Autumn Budget: a plan to start rebuilding Britain

But with yesterday’s far-reaching Autumn Budget, Rachel Reeves acted decisively to deliver an economy that works for working people.

The government’s plans for investment and departmental spending are a vital first step towards repairing and rebuilding Britain – securing the stronger growth, higher wages and decent public services that the country desperately needs

Tax rises will ensure much-needed funds for our NHS, schools and the rest of our crumbling public services, with those who have the broadest shoulders paying a fairer share. Rightly, the Chancellor has prioritised hospitals and classrooms over private jets.

There is still a lot more work to do to clean up 14 years of Tory mess and economic decline – including better supporting and strengthening our social security system. But this budget sets us on an urgently needed path towards national renewal.

Here we examine the Budget’s implications for the economy, spending, taxes and the public sector finances.

1. Economy and pay

The economy has proven stronger than expected in 2024, and higher government spending will mean growth rising from 1.1 per cent in 2024 to 2.0 per cent in 2025.

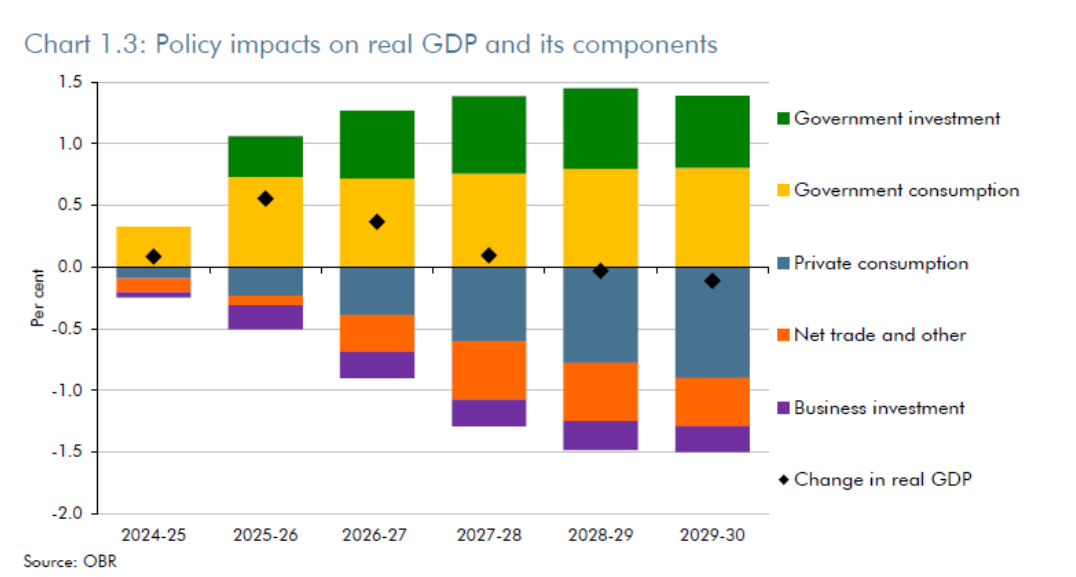

The chart below shows how the OBR see the impact of government spending policies. Initially they forecast stronger growth, but then assume will gains reduce as other sources of demand are weakened.

This is standard for the OBR and should come with something of a health warning. The OBR tend to presume government spending ‘crowds out’ private spending – and on this basis they wrongly predicted that austerity would have no impact on the economy.

Time will tell if the OBR forecasts are proven right or wrong. But TUC believes the OBR are likely to have underestimated the gains that the Budget will deliver.

Over the longer term the OBR does recognise that higher government investment will strengthen the economy and crowd in private investment – judging an increase in ‘potential’ of 0.4 per cent after ten years and 1.4 per cent after fifty if higher investment is sustained. The IPPR have in the past stressed this crowding in, and are now pushing back against the conservatism of this assessment.

Reflecting the initially stronger growth, unemployment is expected to fall from 1.5 million this year to 1.4 million next year.

Inflation is expected to be a little above target until the end of the forecast.

Real wages are expected to grow in 2024 (+2.1 per cent) and 2025 (+1.0 per cent), and overall by 3 per cent over the forecast period.

Beyond these statistics the headline story for workers includes a welcome rise of 6.7 per cent in the minimum wage, as the LPC take account of the cost of living in their calculations. And there is the broader background of the Employment Rights Bill, which will further boost living standards.

Workers will also see improved social security. Deductions taken from Universal Credit will be reduced from 25% to 15%, reducing hardship for some of the poorest families by increasing their monthly income – for some by more than £400 And the extensions to the Household Support Fund will provide an additional £1 billion in funding to protect vulnerable people.

The changed tone on employment support is also welcome, though the position on work capability reforms is unclear. There were several positive announcements on pensions, not least dealing with injustices on pensions for ex-miners. Bringing pensions into the Inheritance Tax regime is a sensible step to raise revenues. And the confirmation of the triple lock will provide a welcome boost for pensioner incomes.

2. Stronger spending

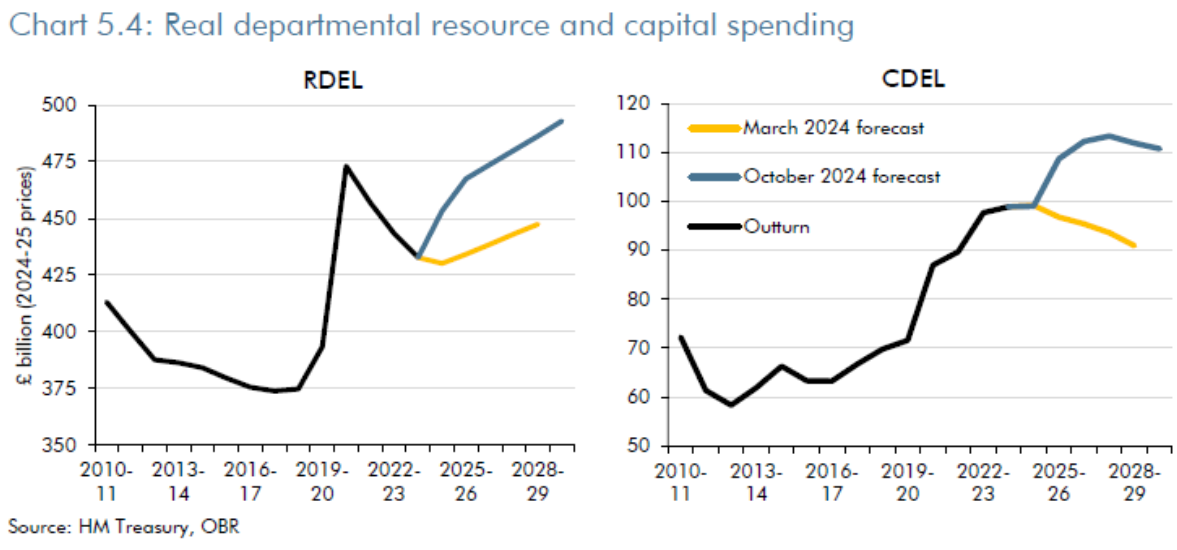

The OBR report includes the following charts to show how public investment and spending on public services has been put on a better course. The left chart measures current spending, which is now up 14 per cent over the next five years (a good 10 percentage points more than in March). The right chart shows capital spending, which ends up 13 per cent above the current level - when previously it was expected to be 8 per cent below.

The changes have been supported by new ‘fiscal rules’: the stability rule on the current budget and the investment rule on debt.

3. Boosting public investment (and the investment rule)

Rachel Reeves announced a series of important capital investment commitments across transport, clean energy, industrial upgrades, housing, health and education.

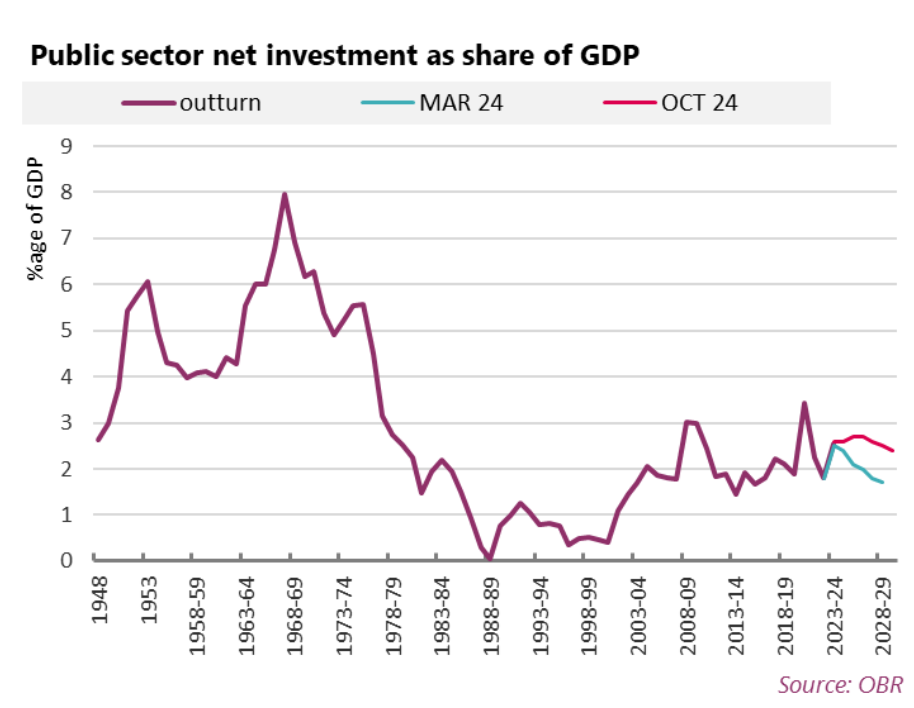

Overall investment is up by over £100 billion over the next five years. Rather than the gradual fall to 1.7 per cent under the Tories, net investment as a share of GDP will average 2.6 per cent over the parliament – meaning the highest investing parliament since the 1970s.

The increase has been supported by a change in the fiscal rules that has been widely welcomed, including by the International Monetary Fund and the former chief economist of the Bank of England. The debt rule is now based on ‘net financial debt’ which includes not just the liabilities on a government’s balance sheet, but the full range of the financial assets too Underneath this change is plain common sense: those who invest for the future, end up better off. The Budget recognises that “Investment today drives future productivity growth and higher living standards."

The changes means that when publicly owned entities, such as the new National Wealth Fund, invest for a future return, they strengthen the state’s balance sheet. This is common practice across European economies and it’s well past time the UK caught up.

Overall the government’s new debt target rises from 83.5 per cent to 84.2 per cent in 2026-27, but then falls each subsequent year to 83.4 per cent in 2029-30. In fact the investment rule requires the target initially to be falling after five years, but then switches to a rolling three year approach. At present it is met sooner than needed.

Great British Energy In previous announcements, Government has committed to capitalise the new public energy company Great British Energy with £8.3 billion over the course of this parliament, and established its remit, including to develop clean power projects and retain a public stake to capture public benefit, to develop UK supply chains, and to work with local authorities on clean power projects. The Budget capitalises GBE with £125 million in the first year, to fund its first project development activities. In the immediate term, the National Wealth Fund will make initial investments for GBE, ensure these are out of the door as quickly as possible.

Great British Energy could be transformative both for the energy sector workforce and for revenues for the state. This is exactly what GBE’s equivalents in other countries are: Orsted in Denmark, EDF in France, and Vattenfall in Sweden. But to do this, over the next years, government needs to show ambition to grow GBE over the long term.

Investing into Manufacturing and Net Zero Previously, the government had already committed to the £7.3bn National Wealth Fund. Beyond the National Wealth Fund, the Budget contained investments into several important manufacturing and net zero sectors and projects, including

- £975 million for R&D in the aerospace sector

- Over £2 billion for the automotive sector up to 2030, for the zero-emissions vehicle manufacturing sector and supply chain.

- £134 million towards port infrastructure to facilitate floating offshore wind

- £3.9 billion in 2025-26 for the first carbon capture and storage (CCUS) clusters in the UK

There was also £2.7 billion of funding to continue Sizewell C’s development through 2025-26 – however, the final investment decision is only expected in next year’s spending review.

The Warm Homes Plan was also allocated £1 billion for next year, with at least £3.4 billion over the coming three years. A further £1 billion over three years will go towards decarbonising public buildings through the Public Sector Decarbonisation Scheme.

Health and education: big increases for capital investment of £1.8bn (+15%) on health and £1.2 bn (+19%) on education between 2024-25 and 2025-26.

Transport: Important commitments to upgrading the UK’s railways included:

Confirming funding to tunnel from Old Oak Common to Euston to ensure HS2 trains terminate in central London

Delivering the Transpennine Route Upgrade between York and Manchester, via Leeds and Huddersfield, and maintaining momentum on Northern Powerhouse Rail

Committing to East West Rail between Oxford, Milton Keynes and Cambridge

£1.6bn is allocated to “repair and renew the nations’ roads”. Unlike under the Conservatives, where transport infrastructure announcements were often made and then quickly downgraded to “illustrative options”, these announcements are fully funded.

Building stock: £5bn was announced to for housebuilding to support the government’s target of 1.5m new homes over the next five years. The Affordable Homes Programme was given an additional £500m to take its budget to £3.1bn. £3bn of support in guarantees to boost the supply of homes and support SME housebuilders – as well as specific investment highlighted for Liverpool Docks and Cambridge.

4. Boosting current spending (and the stability rule)

The government has acted to stabilise and support public services.

Departmental spending on public services is up by £22.9bn this year rising to £48.8bn by 2029-30 compared to the March forecast – growing in real terms by 4.8 per cent this year, 3.1 per cent the year after and by an average of 1.3 per cent over the remaining years of the forecast.

The Treasury Budget document (Table 1.9) includes a detailed assessment of the 2025-26 position by department, with the particuarly welcome gains on the year for health and social care (3.4%), education (3.5%), justice (4.3%) and local government (10.2%).

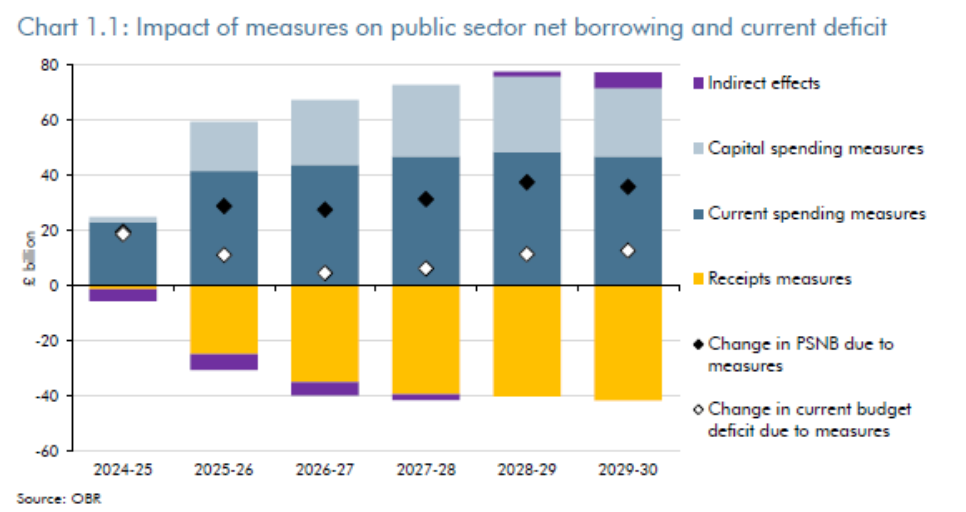

The government’s stability rule requires day to day spending to be matched with taxes, so the increases in current spending (in light blue on the chart below) are broadly matched with increased taxes (yellow).

The rule requires the current budget to be in surplus in the fifth year of the forecast, again switching later to a three-year rolling target. At present this is met sooner than necessary, with a move into surplus of £10.9 billion in 2027-28 after a deficit of £5.3bn in 2026-27.

5. Fairer taxes

The tax increases operate overall to switch the burden from work to wealth and to those who can best afford to pay. The income raised directly funds UK public services and fixing the foundations of the economy.

Among the biggest revenue raisers:

- An increase to the rate of employer National Insurance Contributions to 15 from 13.8 per cent and reduction to the payment threshold, partly offset by changes to the employer allowance to protect smaller businesses will yield £23.8 billion in 2025-26, growing to £25.7 billion in 2029-30. Many commentators already seem to want to have this as a tax on work – but there is no direct link between employer national insurance costs and wages, and as the Low Pay Commission has shown reducing wage bills is seldom the primary means by which employers absorb higher costs.

- Capital Gains Tax (CGT) will increase from 10% to 18% for those paying the lower rate, and 20% to 24% for those paying the higher rate, raising £2.5 billion by the end of the forecast. The Treasury stress the UK will continue to have the lowest CGT rate of any European G7 country.

- A new residence-based regime will replace the current non-domicile regime from April 2025, raising a total of £12.7 billion over 2026-27 to 2029-30.

- VAT on private school fees will raise £1.7 billion in 2029-30.

- Reforms to inheritance tax will raise £2.7 billion by 2029-30.

- Over the next five years HMRC, will look to close the UK’s tax gap – the amount of uncollected tax owed to the UK – by bringing in an additional £6.5 billion per year. This will include legislation to change who has responsibility to account for Pay As You Earn (PAYE) where an umbrella company is used in a labour supply chain to engage a worker (expected to protect around £2.8 billion from being lost to umbrella company non-compliance over 2025-26 to 2029-30).

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox