Record household debt levels show why workers need a new deal

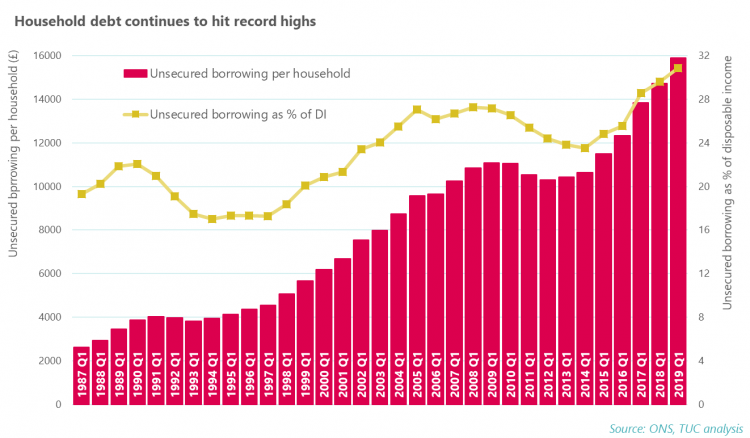

We’ve published new research today showing the level of household debt is continuing to hit new record highs. In the first quarter of 2019, unsecured debt per household rose to £15,880. This is up by £1,160 on a year earlier, and is a record high for the first quarter of the year. This isn’t a blip, but part of an on-going trend: household debt has been rising each year since 2012, hitting a record high in 2015 and surpassing this record each year since.

Unsecured debt as a percentage of disposable income is at 31 per cent, also a record high for the quarter.

Unsecured debt is debt that isn’t backed by an asset, such as a house. So, unsecured debt excludes mortgages, but includes stuff like bank loans, personal loans, credit cards, and student loans .

The impact of household debt

New TUC analysis of the 2018 Bank of England/NMG household survey data provides us with details on who has household debt, and how it affects them.

Over half of households (53%) report having unsecured debt, most commonly in the form of credit card debt (60%), overdraft (28%), personal loans (25%) and car finance (25%).

While some household debt in itself isn’t necessarily a bad thing, it becomes problematic when repayments become a burden, and when people begin struggling to keep up with repayments.

It’s therefore concerning that the majority of households with unsecured debt (61%) describe repayments as a burden, with one-fifth saying they’re a ‘heavy’ burden. Given the percentage of those with unsecured debt, this means that the finances of one in every ten households are heavily burdened by debt repayments.

Over half of those with unsecured debt (54%) are either very or somewhat concerned about their current level of debt (both secured and unsecured). When asked the reason for being concerned, respondents could choose more than one option. The most common reason given for concern was the threat of higher interest rates (42%). Other common reasons for concern are directly work-related, such as a person’s income being lower than expected when they took out the loan (29%), or there being a chance of a fall in income (21%).

Given all of the above, it’s unsurprising that 14 per cent of those with unsecured debt have, in the past year, been more than two months behind on payments. The most common reason given for falling behind on debt payments is an increase in other bills or unexpected expenses/costs (34%). Again, other common reasons are all directly work related, such as an earner in the household losing income due to sickness or injury (21%), or someone in the house missing out on overtime or their hours being reduced (21%).

As well as struggling with repayments, households with unsecured debt are also less likely to have cash set aside for an emergency. Whereas 23% of those without unsecured debt don’t feel they have enough money set aside for emergencies, this almost doubles to 45% among those with unsecured debt.

Who’s more likely to have household debt?

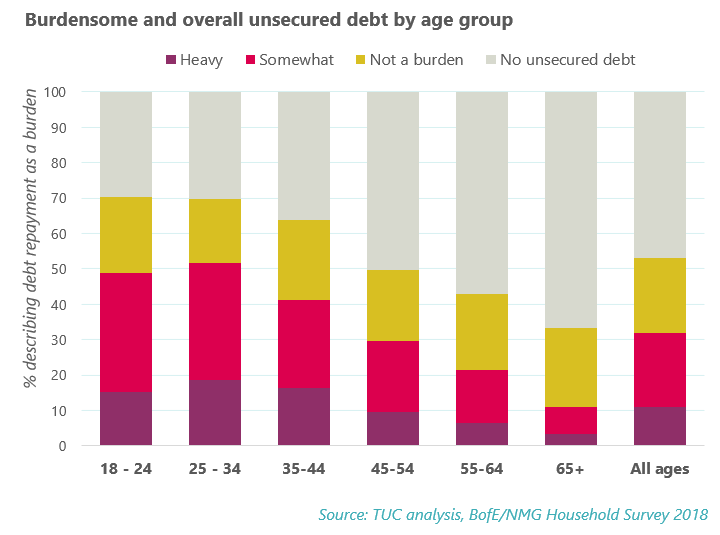

Young people are disproportionately likely to be in debt, and are more likely to feel burdened by the repayments of this debt.

70% of those aged 18-34 report having a type of unsecured debt. This drops to 33% among people over 65. This is at least partly due to higher levels of student loan debt among younger age groups, but this doesn’t make unsecured debt among younger people any less of a burden. Younger age groups are not just more likely to hold unsecured debt, but also more likely to describe their debt as a burden. 74% of those aged 25-34 with unsecured debt described repayments as a burden, with the figure being even higher among those aged 25-34 (74%).

There’s also a link between household unsecured debt and type of housing. Those renting privately and those with a mortgage are more likely to have some form of insecure debt (65% and 62% respectively, compared to 53% of all). This isn’t the only link between unsecured debt and housing a quarter of those with unsecured debt have had difficulties paying for their accommodation in the past 12 months. This compares to 7% of those without unsecured debt.

What can be done?

We believe that low pay, insecure work and austerity are all feeding into this growing debt crisis. We therefore need to reset the balance of power in our workplaces and our economy. We can do this by ensuring that workers get the chance to negotiate better pay and conditions through trade unions. To do this, unions need access to workplace.

We’d also like to see a £10 National Minimum Wage introduced as quickly as possible. A pay rise would better prepare households to meet sudden rises in bills and help to cover any debt repayments. And we need an end to the type of insecure work that means both working patterns and pay are often unpredictable, with households not knowing how much money they’ll have from one week to the next. This should involve a ban on zero hours contracts, as well as compensation for those whose shifts are cancelled at the last minute.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox