TUC submission Autumn Budget 2025

An inheritance of failure

The UK faces an unprecedented set of economic and social challenges: years of poor growth, falling living standards and decimated public services. The drivers include reckless reductions in public capital investment and public service spending; a bad Brexit deal; and a lack of any genuine industrial or labour market policy under the previous Conservative government.

As a result, the Conservatives presided over under-performing labour market, which is still holding back millions of people’s lives and opportunities – as well as depressing growth.

Workers endured the worst pay crisis for two centuries, accompanied by a damaging rise in highly insecure work. Chronic under-investment hollowed out Britain’s industrial communities and too many young people left school without a route to a decent job. Rising numbers of disabled people who could work found themselves without support to do so.

Significant public services cuts were regressive, with those on the lowest incomes seeing the most significant drops in their living standards as services fell away.

The Tories’ disastrous failure also meant a steep increase in public debt. Coupled with high interest rates, government interest payments have risen very steeply.

Investing in change

A commitment of £325bn on government capital spending and public services investment has started to repair damage the last government caused. But while these important improvements are welcome, they are not sufficient. More investment not less is needed to put the UK economy on a firmer footing and to repair our public services.

Capital investment commitments must be protected, and thought should now be given to how they can be further expanded – including ensuring the National Wealth Fund has powers to borrow.

It is welcome that our trading relationship with Europe has begun to improve, and the TUC supports government ambitions to secure commitments in the Common Understanding as soon as possible.

While policymakers continue to misjudge a failure of demand for a failure of supply, the operation of the fiscal institutions the government inherited, in an internationally volatile climate, does place real constraints on what can be borrowed to invest now. So significant action is needed to raise revenues.

Now is the time to address historic imbalances in how labour and capital are taxed. This should include a significant increase in the bank surcharge, further substantial capital gains tax reform and increased taxation on gambling companies. A fairer balance of taxation would raise significant revenues to support the investment and public services spending that will underpin future productivity gains, and protect the incomes of working people whose consumption is also essential for secure growth.

The government must also ensure that its approach to managing the public finances in the longer-term is conducive to securing strong, sustained output gains – an independent commission should now be established to consider how the processes for managing our public finances should continue to evolve, considering best international practice as well as recent UK outcomes.

Raising living standards

In this challenging context, faith in government’s capacity to deliver change is extremely low. After years of life getting harder, frustration with the pace of change is high.

The country is in desperate need of repair and renewal. And while the last 12 months have starkly shown that there are no quick fixes or easy answers an ambitious approach is now needed to securing change that is seen and felt in daily lives.

The living standards crisis has not gone away – it remains the most significant issue facing working people across the country. Real pay is still barely advanced on 2008, despite some small gains over the past year. While around 30 per cent of the public do now report that the pressure on their household budgets is easing, most (58 per cent) do not.1

After the most severe living standards pressures on historic record, it is no surprise that most people’s budgets feel much tighter than they used to. The government must now be relentless in showing working people it is on their side and that it is doing all it can to help families bring down their costs and increase their incomes.

Taking measures in the service of working people’s incomes is not just essential to delivering on a mandate for change, but the right way to rebuild our economy. A focus on stronger growth and rising living standards must go hand in hand.

The UK needs to break free from its persistent recent cycle of stagnant GDP and falling real household incomes. While higher GDP per head is needed to secure more better jobs and higher wages, rising consumer incomes and subsequent higher spending also make an important ongoing contribution to our economic health. Economic policy must simultaneously target both stronger output and rising living standards.

So immediate action must be taken to help working people with the cost of living, including introduction of measures to bring down domestic energy costs, an end to the two-child benefit cap and ongoing ambition on the minimum wage.

A joined-up labour market policy should also be central to the government’s approach - focusing consistently on more and better jobs.

Young people, taking their crucial first steps into paid work at the end of full-time education, have finally been promised a guarantee of quality training or a decent first job. This must be ambitious scheme, with early access for those who need it most. We also need to invest more in learning, prioritising expansion of the Growth and Skills Levy and a new union learning fund to boost union-employer partnerships.

Full implementation of the employment rights bill, and the wider plan to Make Work Pay, are an essential part of the job quality agenda and will also support stronger growth. Our assessment suggests that the employment rights bill alone will improve job security for millions of workers and delivering annual net economic gains of around £10bn a year. As the Bill gains Royal Assent it must now be delivered at pace, ensuring working people see real benefit from the changes it brings and that the economic gains it can deliver are fully felt.

The new industrial strategy has started to deliver investment and futureproof our manufacturing base, while boosting our capacity to compete for the new industries of tomorrow. More action can now be taken to ensure there are strong workforce strategies in place across each sector. This approach can be carried across to significant infrastructure investments, where employers and unions should be supported by government to secure framework agreements across significant infrastructure projects, promoting secure jobs and high labour standards.

Support is also needed across foundation industries to ensure competitive industrial electricity prices – this should include bringing forward the British Industrial Competitiveness Scheme or failing that introducing an interim support scheme to be available to industry on the brink of closure due to energy costs. Additional funding and investment is also needed to futureproof North Sea supply chain firms and deliver a successful workforce redeployment programme for jobs at risk.

Decent public services play a vital role in boosting productivity, growth and living standards – whether through improving the nation’s health, boosting educational performance or ensuring that people with caring responsibilities are able to work. It is therefore vital that investment in the world class public services we need is sustained, and that there is active dialogue with public service unions on a plan to restore public sector pay, recognising that more than a decade of pay restraint has exacerbated the recruitment and retention crises across much of the public sector and the financial hardship faced by many public services workers.

Investing in our infrastructure, skills and public services is not just the right thing to do for individual workers, but to deliver the environment in which growth can thrive. More and better jobs across our country, together with action to tackle the cost-of-living crisis, are the best way to deliver a more secure, productive economy. A government that delivers for working people will be one that can deliver the repair, renewal and growth the country desperately needs.

- 1TUC polling August 2025, undertaken by Hold-Sway, n=5024.

The urgent need for change

- The government took power amidst unprecedented economic and social challenges

- The country is facing simultaneous failures on growth, living standards, (across measures of job quality and employment rates as well as wages), post-Brexit trade, investment and public services.

- The living standards crisis has not gone away – it remains the most significant issue facing working people across the country.

- The government is right to target both stronger growth and rising living standards – both goals are mutually supportive.

- Chronic under-investment has hollowed out Britain’s industrial communities, and too many young people are leaving school without a route to a decent job or secure future.

- Public service performance went consistently backwards, and Tory failures on growth meant they also failed on public debt.

The UK faces an unprecedented set of economic and social challenges – years of poor growth, falling living standards and decimated public services.

We do know that stronger growth and rising living standards must go hand in hand. The UK needs to break free from its persistent recent cycle of stagnant GDP and falling real household incomes. While higher GDP per head is needed to secure more better jobs and higher wages, rising consumer incomes and subsequent higher spending also make an important ongoing contribution to our economic health. The government is right focus their growth mission on achieving both rising real household disposable incomes and higher GDP per head2 : economic policy must simultaneously target both stronger output and rising living standards.

Evidence shows us that change is possible, and that progress has already started. But the failures inherited from the Tories have been worsened by ongoing and strong headwinds from abroad and at home. Conservative failures to reduce public debt, coupled with high interest rates, are acting as a severe restraint to private and public sector activity.

A crisis of growth and living standards

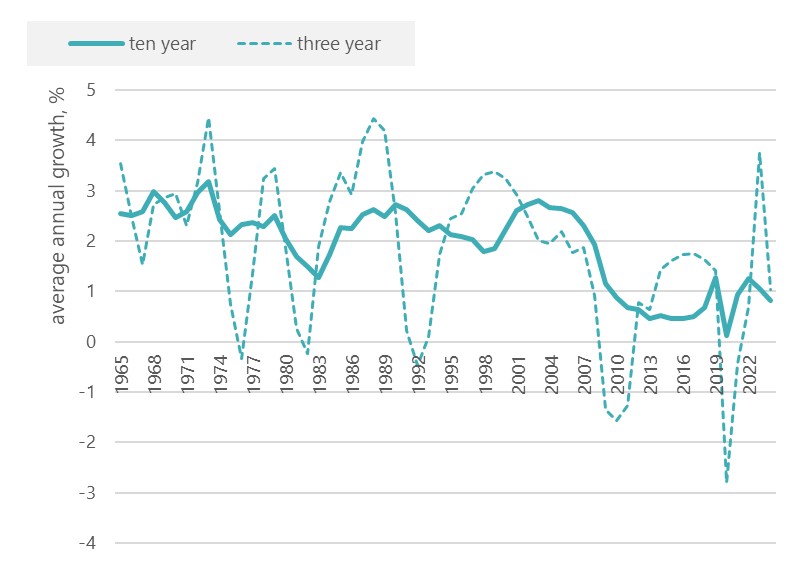

Following the financial crisis, output per head saw a dramatic fall. After a small improvement pre-pandemic, the post-covid period saw further falls. Average annual growth of GDP per head has only been one per cent over the last three years.

Chart 1: GDP per head growth, moving averages

At the same time, under the Tories workers endured the worst pay crisis for two centuries.3 Average weekly earnings adjusted for inflation show that real pay grew by an average of just 0.04 per cent a year between May 2010 and April 2024. Overall, real pay growth averaged a welcome 3.1 percent over the last (financial) year, but it has fallen back more recently as inflation picked up with bills rising into the new financial year (discussed in more detail below). Real average weekly pay remains up by only £9 (1.4 per cent) on the 2008 peak. Had pay instead grown in line with the pre-global financial crisis trends since January 2008, average weekly earnings would now be £298 per week higher.

Chart 2: level of real pay, July 2025 (CPI) prices

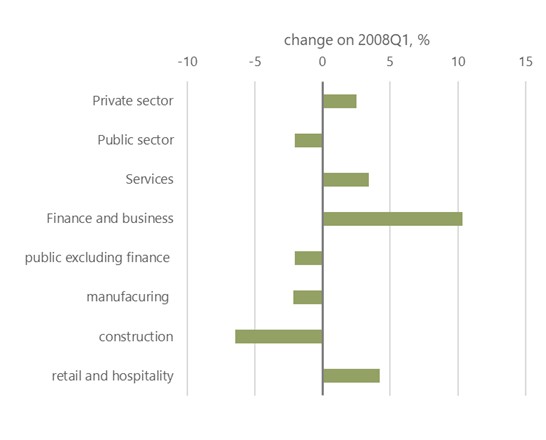

For many workers the reality is even worse, with real pay still below the 2008 level. While finance and business services are now seeing real pay 10 per cent above 2008, hospitality is up by a lower 4 per cent (and from a very low base). Workers’ standard of living in other vital industries has still gone backwards, not least those in manufacturing, construction and the public sector. The living standards crisis has not gone away – it remains the most significant issue facing working people across the country.

Chart 3: industry change in real pay since the global financial crisis (CPI basis)

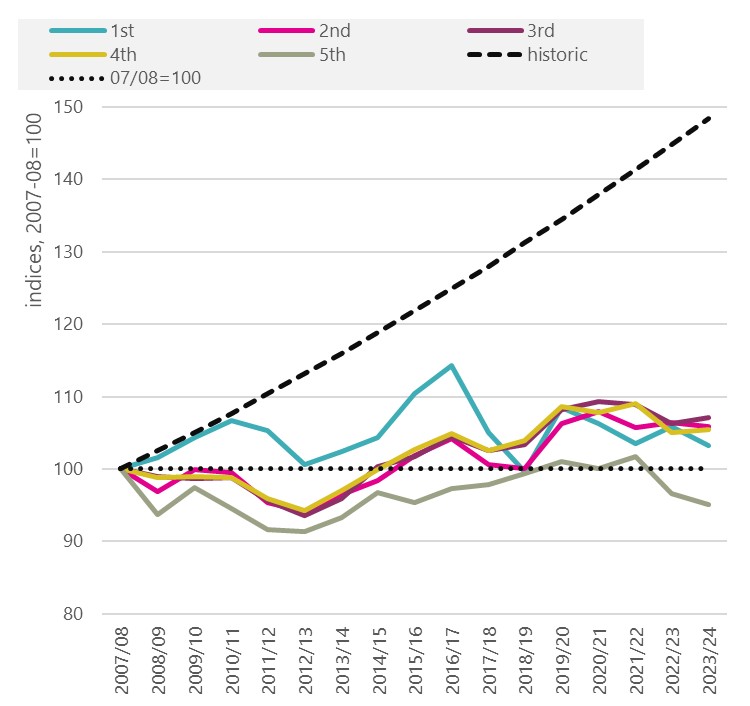

While of great importance, real pay figures also only provide a partial picture of incomes, and do not cover the whole population. ONS figures for the disposable income of individuals include self-employed and retired people and consider taxes and benefits. Chart 4 shows some gains ahead of the pandemic, but real incomes then falling for all quintiles over the last three years under the Tories (the data extend to 2023-24). As with pay, incomes have fallen disastrously short of the pre-financial crisis trend.

Chart 4: median real household disposable income by income quintile

Labour market underperformance

At the same time, the quality of work has deteriorated. TUC analysis has shown that in 2024 there were four million people in insecure work, up from 3.2 million in 2011. As a share of the workforce, insecure work grew to 11.7 from 10.7 per cent.

The increase in insecure work has been disproportionate to the rise in the employment level: insecure work grew by 25 percent compared to 15 percent employment growth (table 5).

Table 5: Insecure work 2011 and 2024

| 2011 | 2024 | Change from 2011-2024 | |

| Numbers in insecure work (16 +) | 3.2 million | 4 million | +25 percent |

| Employment Levels (16 +) | 29.4 million | 33.9 million | +15 percent |

Source: TUC analysis of Labour Force Survey and Family Resources Survey4

Insecure work has an enormous effect on people at work. The prospect of having work offered or cancelled at short notice makes it hard to budget household bills, plan wider life and meet caring responsibilities. Insecure work is also low paid in comparison to permanent employment, leaving many insecure workers struggling financially.

Another Tory legacy is the rising numbers of young people not in Education, Employment or Training (NEET). The latest NEET data shows 873,000 18–24-year-olds are NEET, 948,000 if 16-18 year olds are included. This total been rising since mid-2021 and peaked in October to December 2024, the highest it had ever been since the end of 2014.

Chart 6 shows, compared to the early 2010s where NEET numbers were driven more by young people who were unemployed, NEET young people are now increasingly economically inactive, reporting that they are both out of work and not seeking it. Of the 873,000 18–24-year-olds who are NEET; 330,000 are unemployed (38 per cent) and 543,000 (63 per cent) are economically inactive.

Chart 6: Neet composition of 18–24-year-olds, UK, by unemployment and inactivity.

- 4‘The scale of insecure work in the UK’: insecureworkbriefing2025.pdf

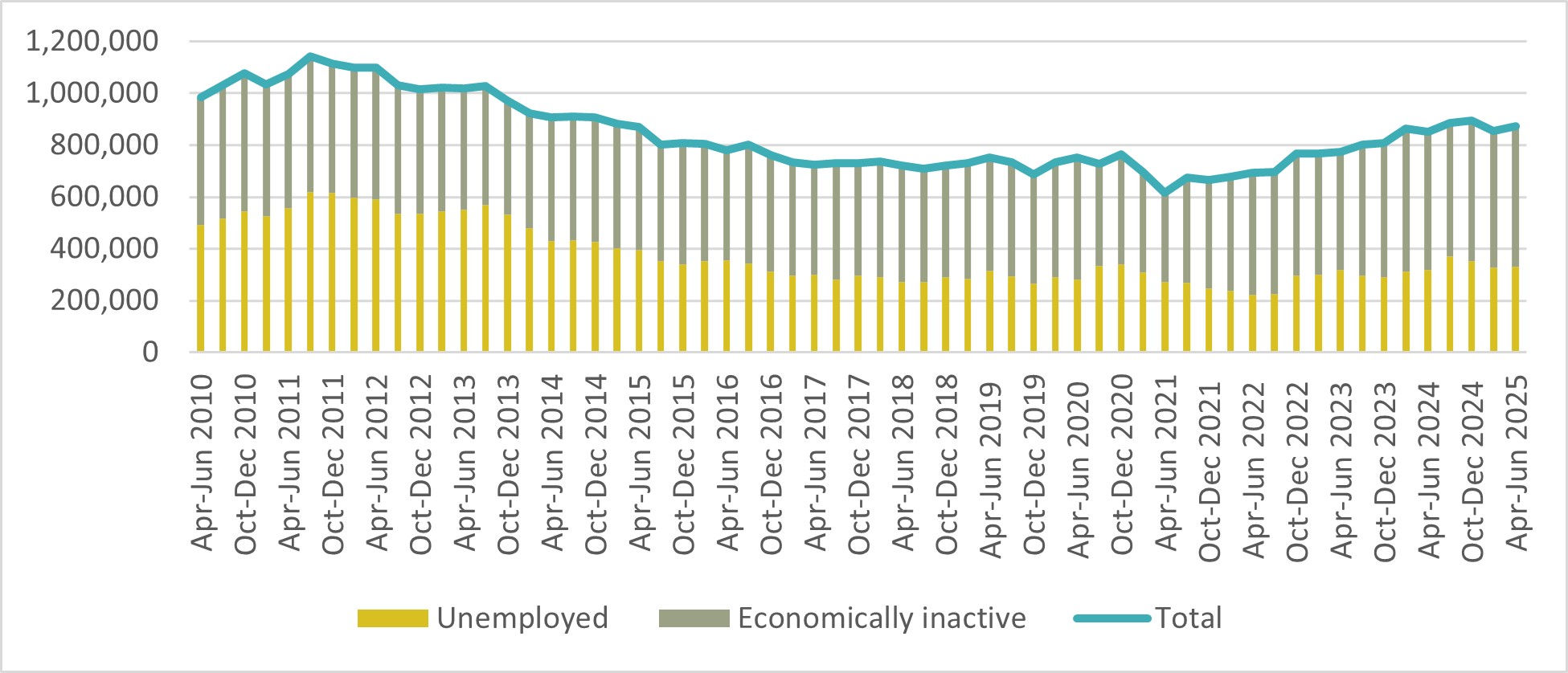

Economic inactivity has also risen for the working population as a whole. Ahead of the pandemic, 2.11 million were inactive due to long term sickness – a total that now stands at 2.79 million, down very slightly from a peak of 2.86 million at the end of 2023. Evidence shows that increased flows from work into inactivity are an important driver of this trend.5

Negative impacts of Brexit

Workers continue to suffer from the damage caused by the Conservatives’ bad Brexit deal which has had a severe negative impact on the UK economy and businesses. Between 2021 and 2023, exports to the EU were down 27 per cent and imported goods down 32 per cent.6 The National Audit Office reports that the annual estimated cost to business of completing customs declarations required by leaving the EU stands at £7.5 billion while it cost taxpayers £4.7 billion to set up new border and customs arrangements. 7

The Office for Budget Responsibility (OBR) has provided a detailed analysis of the potential growth impact of Brexit on the UK economy. They have concluded that Brexit will reduce long-run productivity by 4 percent relative to remaining in the EU. 8

Leaving the EU had a severe negative impact specifically on investment. Haskel and Martin (2023) estimate it lowered investment by 10 per cent9 while other studies suggest that with the current agreement with the EU investment will fall by 32 per cent by 2035.10 This has been driven in part by the loss of the European Investment Bank which, among other areas, supported investment in manufacturing and clean energy.

Investment failures

Growth has been further held back by Conservative failures on capital investment. Upon taking office, the Conservatives immediately cut public infrastructure spending, at a time when the recovery inherited from the Labour government was still fragile. In 2018, TUC analysis showed UK investment third from bottom of all OECD countries, and coming in the bottom half of OECD countries for all broad categories of investment.11 The IPPR has shown business investment “ranking a lowly 28th among 31 OECD countries”, and the lowest in the G7 for three years running to 2022. 12

Public sector net investment averaged only 1.8 per cent of GDP over 2010-11 to 2014-15 (chart 7). The figures spiked momentarily during the pandemic at 3.4 per cent of GDP. But afterwards the Conservatives planned for a gradual fall to 1.7 per cent – the joint second lowest figure in 25 years.

Chart 7: Public sector net investment, % GDP

- 5Resolution Foundation, July 2025: Opening-doors.pdf

- 6‘Unbound: UK Trade post-Brexit', Jun Du, Xingyi Liu, Oleksandr Shepotylo and Yujie Shi, 2024:https://www.aston.ac.uk/sites/default/files/2024-09/Full%20Report.pdf

- 7National Audit Office, ‘The UK border: Implementing an effective trade border, 2024: https://www.nao.org.uk/wp-content/uploads/2024/05/the-uk-border-impleme…

- 8Brexit analysis - Office for Budget Responsibility; last updated July 2025.

- 9https://www.economicsobservatory.com/how-has-brexit-affected-business-i…

- 10Cambridge Economics, January 2024: https://www.camecon.com/case-studies/greater-london-authority-impacts-o…

- 11https://www.tuc.org.uk/blogs/uk-third-bottom-global-investment-league

- 12’Rock bottom: low investment in the UK economy’, June 2024: https://www.ippr.org/articles/rock-bottom

Capital investment is critical to economic capacity and to growth prospects into the future. Investment failures of the past 15 years have meant weaker economic growth, weaker revenues and so have further damaged the public finances. Moreover, the IPPR have recently argued there are critical synergies between the private and public sector: “the consensus on investment is shifting – public investment can crowd in business investment”. 13 At the Labour Party 2025 conference, the Chancellor reiterated the point:

- 13Rock bottom

I have never believed the Tory mantra that the best thing that a government can do is to get out of the way. A strategic state must use its power to support jobs and growth – and that includes public investment. Under the Tories, capital spending was always the first victim when the public finances came under pressure. So, in last autumn’s Budget, I changed those fiscal rules – to support and to protect investments.

We urgently need a reset that ensures strong and sustained growth in both public and private investment outcomes.

Chronic under-investment and chaotic industrial policy-making led to deindustrialisation. Foundation manufacturing sectors and supply chains were offshored, while the UK struggled to attract new high-tech, advanced manufacturing or clean power manufacturing operations. The overall and steep decline in manufacturing as a share of the economy continued; chart 8 compares the UK with the average for all advanced economies.

Chart 8: Manufacturing as a share of GDP

Under the Conservatives, the government’s policy aimed for a climate transition that prioritised public investment-backed technology development and manufacture in other countries, with the UK’s role as a consumer of technology. For example, in offshore wind the UK’s leadership in deployment was associated with a failure to deliver jobs and domestic economic benefit.

Public services failures

Spending on public services was also decimated under the Conservatives. These simultaneous cuts in infrastructure and wider public spending were disastrous for services in their own right, and also held back the economy and therefore created further pressure on public debt. By 2018-19 the widely used real terms per head measure showed departmental spending down 15 per cent from £6,700 to £5,745. After an increase during the pandemic, spending was cut back sharply again and for 2024-25 was projected still to be 5 per cent below the 2009-10 position.

These cuts were severely regressive. For example, analysis by Landman Economics of the impact of planned cuts for the 2015-2020 parliament showed “The average reduction in living standards as a result of all the modelled tax, transfer and public spending measures is around 13 percent for the bottom decile and around 11 percent for the second and third decile. Meanwhile, for the top decile the average change in living standards are close to zero”. 15

The cumulative loss over the past 15 years has been immense. In July 2024, as the Labour government took office, an Institute for Government report set out “...that the government’s inheritance on public services is extremely precarious. Most services are performing worse now than they were in 2010 or before the pandemic. The government’s status quo spending plans from April 2025 onwards will likely mean that all services other than general practice, hospitals and schools could be performing worse in 2027/28 than in 2010" 16

Public finance failures

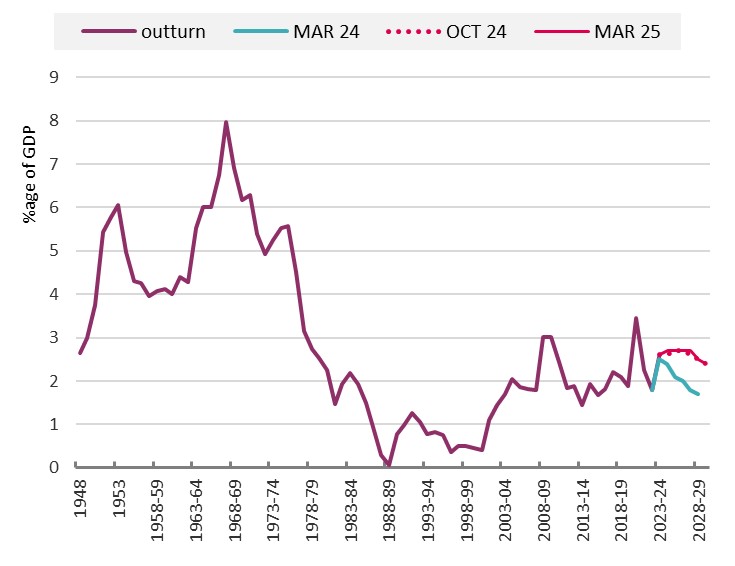

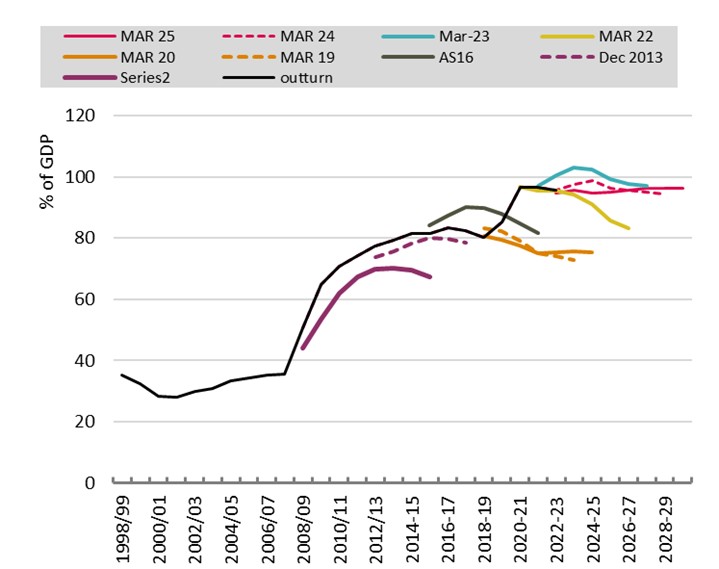

Sustained failures on growth have also had significant impacts for public debt. With our economy so much smaller than anticipated, government revenues have fallen below forecast and our debt has increased as a proportion of GDP. Chart 9 shows badly the Conservatives failed against meeting the targets they set themselves in June 2010.

The plan was to reduce public sector net debt as a share of GDP to 67 per cent by 2015-16. But instead in their March 2024 forecast the OBR reckoned the ratio to be 98.8 per cent of GDP in 2024-25. While the latter figure has obviously been affected by the pandemic, TUC analysis showed the failure on public debt ahead of the pandemic the worst in at least a hundred years.17 In March 2025 the OBR judged that public sector net debt will be at 96.1 per cent of GDP in 2029-30.

Chart 9: Public sector net debt

- 15March 2016: https://www.tuc.org.uk/sites/default/files/Spending-cuts-Report.pdf

- 16’Fixing public services: Priorities for the new Labour government’: Fixing public services | Institute for Government https://www.instituteforgovernment.org.uk/publication/fixing-public-ser…

- 17The Conservatives are presiding over the worst period of economic growth since the 1920s | TUC https://www.tuc.org.uk/news/tuc-conservatives-are-presiding-over-worst-…

This failure continues further to constrain the actions of the current government going forwards, with the position even more challenging given the steep rise in interest costs (discussed in further detail below).

Starting to rebuild Britain - in challenging times

- The country is in desperate need of change and national renewal – and the government has started to deliver change.

- Important commitments on government capital spending and public services investment have started to repair the damage of 14 years of Conservative failure.

- Public sector net investment is now set to rise to 2.7 per cent over 2024-25 to 27-2028. Real departmental spending per head is set to rise to 3.0 per cent above the 2009-10 level in 2029-30.

- Maintaining and building on these commitments in the years ahead will be vital to sustaining growth and boosting living standards.

- Our relationship with Europe has also begun to improve. But although government action is supporting growth, a challenging international context is holding our economy back.

- Consumer demand is depressed and is also pressing down on output.

- High interest rates are holding back growth, and the case for further cuts is strong.

- High interest rates are also impacting the public finances and holding back spending, as the higher Bank rate feeds through to the borrowing costs of government – which are significant given the debt burden inherited from the Tories.

The country is in desperate need of repair and renewal – and the government has started to deliver change. But the last 12 months have starkly shown that there are no quick fixes or easy answers. We still face significant challenges, the scale of which has become starkly clear over the last year. Budget 2025 must now take this formidable task on.

Capital spending boosted

At the 2024 Autumn Budget the government boosted public service and public investment by £326bn – the biggest real terms increase since the 2000 spending review. 18

The increase in government investment spending is shown as a share of GDP on chart 7 above. Rather than falling to 1.7 per cent in 2029-30 (as the Conservatives planned), the latest assessments show public sector net investment is now set to rise to 2.7 per cent over 2024-25 to 27-2028. Chart 10 shows the OBR assessment in gross, cash terms – the rise in investment since 2023-24 totals a cumulative £110bn. The Institute for government pinpoints the beneficiaries: “... big increases in investment spending for energy and net zero, transport, and business – in support of [Reeves’s] missions to grow the economy and decarbonise the energy system – as well as defence”.19

Chart 10: General Government gross fixed capital formation, £ billion

- 18Chancellor provides £326 billion boost to public services and investment, funded by the biggest tax rises on record and higher borrowing • Resolution Foundation https://www.resolutionfoundation.org/press-releases/chancellor-provides…

- 19https://www.instituteforgovernment.org.uk/comment/spending-review-2025

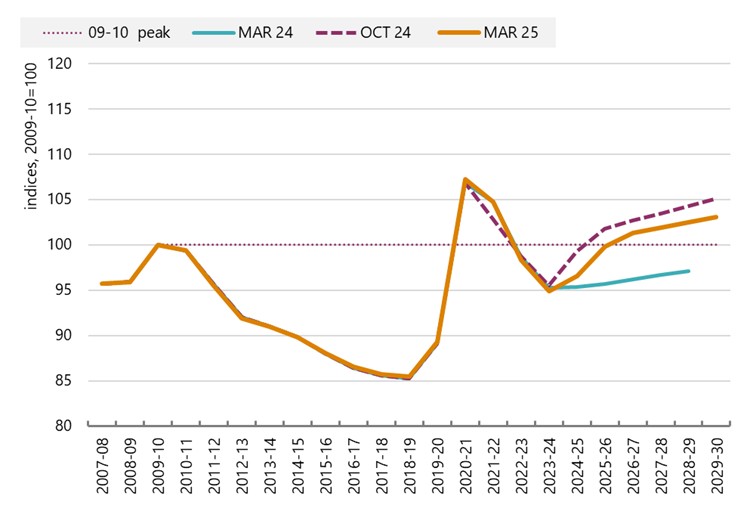

Public service improvements, although more investment needed

Public services spending was decimated under the Tories. Chart 11 shows a decline of 15 per cent on the real terms per head measure, and the further slump in spending the Conservatives planned following the pandemic. The latter meant a renewed decline to 5 per cent below the 2009-10 position.

Under the current government real departmental spending per head is set to rise to 3.0 per cent above the 2009-10 level in 2029-30. The International Monetary Fund has confirmed the government was right to raise revenues to support this investment.

The authorities’ fiscal plans strike a good balance between supporting growth and safeguarding fiscal sustainability. The new spending plans are credible and growth-friendly, taking account of pressures on public services and investment needs. They are expected to provide an economic boost over the medium term that outweighs the impact of higher taxation. As revenue is projected to increase, deficits are set to decline and stabilize net debt.

Chart 11: Real departmental spending per head, 2009-10=100

In the context of poor growth, public spending is also supporting jobs. Payrolls figures show private sector jobs falling from the start of 2024, but the declines offset by gains in public sector employment.

Current spending increases are also badly needed, but they do fall short of the full investment necessary to turn services around and drive improvements. Current spending has been focused on health, which has meant smaller real terms increase in education and other departments.21

After years of real terms falls and freezes, public sector pay awards in 2025 were broadly in line with inflation (when announced), building on the above-inflation pay awards in 2024 and helping to reduce the gap between public and private sector pay growth.22 Welcome steps have also been taken to put the Pay Review Body timetable back on track, so that many public service workers will start to receive their pay awards on time within this parliament. This will provide clarity and certainty to workers about the timings of pay awards, as well as minimising the risk of administrative issues and complications arising from interactions with social security payments and increases to the national minimum wage (NMW). The start of talks to negotiate structural changes to the Agenda for Change contract are also welcome, and NHS unions have been clear that the promised funding must cover the agreed outcomes in full.

But workforce recruitment and retention challenges remain endemic across much of the public sector, albeit with some evidence to show that high vacancy rates are abating. As of the end of June 2025, there were 102,576 vacancies in the NHS – almost 11,000 fewer than the previous year but still very high.23 The National Foundation for Education Research (NFER) annual Teacher Labour Market report found that the unfilled vacancy rate for teachers is six times higher than pre-pandemic, while 3.9% of teaching posts in further education were vacant at the end of the 23/24 academic year. 24 25

The impact of pay erosion has had severe cost of living consequences for many public sector workers. UNISON estimates that the average public sector worker saw the real value of their wage fall by over £11,000 in 2024 compared to 2009, with unions reporting that public sector workers feel that rises to their household costs - including mortgage repayments, energy bills, and childcare - significantly outpace pay increases.26 The effects on workers’ wellbeing should not be underestimated – for example, almost one in eight teachers have been forced to take a second job to supplement their income. 27

Improving relations with Europe offset by international headwinds

Importantly, relations with the European Union have started to be repaired. The government has placed a welcome priority on building a closer relationship with the EU, which is crucial to protecting good jobs, locking in the highest standards of workers’ rights and providing the UK with a powerful and reliable partner with which to face global instabilities and challenges.

The agreement of the Common Understanding in May was welcome, and while further rapid progress is needed, these commitments have potential to boost both growth and living standards. 28

In the first half of the year UK growth at 1.0 per cent was the fastest in the G7.29 But the wider economic context remains challenging. The USA’s economic policy has created turbulence and uncertainty around external demand and high UK interest rates continue to constrain internal demand. The Bank of England are also warning of threats to financial and economic stability, including from the “stretched” valuation of technology companies focused on AI.30

Stronger government current and capital expenditure are protecting the economy in the face of these risks but cannot fully migrate them. The latest monthly figures into July show quarterly GDP growth slowing to 0.2 per cent. The Bank of England judge the underlying rate of growth is around 0.25 per cent a quarter.

Consumer demand remains depressed by the living standards shock

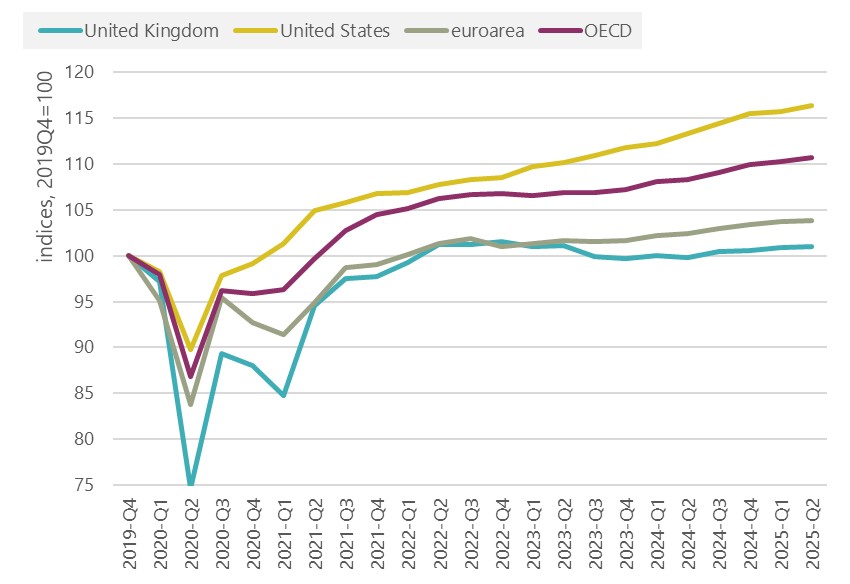

The most significant challenge the UK economy faces remains depressed consumer demand, with the latest figures showing it stagnating for three years. Since the financial crisis, consumer spending has generally accounted for around two thirds of GDP growth, but over the last two years has made no contribution at all. Improving workers’ living standards is vital for driving improvements in economic performance.

The situation in the UK is more challenging than in most advanced economies. Consumer spending in the UK is only up only 1 per cent on 2019 Q4, compared with 16 per cent in the US, 11 per cent across all advanced economies (OECD) and 4 per cent in the euroarea over the same period (chart 12).

Chart 12: Household expenditure, indices (2019Q4=100)

- 21https://www.resolutionfoundation.org/press-releases/britain-is-turning-…

- 22https://www.resolutionfoundation.org/press-releases/britain-is-turning-…

- 23NHS England, 2025: NHS Vacancy Statistics England, April 2015 - June 2025, Experimental Statistics https://digital.nhs.uk/data-and-information/publications/statistical/nh…

- 24Department for Education, 2025: Further Education Statistics https://explore-education-statistics.service.gov.uk/find-statistics/fur…

- 25Department for Education, 2025: Further Education Statistics https://explore-education-statistics.service.gov.uk/find-statistics/fur…

- 26’Bargaining on annual pay rises’, 2025: https://www.unison.org.uk/content/uploads/2024/11/Pay-claims-0125.pdf

- 27‘Supplementary Submission to the School Teachers’ Review Body‘, NASUWT, 17 January 2025

- 28https://www.gov.uk/government/publications/ukeu-summit-key-documentatio…‘, NASUWT, 17 January 2025

- 29GDP quarterly national accounts, UK - Office for National Statistics; table 5. https://www.ons.gov.uk/economy/grossdomesticproductgdp/bulletins/quarte…

- 30Record of the Financial Policy Committee meeting on 2 October 2025: https://www.bankofengland.co.uk/financial-policy-committee-record/2025/…

Flat spending indicates that workers remain under significant pressure. ONS polling shows that the cost of living (87%) remains the most important issue facing the UK (along with the NHS (82%) and the economy (70%)). 31 Survey data from the middle of the year show around one in four (24%) of adults reported that they had found it very or fairly difficult to get by financially in the past month; and two in five (40%) adults reported spending less on food shopping and essentials; this increased to 71% for those who were more likely to be financially vulnerable.32

Interest rates are unnecessarily high and are holding the economy back

While the Office for Budget Responsibility is reportedly revising its assessment of future potential productivity growth, our analysis suggests that the weakness of the UK economy follows from the weakness of aggregate demand. Attributing demand-driven weakness to the supply-side of the economy has been a constant and greatly problematic feature of policymaking since the start of austerity in 2010. 33

This is exacerbated by the Bank of England’s assessment of the position on inflation. Ongoing high interest rates are pressing down on growth, but making little impact on inflation. At 4 per cent interest rates in the UK are double those in the EU and on a less definitive trajectory to the USA (at the start of September the Federal Reserve reduced their 'target range' to 4-4¼% and signalled further reductions).34

While higher prices have meant that wages held up over the last year, as workers tired to stay afloat, spending is flatlining. Lower interest rates are urgently needed to boost demand.

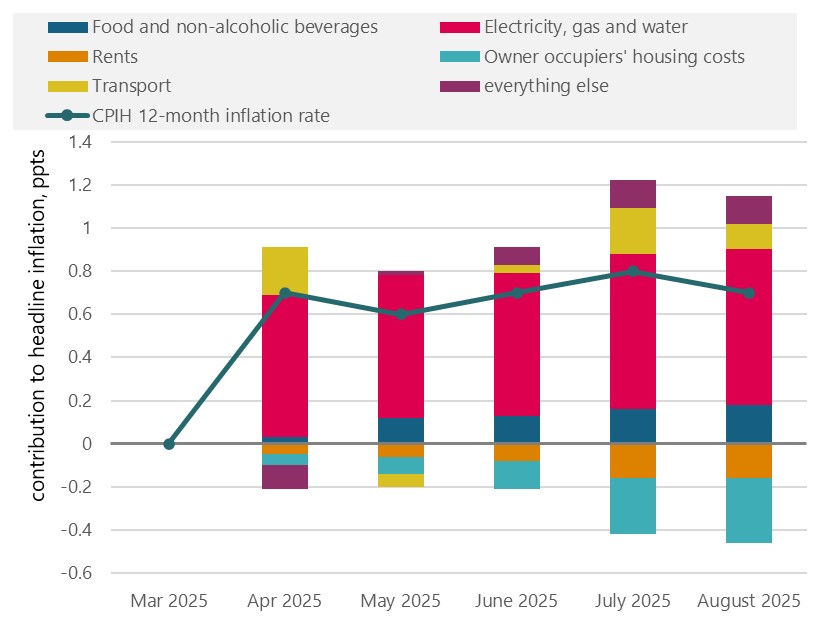

Those who maintain that higher rates are needed focus on higher inflation in the UK than our international competitors. But this assessment does not take account of the fact that most of the higher inflation rises in the UK are due to utility prices.35 Chart 13 shows that the contribution of electricity, gas and water at 0.72 ppts outstrips the rise in overall (CPIH) inflation between March and August 2025. The other key upward pressures are from food, which is driven by international commodity markets (notably coffee, chocolate and beef), a little on transport, though significantly reduced from July with the upward impact from air fares reversing, and only a small contribution from everything else. This latter category might include employer NICs, showing that while the costs are of course real for employers they are not significant factor driving higher inflation.

Chart 13: Contributions to change from March 2025 in CPIH inflation, ppts

- 31Public opinions and social trends, Great Britain - Office for National Statistics; 19 September 2025. https://www.ons.gov.uk/peoplepopulationandcommunity/wellbeing/bulletins…

- 32https://www.ons.gov.uk/peoplepopulationandcommunity/wellbeing/bulletins…

- 33’Productivity: no puzzle about it’, TUC, February 2025: https://www.tuc.org.uk/sites/default/files/productivitypuzzle.pdf

- 34’Federal Reserve issues FOMC statement’, 17 September 2025: https://www.federalreserve.gov/newsevents/pressreleases/monetary2025091…

- 35The relevant level of detail is only available for CPIH, where the overall increase in inflation between March and August is lower at 0.7 ppts, given a large downward effect from owner occupiers‘ housing (which is not included in CPI).

In a recent speech Sarah Breeden (Deputy Governor, Financial Stability at the Bank of England) deployed a similar chart, and concluded that “the current “hump” has been driven by external shocks that are not a reflection of domestic inflationary pressures”. 36 Given there is little evidence of domestic inflationary pressure, along with significant falls in consumer demand, the case for keeping interest rates high seems highly questionable. We judge these high rates are severely damaging economic growth, to no obvious gain in terms of the inflation picture.

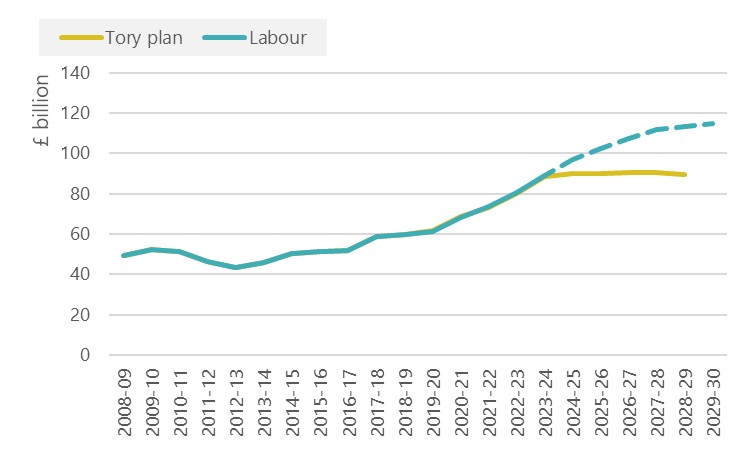

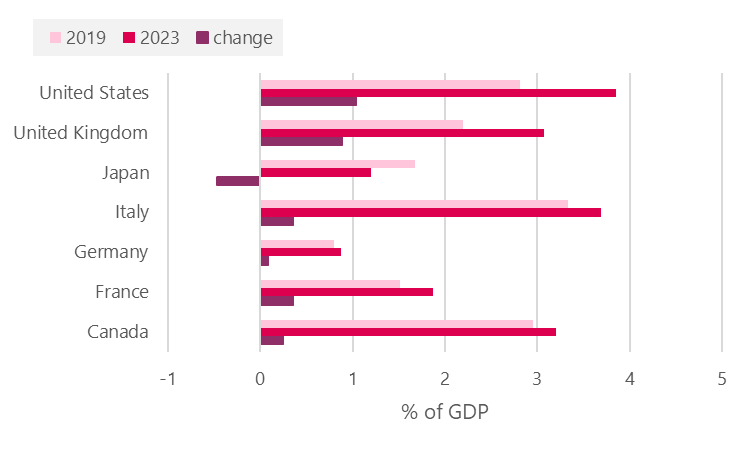

High interest rates are also impacting the public finances, as the higher Bank rate feeds through to the borrowing costs of government. The OBR shows payments up £75bn a year or trebling since before the pandemic. Over 2025-26 to 2029-30 government interest payments are expected to average £113bn a year; in the five years to 2019-20 interest payments averaged £38bn. 37

Chart 14 shows the UK along with the US having the steepest increase in the share of GDP allocated to interest payments (with figures only to 2023).

Chart 14: Government debt interest payments, % GDP

High interest rates have had significant implications for the debt burden inherited from the Tories. Overall debt interest payments depend on both the stock of government debt and the rate of interest on that debt. The relationship between the two quantities is complex. Government borrowing costs rocketed when the Bank of England raised interest rates, and projected future interest payments have further repercussions on the level of public debt going forward. But there is a vicious circle, to the extent that higher debt servicing costs mean that higher public debt is then regarded (not least by financial markets) as a bigger problem.

High interest rates also depress both private and public expenditure, and further damage economic growth. In the past the TUC has referred to a doom loop, when policy actions with the stated purpose of improving the public finances prove counterproductive. 36

- 36’From the doom loop to an economy for work not wealth’, TUC, 2023: https://www.tuc.org.uk/research-analysis/reports/doom-loop-economy-work…

- Last year’s Budget set a new course in motion, but more is now needed to sustain change and secure stronger growth and higher living standards.

- The country needs significant sustained investment. This must include ensuring decent public services can fully play their role in boosting productivity, growth and living standards.

- To deliver effectively, action is needed to boost growth (and reduce costs of government borrowing) and to raise revenues.

- Existing capital investment commitments should be at least protected and should be expanded – including by ensuring the National Wealth Fund has powers to borrow.

- Faster progress is needed on closer EU trade.

- Now is the time to address historic imbalances in how labour and capital are taxed, and to raise urgently needed revenues.

- This should include a significant increase in the bank surcharge, CGT reform and increased taxation on gambling companies.

- The government must also ensure that its approach to managing the public finances in the longer-term is conducive with securing strong, sustained growth – an independent commission should be established to consider how the management of our public finances should continue to evolve.

- It is vital that we oversee our public finances using credible fiscal rules, but also that these rules are grounded in the evidence of recent years and promote economic stability.

Last year’s Budget set a new course in motion, but more is needed to sustain change and secure stronger growth and higher living standards. This will need higher public spending, and therefore action to both raise new revenues and bring down the costs of government borrowing.

Capital investment must be sustained and increased

The increase in public investment to 2.7 per cent of GDP, and associated infrastructure initiatives, is vital to growth going forwards. It is imperative that this approach is maintained in the years ahead. Without government action, the default trajectory would have seen UK industry remaining starved of long-term investment and shrinking further. Without continued public investment to drive industrial upgrades and boosts to productivity, UK manufacturing risks becoming increasingly uncompetitive, with domestic production offshored to countries with move active states.

Likewise action in last year’s Budget to free up further borrowing by changing the target measure to public sector net financial liabilities (PSNFL) was welcome. Government borrowing is now based on a more complete picture of the government's financial position than the traditional Public Sector Net Debt (PSND) measure. By including the value of financial assets like student loans and other government investments alongside liabilities, PSNFL allows the government to fund investments that build assets, which can then be used to pay off the debt over time. This increases the scope to increase public investment without violating borrowing rules.

The Treasury should now take full advantage of these new freedoms and empower the National Wealth Fund to borrow directly from capital markets to increase its capital pool – an approach that would be in line with our current fiscal rules.

Stronger EU trade should be secured as soon as possible

With UK exports to the US now facing additional tariffs, it is more important than ever that the UK can improve trade and investment with the EU, our closest and most integrated trading partner.

The TUC welcomes the priority the government has placed on building a closer UK-EU relationship and the achievement of the Common Understanding in May between the UK and EU. It is critical that the government secures as soon as possible the commitments outlined in the UK-EU Common Understanding to remove barriers to trade in agrifood products, EU carbon border tariffs for steel exports, enable young workers more opportunities to work and study in the EU and allow UK defence companies to bid for contracts from the EU SAFE fund - which will promote jobs across the country.

The TUC and our sister trade unions in countries across the EU have common objectives a closer UK-EU relationship as affirmed in the joint statement the TUC released with the European Trade Union Confederation in March.39 We would like to see the government build on the Common Understanding to:

- remove barriers to trade in chemicals and pharmaceuticals which have faced significant additional costs since Brexit which have put jobs and conditions at risk.

- see barriers for touring artists removed.

- strengthen Level Playing Field commitments in the UK-EU Trade and Cooperation Agreement by agreeing to implement improvements to workers’ rights made in the EU, so UK workers do not fall behind.

We look forward to continuing to engage with the government on the UK-EU reset negotiations, including through our role chairing the UK-EU Domestic Advisory Group.

Fairer, better taxes

Given the imperative to support and increase public investment, the TUC supports a wealth tax package with higher taxes on wealth, banks and gambling companies. Decent public services play a vital role in boosting productivity, growth and living standards – whether through improving the nation’s health, boosting educational performance or ensuring that people with caring responsibilities are able to work. In polling undertaken before the election, 81% of business leaders said that public services were important to the success of their business, and 89% said that public service improvements should be a government priority.40 The Resolution Foundation has set out the huge ‘in-kind’ benefit that public services make to the living standards of low and middle income households. 41

As well as raising vital revenues, fair taxes can also address wider policy challenges. The director of the Institute for Fiscal Studies has recently warned that the UK tax system is characterised by “a large, unjustified and problematic bias against employment and labour incomes and in favour of business ownership and capital”.42 This can create wider distortions – with the incomes of low and middle earners taxed at rates that are much higher than those who make many times more from their investments. As workers spend a larger share of their incomes than the wealthy, the current design of our tax system is holding back wider spending (particularly important given the role of consumer spending in boosting growth).

While some have suggested that it is not falling real incomes but high savings rates holding back consumers, there is widespread evidence that savings may be concentrated among better off households.43 44 The Budget provides an important opportunity to start to correct this imbalance, while also raising some of the revenues needed to boost growth and rebuild our public services.

Our polling has also shown that there is significant support for a package of wealth taxes and taxes on financial institutions to fund better public services, and that this support comes from across the political spectrum.V More than two-thirds of adults support a package of measures to tax wealth, banks and gambling companies, while just 23 per cent oppose. This rises to 84 per cent supporting among Conservative to Labour switchers from the 2024 general election. And three-quarters (74 per cent) of 2024 Labour voters who are now learning towards Reform support the measures.

The public understand the need to act. Our polling also found widespread support for a modernised and simplified system, with three-quarters (73 per cent) supporting this. This rises to 83 per cent among Labour to Reform switchers.

Immediately, a package could include:

- A windfall tax on banks. In recent years, banks have made significant unexpected profits because of increased interest rates. This has led to higher returns both from net interest (the difference on interest charged to borrowers and paid to savers) and interest paid to banks on reserves they hold at the Bank of England. As a result, bank profits are now even higher than they were in the period before the financial crisis. But under the Conservatives, taxes on banks were slashed just as these excessive profits kicked in. An increase in the bank surcharge to 16 per cent, double what it was before the Conservative cuts, could raise £20bn over the next four years. A 35% surcharge, which would be the same level as the windfall tax the Conservatives imposed on energy companies,46 could deliver £50bn over the same time period.47

- Reforming the Capital Gains Tax (CGT) system by equalising CGT rates with income tax rates and closing loopholes. This would build upon the changes to CGT already announced in the October 2024 budget and could raise a further £12 billion a year. 48

- Increased taxes on gambling companies. Proposals for how to increase taxes on gambling have previously been put forward by the IPPR who have estimated that a package of taxes aimed at tobacco, gambling, vaping, alcohol and unhealthy foods could raise £10 billion by 2029/30. The changes to gambling taxes specifically could raise up to £3.4bn in 2029/30. 49

- A 2 per cent tax on assets over £10 million. This would affect only 0.04 per cent of the population and could raise up to £24 billion a year. This would have to be carefully designed and implemented, with learning from other countries that have put wealth taxes into place. Budget 2025 provides an opportunity to consider the first steps that could be taken towards ensuring such an approach can be established.

In the medium term, wider reform is also needed. For example, there is a strong case for a review of property taxation where existing approaches are both unfair and damaging to growth.

A new fiscal commission

The government must also ensure that its approach to managing the public finances is conducive to securing strong, sustained growth.

Under the Conservatives the rules were changed nine times,50 and the public finances still deteriorated to an unprecedented extent (as set out above). While the Chancellor’s recent statement on the country’s public spending inheritance rightly pointed to the disarray and negligence caused by previous governments, the lesson from past failure must also be that an overly restrictive household budgeting approach to the public finances risks being counterproductive. It is pro-growth policies that will permit our national revenues to improve, and in turn these must be enabled by our fiscal framework. 51

Fiscal rules and fiscal councils are now part of governments’ public finance processes across developed economies. In a recent overview, the IMF describe fiscal rules as “a long-lasting constraint on fiscal policy through numerical limits on budgetary aggregates. Fiscal rules typically aim at correcting distorted incentives and containing pressures to overspend, particularly in good times, so as to ensure fiscal responsibility and debt sustainability.” They describe fiscal councils as: “often non-partisan, technical bodies entrusted as a public finance watchdog to strengthen credibility of fiscal policies with a variety of mandates.” 52

The IMF also note that these frameworks have become particularly widespread over the last two decades. In the UK, fiscal rules started with the introduction of Gordon Brown’s ‘golden rule’ that over the economic cycle the government would only borrow to invest and not to fund current spending. Fiscal rules have been part of the UK public finance policy ever since.

The UK fiscal council, the Office for Budget Responsibility (OBR) was then set up under Conservative Chancellor George Osborne in 2010 with the stated purpose of increasing “the role of independent expert oversight over the UK fiscal process” and as one of “the post-financial crisis creation of increasing numbers of Independent Fiscal Institutions (IFIs) across advanced democracies”. 53

Since then, in the UK and many other economies, fiscal frameworks have continued to further evolve. The IMF notes that post financial crisis many frameworks were reviewed to enhance “flexibility, enforcement and the monitoring of fiscal rules”.54 They also draw an important distinction between the pre-and post-pandemic periods, and note that in many cases government needed to deviate from their fiscal rule limits to deliver support. They reference the post-pandemic policy challenge of “whether and how countries should return to the limits and the fiscal rules, while ensuring credibility of the fiscal framework.” There have been suggestions that many countries are now starting to think about the ‘second generation’ of fiscal frameworks.

The TUC view is that there is a compelling case for further evolution of the UK public finance processes. This should recognise, as the IMF say, the importance of strong fiscal frameworks but also of ensuring that they are fit for purpose and responsive to changes in the economic cycle - rather than reinforcing them (i.e. rules should ensure they are not driving austerity during periods of slow growth when spending is needed to boost demand).55 The National Institute of Economic and Social Research (NIESR) has warned of “self-imposed and arbitrary fiscal rules” and urged a “rethink of the fiscal framework“. 56

Both NIESR and Andrew Haldane, former Bank of England chief economist, have set out that our current approach is holding back growth:

- 39https://www.etuc.org/sites/default/files/press-release/file/2025-03/EN-…

- 40https://www.tuc.org.uk/news/more-half-business-leaders-59-say-they-are-….

- 41https://www.resolutionfoundation.org/events/public-services/

- 42'Clear visions for tax reform exist — Reeves just needs to back one‘, Helen Miller, 3 October 2025: https://www.ft.com/content/d425fc50-760c-4526-999d-5c9868a2fe81

- 43Distributional factors are likely at play here – not least given the severity of the real pay and incomes crisis set out above. NIESR work from three years ago suggested the first six income deciles were in deficit, with spending outstripping incomes (UK-Economic-Outlook-Spring-2022.pdf: table 2.6).

- 44’The Polarization of Personal Saving’, Bureau of Labor Statistics, June 2024: The Polarization of Personal Saving. Of note also is a fuller analysis for the US, which echoes these results and showed that the top decile accounted for virtually all of household saving. The restraint on consumption is less the high saving, and more the bad distribution of income. https://www.bls.gov/osmr/research-papers/2024/pdf/ec240050.pdf

- 46‘Taxation of North Sea oil and gas’, 2024: https://commonslibrary.parliament.uk/research-briefings/sn00341/

- 47’Bank taxation‘, TUC, 2025: https://www.tuc.org.uk/research-analysis/reports/bank-taxation-2025

- 48’Ten tax reforms and closed loopholes to raise over £60 billion in a single year’, Tax Justice UK, 2025: https://taxjustice.uk/wp-content/uploads/2025/03/Ten-tax-reforms-closed…. Estimate of money raised by a 2% tax on assets over £10 million also taken from this source.

- 49’Our greatest asset’, IPPR, 2024: https://ippr-org.files.svdcdn.com/production/Downloads/Our_greatest_ass…; ; estimate of money raised from taxes on harmful products can be found on page 29.

- 50https://www.theguardian.com/uk-news/2024/mar/05/uks-fiscal-rules-obr-tr…

- 51As Keynes put it, “There is no possibility of balancing the budget except by increasing the national income” (Collected Writings, Volume IX, p. 347).

- 52‘Fiscal Rules and Fiscal Councils: Recent Trends and Performance during the COVID-19 Pandemic’,

- 53The Office for Budget Responsibility and the Politics of Technocratic Government, Ben Clift, 2023: pp. 75-6.

- 54See n. 52

- 55TUC response to spending review consultation 2025.pdf (section 2). https://www.tuc.org.uk/sites/default/files/2025-03/TUC response to spending review consultation 2025.pdf

- 56Chancellor on track to miss fiscal rules, says economic forecaster | The Independent https://www.independent.co.uk/news/business/chancellor-on-track-to-miss…

Not only are these rules are not being met, but they are also inadvertently constraining the public investment needed to improve economic growth

... Existing fiscal rules risk starving the economy of the very investment needed to boost medium-term growth and, ultimately, pay down debt and lower taxes.

Commenting on New Economics Foundation proposals to replace the OBR with a new institution to work alongside the Treasury,59 Mehreen Khan, Economics Editor of The Times, is more direct: “In 2025, that noble aim has created a created a perverse system where three technocrats have an outsized say over what the government of the day can spend or tax”. 60

We need to ensure that our approach to the oversight of fiscal policy reflects the learning of the last 15 years and is fully aligned with the government’s growth ambitions.

In this context, the TUC believes the government must act. Recognising the need to ensure any reform is informed by evidence, we propose the government set up a formal review to consider how the UK’s fiscal framework needs to further evolve to ensure it provides both fiscal and social stability in post-pandemic Britain.

We propose the review could include consideration of:

- How the UK approach compares to best practice globally, both as countries respond to the experience of policy since 2010 and to the changing geopolitical context. Germany is only the most prominent country to refigure its approach to fiscal policy, with a ‘constitutional reform of its national fiscal framework’.61

- The advantages (and challenges) of expenditure targeting over the present fiscal mandate based on debt and deficit targets. Iain Begg of LSE has reported that “Many European countries with far healthier public finances have moved away from debt and balance rules in favour of what is known as an expenditure rule. The main reason is that the government directly controls expenditure and, especially if it plans it over a number of years, can set a stable path for the economy”. 62

- Institutional arrangements including the operation of fiscal councils globally, the roles of the Treasury and OBR, and the timing of fiscal events, and how to make more meaningful assessments of investment outcomes over a longer time horizon. This could include consideration of the OBR’s role in producing the economic forecast, and whether there are institutional arrangements in other countries which could inform a new approach to building on external expertise in forecasting the impacts of specific policy interventions (for example labour market policy).

- The role of modelling processes, and in particular the role of the controversial judgement that public expenditure ‘crowds out’ private expenditure, and, in the event of error, the implications for capacity and the output gap. This should keep uppermost the IMF conclusion: “On average, fiscal consolidations do not reduce [public] debt-to-GDP ratios”,63 which has certainly been the case in the UK. While all commentators including the OBR themselves recognise the role of uncertainty, existing mechanisms also have potential for bias. Ben Clift has set out that any such economic models are not politically neutral, “there is always a politics of economic ideas, and economic orthodoxy is always a social construction”.64 65

- The interplay between the OBR’s modelling processes and assumptions about policy at the Bank of England. Both institutions currently seem to take a closely aligned position on the output gap (the measure of spare capacity in the economy) and crowding out (the extent to which public spending displaces private investment). For instance, the OBR anticipated interest rates would have to stay higher for longer after the expansionary Autumn Budget 2024 as their modelling suggests limited spare capacity. In this assumed context they considered higher public investment would crowd out private investment. Separately Robert Chote (former Chairman of the OBR) wrote in 2024 about events in 2012/2013 when the OBR “show[ed] an extended period of spare capacity in the economy”, “… from which readers might have concluded that we felt the Bank needed more help from fiscal policy to bolster demand. That signal would have been clearer had we also forecast that inflation would persistently undershoot the target, but this would have had the Bank and Treasury straight on the phone”.66 The implication of his point is that the OBR was constrained in its ability to make the case for more demand stimulus in the economy, as it would have found itself in conflict with the Bank of England.

It is vital that we continue to manage our public finances using credible fiscal rules, but also that these rules are grounded in the evidence of recent years and promote secure growth and economic stability.

- 59'A democratic fiscal framework’: https://neweconomics.org/2025/08/a-democratic-fiscal-framework

- 60’OBR should be scrapped, Rachel Reeves told‘, 21 August 2025: https://www.thetimes.com/business-money/economics/article/new-economic-…

- 61https://economy-finance.ec.europa.eu/economic-forecast-and-surveys/econ…

- 62How Rachel Reeves should have changed the fiscal rules - British Politics and Policy at LSE https://blogs.lse.ac.uk/politicsandpolicy/how-rachel-reeves-should-have…

- 63World Economic Outlook, April 2023: https://www.imf.org/en/Publications/WEO/Issues/2023/04/11/world-economi…

- 64The OBR and the politics of technocratic economic governance, p. 20.

- 65While the OBR was recently (Feb.) reviewed, this was led by the former head of the Dutch independent fiscal institution (IFI). The review did warn that emphasis on “headroom” was increasingly problematic, and “[t]his focus on the short-term fiscal space has gone and-in-hand with very limited attention on long-term fiscal sustainability” The review was headed by Laura van Geest, former head of the Netherlands Bureau of Economic Policy Analysis (CPB). https://obr.uk/third-external-review-of-the-obr-published/

- 66‘Has the OBR experiment been worthwhile?’, August 2024: https://heywoodquarterly.com/has-the-obr-experiment-worked/

Below we set out both the key wider policies the country needs both to secure stronger growth and higher living standards.

Direct support to raise workers’ living standards

- Introduce a new domestic energy billing structure that provides a low and fixed rate for sufficient energy to cover essential needs (variable according to family size, property architype, receipt of benefits, and energy requirements for those with disabilities) along with several higher rates for high and luxury usage.

- Adjust VAT on domestic energy. Current flat 5% VAT rates could be replaced by a 0% assessment for essential usage levels along similar lines to the above, with higher usage being taxed at 10%, and luxury usage (for example for private swimming pools) taxed at 20% or more.

- Reverse the Conservative policy of the two-child benefit cap and repeal the wider benefit cap to ensure all children feel the full benefit of the change.

- Remove the five-week wait for Universal Credit payments and redesign the system to ensure more regular payments and longer assessment periods to reduce fluctuations in income.

- Recommend a minimum wage rise that takes the rate beyond two-thirds of median wages and ask the Low Pay Commission to chart a course towards a 75% bite target.

A consistent focus on more and better jobs

- Introduce a shared cross-government set of metrics for labour market policy including commitments to: secure progress towards an 80 per cent employment rate; return the number of young people NEET to pre-covid levels by the end of the parliament; and drive improvements in job quality, committing to a reduction in the number of people in insecure contracts and faster wage growth in deciles below the median.

- Establish a central labour market unit to oversee the development and implementation of these ambitions. This would help ensure job quality and quantity measures are consistently reinforced across policy and that those groups currently furthest from the jobs market are not left behind in policy design.

- Prioritise more resources for the employment tribunal system to ensure that cases can be resolved swiftly. This should sit alongside a tripartite review of the system, to ensure it is fair, accessible and fit for the future – involving unions, employers and Acas.

- Ensure the establishment of the Fair Work Agency is supported by a funding settlement that enables it to discharge its new functions and powers effectively. This should be supported by ensuring that new powers to recoup the costs of investigations/enforcement actions from employers who are found to have broken the law are switched on as soon as possible.

- Deliver a fair funding approach for the Central Arbitration Committee. We estimate that the CAC will require a budget increase of around 50 per cent to carry out its significant new duties to a sufficient standard.

Invest in the Health and Safety Executive and the Equality and Human Rights Commission, committing to bring their budgets back to their pre-financial crisis position in real terms. - Ensure the effective implementation of the Employment Rights Bill with the introduction of additional support to equip managers and union reps with the knowledge they need to put new rights and protections into practice.

- Implement an ambitious jobs guarantee for young people, with early access for those young people at highest risk of becoming NEET. Jobs should be by government to pay at least the minimum wage alongside training that provides a pathway to a level 3 qualification.

- Put in place effective support for more disabled people to stay in work and return to employment if they are out of work, including through introducing a time limit on decisions regarding reasonable adjustments and ensuring excellent employment support is available, ideally extending a jobs guarantee approach.

- Increase apprenticeship participation and completion rates through expansion of the Growth and Skills Levy to include more SMEs, and greater engagement with trade unions to improve apprenticeship standards and apprentices’ experiences.

- Ringfence additional funding for the tertiary education sector to address the workforce recruitment and retention crises in further and higher education, recognising that these will be key barriers to skills and labour market policy delivery if unaddressed.

- Pilot a new £5-10 million union learning agreement fund, with an overarching aim to raise collective bargaining coverage with regard to skills.

- Take a consistent approach to developing and implementing workforce strategies across the industrial strategy sectors.

- Ensure delivery of large infrastructure projects, involves employers with the TUC and affiliated trade unions to secure framework agreements, promoting secure jobs and high labour standards.

- Design social value criteria to capture the potential of procurement to stimulate re-industrialisation and good quality, unionised jobs across the country.

Full support to futureproof industry

- Provide strategic transitional investment to drive innovation in foundation industries, via a new fund.

Retain existing commitments including:

- £1.8bn National Wealth Fund investment in ports

- £500m National Wealth Fund investment in hydrogen

- £2.5bn investment in steel

- £1.5bn NWF investment into gigafactories

- £2.5bn DRIVE35 investment in automotive, including support to transition the Internal Combustion Engine supply chain and develop EV supply chains

- £21.7bn investment over next 25 years in Carbon Capture, Utilisation and Storage (CCUS)

- Wider support via the National Wealth Fund and British Business Bank for electrification, grid infrastructure and other decarbonisation technologies.

- Government should launch a ‘Business Transition Hub’ to provide pro-active guidance, technology insights and market intelligence to high-carbon sectors on futureproofing pathways, decarbonisation and diversification

- Expand the Clean Industry Bonus by up to £1 billion over the course of the Parliament.

- Aim to invest £1.1 billion a year into building up UK clean energy supply chains, through a combination of Clean Industry Bonus, National Wealth Fund and expansion of past grant schemes (e.g. Offshore Wind Manufacturing Investment Scheme and the Green Industries Growth Accelerator).

- Establish a targeted public investment fund within the National Wealth Fund to support oil & gas supply chain firms to upgrade their infrastructure, technology or skills base, sufficiently to supply new markets.

- Provide new funding to support the North Sea transition including by:

- Establishing a “Your Country Needs You” redeployment programme to transfer oil and gas workers to sectors with skills shortages.

- Putting in place a time-limited furlough or a short time working scheme, for workers who fall through the gaps from other interventions.

- Set a clear goal to achieve industrial electricity price parity with EU competitors, with a plan towards getting there.

- Take further action to bring down industrial electricity prices including bringing forward the British Industrial Competitiveness Scheme or failing that introduce an interim support scheme to be available to industry on the brink of closure due to energy costs.

- Introduce an electrification business model to incentivise fuel switching within appropriate industrial processes.

Sustained investment in world class public services

- Ensure investment in public services is now sustained. Services remain overstretched, understaffed and unable to meet the needs of our communities.

- Engage in dialogue with public services unions on a plan to restore public sector pay, recognising that more than a decade of pay restraint has exacerbated the recruitment and retention crises across much of the public sector and the financial hardship faced by many public services workers.

- Ensure evidence to Pay Review Bodies (PRBs) does not dictate a headline percentage pay award. This negates the independence of PRBs and their process, and becomes a de facto cap.

- Fund future pay awards with additional expenditure so that public services and devolved governments are not forced to reallocate budgets and make cuts elsewhere to meet the value of pay awards.

- Reinstate a structure like the Public Services Forum as a ministerial advisory body to guide the overarching approach to delivering government’s priorities in public services, including AI adoption and public services reform.

- Ensure the welcome Fair Pay Negotiating Body for Adult Social Care and School Support Staff Negotiating Body have the resources they need to address deep-seated recruitment and retention problems.

- Make greater investment in public-interest regulation and scientific resilience so that all relevant bodies are fully-resourced.

- Restore fair and sustainable funding for local government – including restructuring or cancelling local government debt – both to retain and develop the local government workforce and protect and rebuild local public services.

- Set out a roadmap for sustained investment in fire and rescue services.

- Ensure public ownership and in-house delivery are the default setting for public services, with funding available to ensure this can happen. The public interest test should be introduced swiftly.

- Strengthen the Procurement Act so that organisations that commit labour-related and other regulatory violations are subject to more robust exclusions criteria.

- Ensure transparency around public spending and contracts, including suppliers’ contract performance, by establishing a centrally-held and managed Domesday Book of public service contracts and extending the Freedom of Information Act to be applicable to any entity delivering a public contract.

Provide direct support to raise workers’ living standards

Support for domestic energy prices

We welcome the government’s ambition to lower domestic energy bills by growth of clean energy production and the electrification of an increasing percentage of domestic heating. But it remains the case that domestic energy bills are persistently high, and that the scale of current government commitments is not clearly aligned to a significant reduction that people can feel in their regular bills. We therefore recommend that the government should look to more immediate and demonstrable solutions to this situation.

Government should consider a new domestic energy billing structure that provides a low and fixed rate for sufficient energy to cover essential needs (variable according to family size, property architype, receipt of benefits, and energy requirements for those with disabilities) and introduce several higher rates for high and luxury usage along a rising-block tariff structure, with the highest rates reserved for such clear luxuries as heating private pools, heating unoccupied buildings and warming driveways.67 This could be introduced on a cost neutral basis, with premium tariff payers subsidising lower income users, but could be expanded by a government subsidy. Our initial assessment is that a subsidy of around £2bn could save the average household in the lowest income decile over £200 a year.

This new structure (versions of which are already used across such different jurisdictions as Japan and California) would ensure that no households goes without the energy they need to cover their basic needs, with eradication of absolute fuel poverty becoming possible. It would result in reduced bills for the majority and introduce the logic of progressive liability to a key element of household expenses. Furthermore, such a new system would disincentivise very high consumption, reducing overall energy usage and incentivising households to take up offers of and seek out energy efficiency retrofit, promoting the aims of the Warm Homes Plan.

The government could also consider adjusting VAT on domestic energy with similar results. Current flat 5% VAT rates could be replaced by a 0% assessment for essential usage levels along similar lines to the above, with higher usage being taxed at 10%, and luxury usage taxed at 20% or more. This too would lower costs for the majority while increasing tax income overall, allowing new money to be redirected to expand delivery of the Warm Homes Plan.

Remove the two-child benefit cap

The government has made a welcome commitment to develop a child poverty strategy. This will need to address several policy areas – including social security.

A priority step must be to reverse the Conservative policy of the two-child benefit cap. Alongside this the benefit cap has to be repealed, as any financial gain for families could be erased should this wider cap remain in place.

Abolishing the two-child limit would be the most cost-effective way to reduce child poverty. Scrapping the two-child limit now would not only pull 350,000 children out of poverty overnight but it would stop another 150,000 being pushed into poverty over this parliament.68 Estimates for the cost of removing both policies are in the range of £3-4 billion a year by 2029/30.

Reform Universal Credit

The design of Universal Credit can also exacerbate child poverty. We support the government’s recognition that Universal Credit needs to be reformed, and hope that the Universal Credit Review will achieve progress on removing the five-week wait, enabling more regular payments and putting in place longer assessment periods to reduce fluctuations in income.

A five-week wait for the first payment fails to recognise that most low-paid workers do not have savings to get them through this period.

Along with redesigning the initial payment in Universal Credit, the whole monthly assessment period should be reformed. The monthly assessment periods are set based on the date of someone’s claim, rather than being aligned with pay cycles, thus causing a mismatch between the two. This means it is possible to receive two wage payments in the one assessment period which reduces the Universal Credit payment. USDAW report that 78% of their members on Universal Credit are paid four weekly, which means their Universal Credit payment can be reduced by £800 for one month a year, making it harder to budget.

In our 2022 report on reforming Universal Credit69 we recommended the removal of the monthly assessment period designed to include a monthly payment in arrears. We also set out the need for a longer three- to-six-month assessment period to reduce fluctuations and provide stability, and allowing claimants to choose more frequent payment options to better suit their budgeting needs.

A new bite target for the National Minimum Wage

The government made a manifesto commitment to make the minimum wage a genuine living wage. This will require ambitious increases which take the minimum wage above its current 66 per cent bite. This is in line with the government’s remit to the LPC which says the minimum wage should not fall below two-thirds of median wages. As the minimum wage has been at two-thirds of median wages for two years, the next increase should go beyond this.

Looking forward, the minimum wage should be increased to 75 per cent of median wages so that it reaches £15 as soon as possible. This would raise pay for millions of workers, improve living standards, and shift our economy away from an over-reliance on low paid work. A strong minimum wage underpins much of the government’s vision including making work pay, tackling poverty and delivering economic growth.

The Low Pay Commission should be responsible for charting an ambitious path towards a 75 per cent bite target. This would ensure that the process is led through social partnership by a body with authority to test the limits of minimum wage policy alongside consideration of prevailing economic conditions.

A consistent focus on more and better jobs

Achieving the government’s growth mission of “more people in good jobs, higher living standards, and productivity growth in every part of the United Kingdom” requires a sustained focus on improving both the availability and quality of jobs. Crucially, government must recognise that job quality and job creation are not in tension, but mutually supportive goals.

A range of welcome interventions have been announced, not least the Employment Rights Bill and the wider plan to Make Work Pay. The Get Britain Working White Paper also proposes an important 80% employment rate target, which sits alongside recognition of the need to support more young people into meaningful routes towards the jobs market and ensure more disabled people can stay in work. The industrial strategy’s workforce and skills plans, and forthcoming skills and apprenticeship reforms, will also have important roles to play in securing success.

Ensuring consistency across labour market interventions would benefit from a shared cross-government set of metrics. These should include commitments to:

- Secure progress towards an 80 per cent employment rate.

- Return to the number of young people NEET to pre-covid levels – a 15% reduction by the end of the parliament.

- Reduce flows from employment into economic inactivity because of ill health.

- Shorten the average period of unemployment/gaps in average unemployment duration between local areas (a test of the success of both job creation and back to work policies)

- Improve job quality, for example, committing to a reduction in the number of people in insecure contracts, or to securing faster wage growth in deciles below the median.