Government minister in denial over record household debt

Following the release of TUC figures on Monday that showed average unsecured debt has now reached an eye-watering £15,400 per household, today Labour MP Laura Pidcock challenged the government to explain what it is doing to address the growing debt crisis.

Given the scale of these debts, she justly called for a real minimum wage of £10 an hour and a return to serious collective bargaining for workers in the UK

In response Claire Perry MP, a minister in the department for Business, Energy and Industrial Strategy, claimed that our analysis had been “entirely discredited” because it includes student debt, “which is not something that accrues to every household”.

She went on to say that if student debt was stripped out “then you see that the growth of consumer credit has actually slowed”.

Certainly I am not aware of any substantive challenge to our analysis (beyond a commentary in the ‘continental telegraph’*).

And it’s not a valid complaint to say something should be excluded simply because it doesn’t accrue to every household – for example, the RPI includes cigarettes even though most people don’t smoke.

The role of student loans has been more widely commented on. But student debt is still debt – and it has to be repaid from income that is barely growing.

If anything, the analysis illustrates just how alarming the role of growing student debt has become – especially the sharp uptick in the trend for recent years.

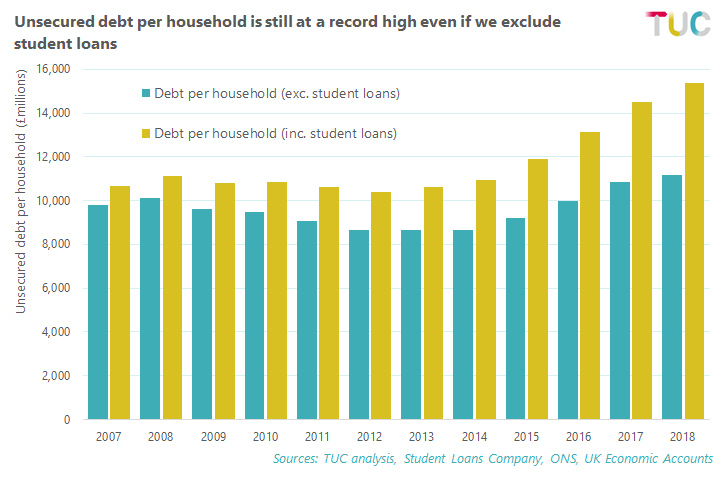

And even if we remove student debt (with figures from the student loan company ), the headline figure of debt per household is still at an all-time peak:

And student debt is still a long way below half of all unsecured debt

House of Commons library research published before Christmas demonstrated a more granular breakdown.

While the numbers are calculated differently (per individual rather than household and excluding those without any personal debts), they show debt per individual is £12,500. Excluding student loans it is £9,600 – hardly a trivial amount either.

But then what of the Minister’s claim that the expansion of consumer credit “has actually slowed”?

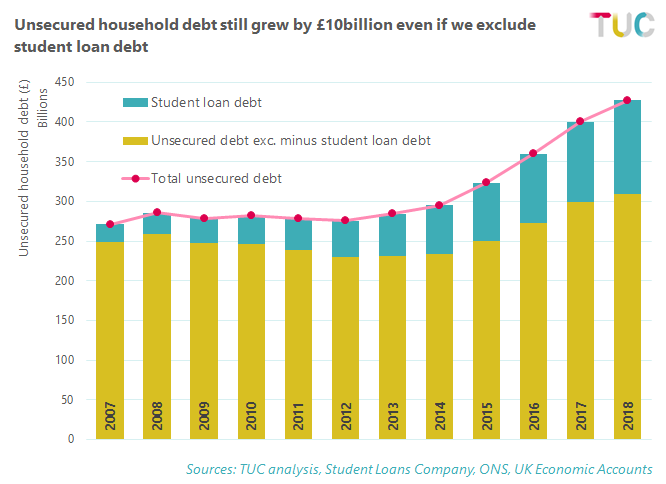

Excluding student debt unsecured borrowing was still up £10bn this year, smaller than the very sharp rise of £26bn last year. So it has slowed, but so what?

£10bn is still a big rise. And for many – not least the poorest – the damage has already been done.

Just last year the BBC reported National Audit Office analysis that 8.3 million people were struggling with personal debt in the UK. Unsurprisingly, this also leads to “anxiety and depression, which adds to NHS costs”.

And while the Treasury has formal responsibility for managing these debts, NAO head Amyas Morse said at the time that it “needs a better understanding of the scale of people's debt problems and how it is impacting their lives and the taxpayer so it can effectively resolve the problem”.

Well the message hasn’t got through to the minister, who appealed only to existing increases in the minimum wage.

The penultimate word should go to Governor of the Bank of England Mark Carney. In an interview to mark the 10th anniversary of the global financial crisis, he identified household debt as the first of four ongoing risks to the financial system.

Yet it’s hardly surprising that the minister is denial, because the Tory masterplan to wean the economy off debt than has failed disastrously.

Instead austerity has destroyed the economy, caused the worst pay crisis in two centuries, and forced millions of people into the red to just get by.

Sorry minister, but Laura Pidcock is most definitely right.

(*FWIW there is an error in the continental telegraph commentary. The claim that non-student loan debt is rising by only 2.6% is based on an illegitimate comparison of the cash increase in consumer credit against the stock of consumer credit and student loans.)

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox