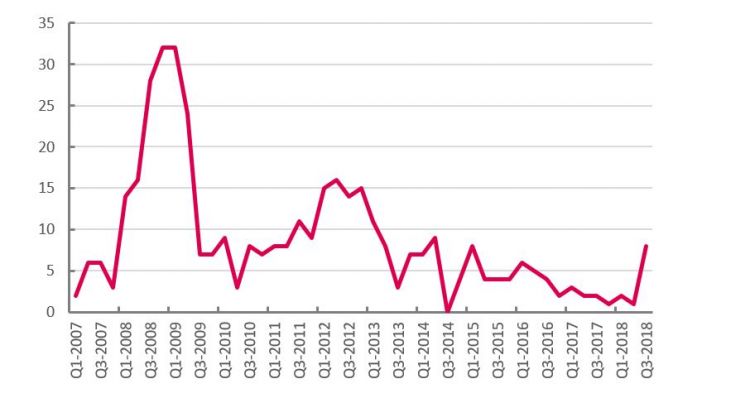

In the third quarter of 2018, eight OECD countries showed negative quarterly GDP – up from between one and three over the previous two years and the highest number for around four years.

Count of OECD countries with negative quarterly GDP growth

We are only just beginning to get readings for Q4: and we now know Italy is in recession, Argentina (outside the OECD) was already in recession, and Germany and Turkey are highly likely to be.

Last year the Bank of England were dismissing the weak Q1 reading as a result of bad weather. They expected growth of 1.8% for both 2018 and 2019 – 2018 is now at 1.4% and they now expect growth in 2019 to be a dismal 1.2%.

Ever since austerity we have become conditioned to a new normal of seriously weak growth, but we are now staring in the face of even worse. As the FT reported last week the Treasury are looking at boosting spending to support the economy after Brexit– though the advocates of austerity are still pushing back. But whatever happens with Brexit, weak growth in the UK in the context of a weak global economy means the government need to act now. The spring statement should be used to announce a significant boost to public sector pay, public services and infrastructure spending.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox