Our new government must address the burgeoning household debt crisis

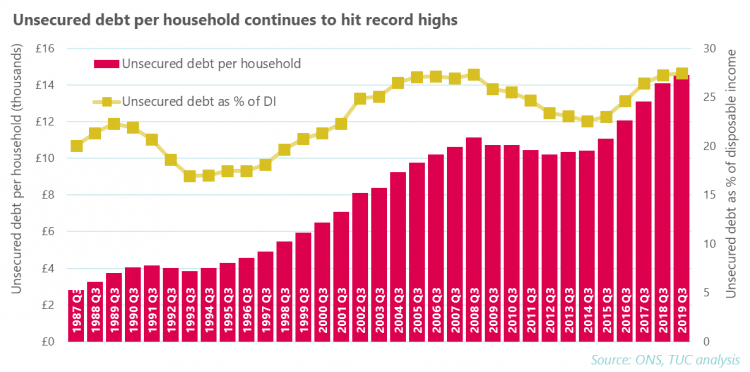

Household debt has risen to a new record high. The most recent figures, for the third quarter of 2019, show that the average amount of unsecured debt per household is up to £14,540. That’s a rise of over £400 compared to the same period last year.

Unsecured debt is any debt that isn’t backed by property. This includes credit cards, purchase hire agreements and student loans, and excludes mortgages.

Unsecured debt as a percentage of disposable income has hit 27.5 per cent, which is also a record high for the period. The previous high was 27.3 per cent, in both 2018 and 2008.

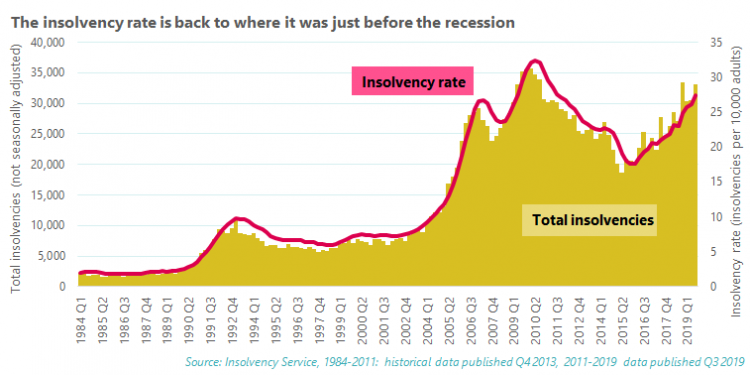

The third quarter of 2019 also saw a worrying rise in the number of individual insolvencies . An insolvency occurs when someone is unable to keep up with debt repayments. Types of insolvency include bankruptcies, individual voluntary arrangements (IVAs) and debt relief orders.

A 23 per cent increase on the same period last year led to there being just under 31,000 individual insolvencies in the third quarter of 2019 alone. Across the first three quarters of 2019, there were over 93,000 insolvencies in total - the highest level at this point of the year since 2010.

The insolvency rate (the number of insolvencies per 10,000 adults) has been consistently growing since 2015. It currently stands at 27.5, a rate we haven’t seen since the lead up to the financial crisis.

Red flags across the board

Concerns around debt are particularly pertinent just after Christmas. StepChange, the debt advice charity, has highlighted how the pressure to spend during the festive period pushes people into debt, with a third of people saying they’ll be using credit cards to pay for part, or all, of Christmas . On average, it will take these people 7 months to pay off their Christmas debt.

A quarter of people said they would be using ‘buy now, pay later’ options. Services such as Klarna are increasingly offered by more and more online retailers. These allow customers to buy a product from a website, and put off paying until a later date, usually within the next 30 days.

In its mid-year report for 2019, StepChange was already raising concerns about the level of problem debt in the UK. The charity revealed that a record number of people were coming to it for debt advice , with their CEO, Phil Andrew, explaining:

Across the board we are seeing red flags, including worrying proportions of new clients falling into debt due to reduced income, illness or because they rely on credit to pay for day-to-day living expenses. Clearly more and more households are struggling to hang on and are ill-equipped to deal with any economic shocks the future may hold.

Action needed now, not in 2024

Tackling debt will involve tackling the causes of debt. Working people should be being paid enough to live on, including setting a bit aside to cope with the surprises and shocks that inevitably happen to us all. In reality though, a fifth of working people aren’t being paid a real living wage.

The government’s aim of raising the minimum wage to £10.50 by 2024 isn’t good enough. We need a living wage as soon as possible, not the conditional promise of one in four years’ time. We also need to give unions the right to access workplaces, so we can tell individuals about the benefits of joining a union and help them to fight for better pay.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox