The OBR’s evidence is clear: the Autumn Statement has done nothing to end the living standards and growth crises

• The politically charged National Insurance cut makes the smallest dent in the worse squeeze on household incomes since the 1950s.

• While the Chancellor has enjoyed higher revenues, he has chosen to play austerity politics rather than back public services on the brink – £20 billion has been taken from public services to fund the meagre tax cut.

• An ‘Autumn Budget for growth’ has meant the reduced growth in almost every year of the forecast.

• ‘Full expensing’ of capital expenditure is a seriously inefficient way to boost the economy.

• In spite of all the claims to the contrary, the Tories are still presiding over worst deterioration in public finances for more than 100 years.

Real wage and household disposable income crisis unended

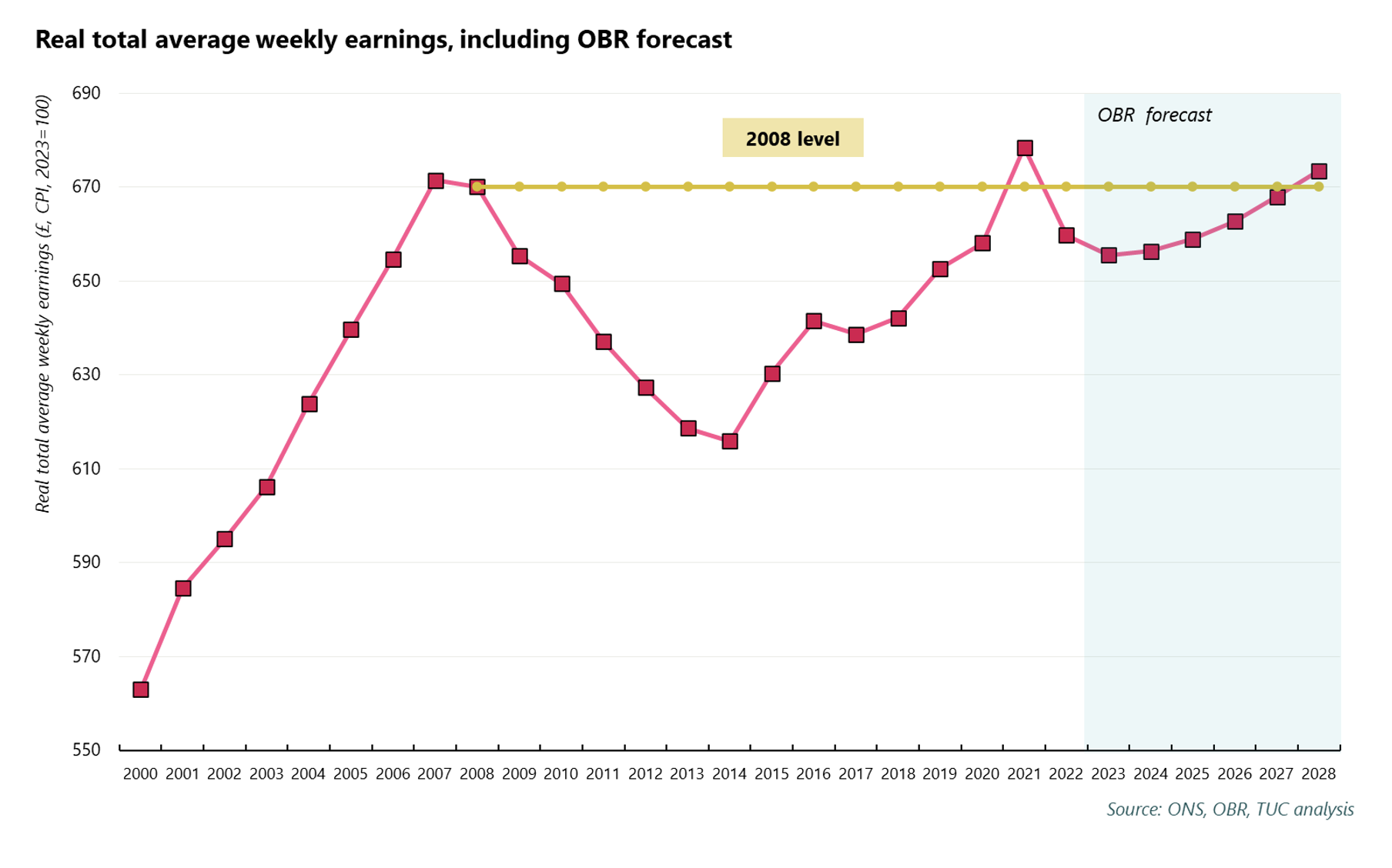

The forecasts published alongside the statement by the Office for Budget Responsibility (OBR) contained alarming news on real wages. According to the OBR forecasts, real wages are now not set to return to 2008 levels until 2028. The current pay squeeze will hit two decades.

This is a significant downgrade on the March forecast, when wages were returning to 2008 levels by 2026 – two years sooner than it now expects.

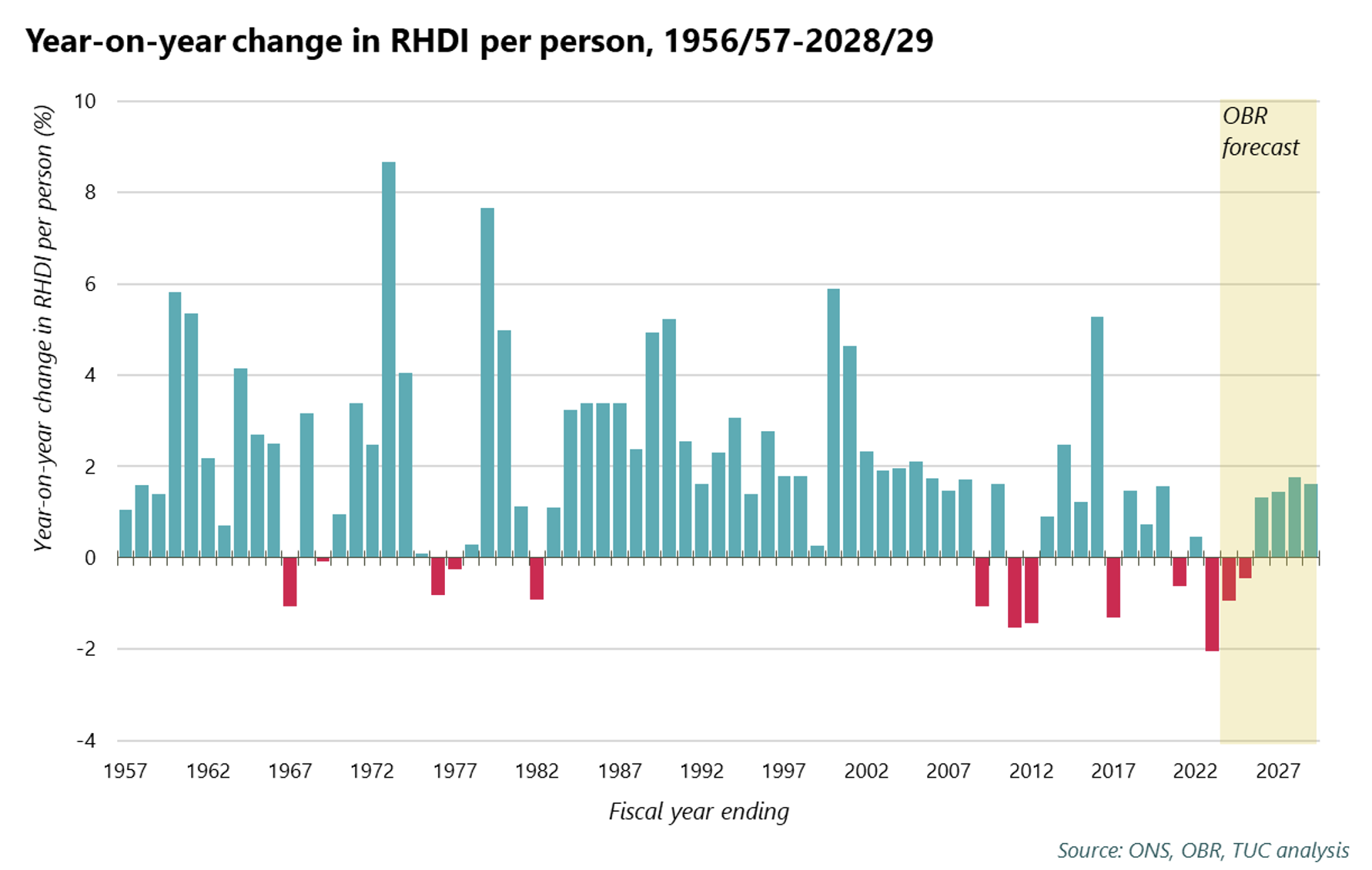

The forecast for broader living standards (as measured by real household disposable income per person) remains dire. After already declining in both the 2020/21 and 2022/23 financial years, further falls are expected over the next two.

While in fact a less bad forecast than March, the OBR stress that living standards “are forecast to be 3½ per cent lower in 2024-25 than their pre-pandemic level … this … represents the largest reduction in real living standards since ONS [Office for National Statistics] records began in the 1950s”.

The OBR also put into perspective the 2 per cent cut in National Insurance, reckoning it will boost living standards by around 0.5 per cent at the end of the forecast. This is a minor dent in an immense collapse, and of course as everybody has pointed out only reverses in a small way tax increases at past statements - even on their own terms the government are failing.

Minimum wage

Specifically for those on the minimum wage, the Chancellor has accepted the recommendations of the Low Pay Commission (LPC). This takes the wage floor to £11.44 an hour and extends coverage to everyone aged 21+. This is badly needed and follows pressure from unions and low-pay campaigners. But with prices sky high, and the OBR increasing its inflation forecasts, the minimum wage must be raised to £15 as soon as possible, and extended to all adult workers.

The Low Pay Commission’s recommendations take the minimum wage to 66% of median wages. This is an internationally recognised measure of relative low pay. However, the Chancellor’s claims that he has eliminated low pay should be taken with a pinch of salt. This is a measure of pay distribution which looks at how close low-paid workers are to the median worker. The floor has risen since 2010 but the middle has had no real pay rise over 13 years. The bottom has been catching up, in part, because wages are stagnant for everyone else. The government should set the LPC’s next minimum wage target at 75% of median wages, and this should be delivered alongside a plan for real wage growth for all workers.

Unemployment rise

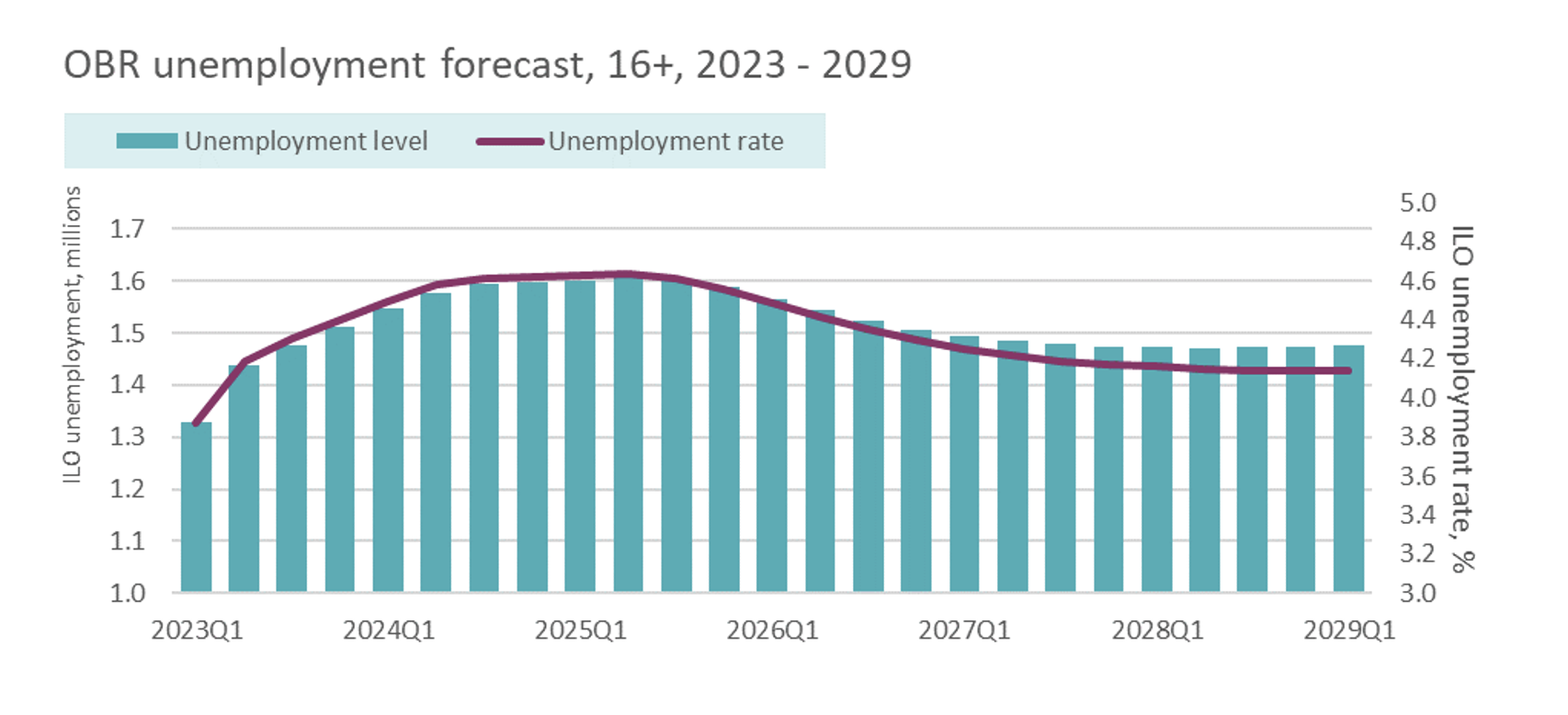

The OBR has also predicted that unemployment will steadily rise from now until midway through 2025, estimating there will be 275,000 more people in unemployment than at the start of this year. At no point in the OBR forecasts do they predict unemployment will fall below the level at the start of the year.

It is unfair to put it mildly to penalise individuals for an economic climate which is out of their control. The Chancellor decided to support compulsory work placements, but analysis show this punitive policy does not result in an improved employment outcome.

Skills

The Government plans focus largely on reforms coming in for 16-18 year olds, overlooking the skills gap faced by those already in the labour market. On apprenticeships £50m for a 2-year pilot widely misses the mark. In 2021/22, there were approximately 349,200 apprenticeship starts in England - a 31% decline from the pre-Apprenticeship Levy figures of 509,400 starts in 2015/16 (Source: CIPD). The funds are largely directed at male-dominated sectors, according to the Women’s Budget Group. Other measures are recycled and/or small – though the increase to the pitifully low apprenticeship minimum wage is be welcomed.

Little has been done to reverse cuts to adult and further education budgets since 2010, with spending still significantly below where it was when the government took office. Celebrating an uptick in Level 4 apprenticeships just repeats the ‘virtuous cycle’ where those with the highest levels of qualification receive the most investment in their training. Graduates get most of the training as working adults, and almost half of adults from the lowest socio-economic group receive no training at all after leaving school.

Social security

It is a low bar for this Government when they boast that benefits are being uprated in line with September’s rate of inflation, which is standard practice. Though they have severed the link between inflation and the uprating of benefits numerous times since 2010 – which has slashed vital financial support for families.

And while the Local Housing Allowance has been restored to the 30th percentile after it was last frozen in 2020, it will be frozen again and support reduced for ever-increasing rental prices.

There were also significant cuts to benefit entitlements for some people with long term health conditions. They are expected to lose £400 a month compared to current system, and face the threat of sanctions to enter employment.

The rate at which prices are increasing may have slowed, but families are still struggling with the essentials. Over the last two years the cost of energy has increased by 49 percent while food prices have increased by 28 percent.

Energy prices

And energy bills are a glaring omission from this Autumn Statement.

Household energy bills remain 50% higher than they were in the winter of 2021-2022 (approximately £600 higher for an average household). This means that an estimated 6.3 million households are in fuel poverty (spending more than 10% of their income on energy), and more than 1 million households are in extreme fuel poverty (spending 20% or more of their income on energy). (Estimate by Friends of the Earth and National Energy Action as government data are not yet available.)

Energy prices are expected to remain high or increase. Ofgem today raised the domestic energy price cap by 5%, based on wholesale price volatility.

Many employers will also struggle with rising and volatile energy bills. The UK consistently has some of the highest electricity prices for business in Europe, affecting the ability of UK manufacturers to compete internationally. Unions representing manufacturing workers have consistently campaigned alongside employer bodies for measures to rein in excessive and volatile wholesale energy prices – but these issues seem to be far from the list of priorities of the current Government.

Public services and public finances crises continue

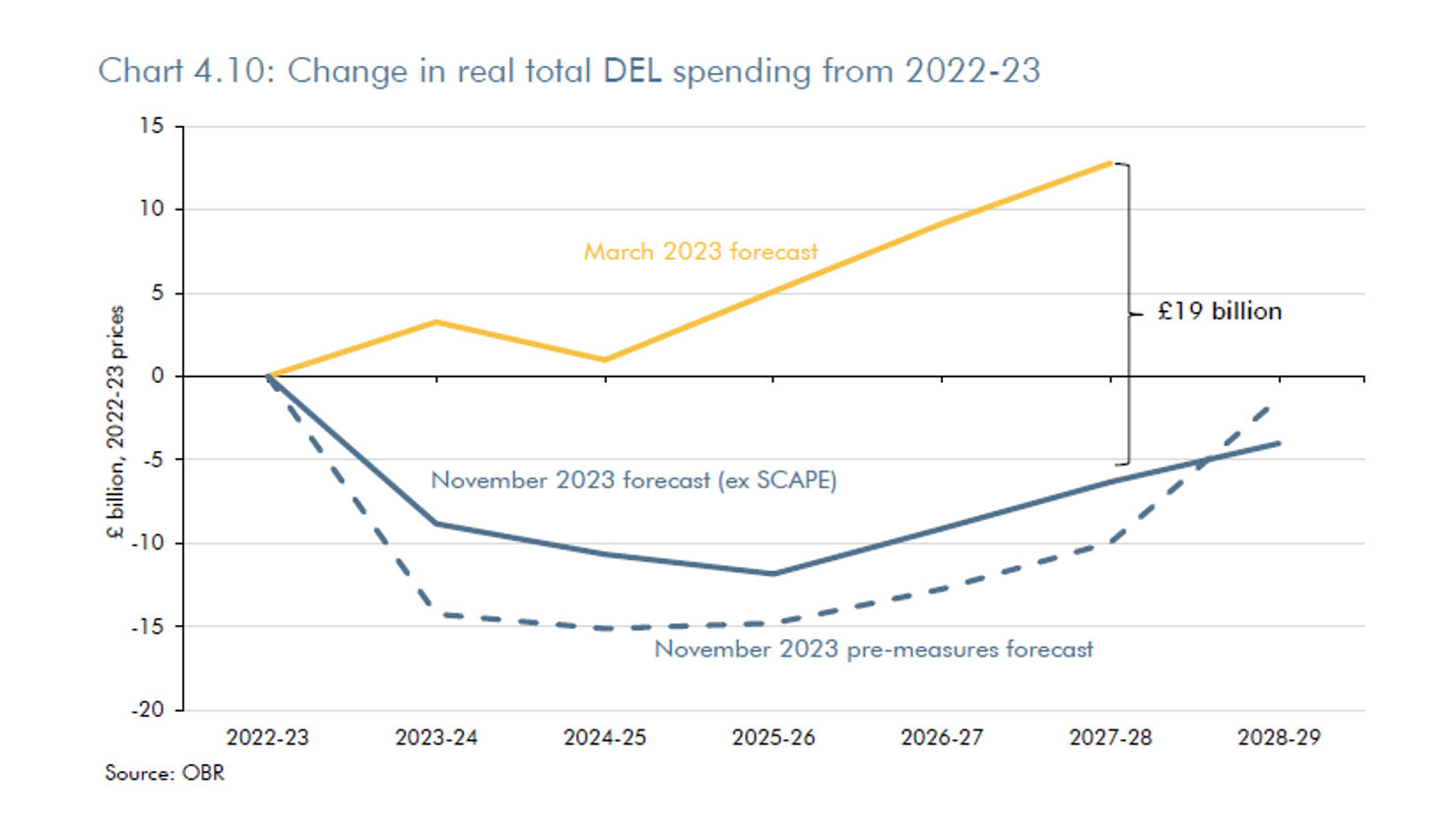

As the OBR gently warn, “it is worth dwelling for a moment on something the Chancellor didn’t announce in his Autumn Statement – which is any major change to departmental spending plans despite significantly higher inflation”.

The government has added “just” £5 billion a year in cash terms to departmental budgets, and this means that “the real spending power of these budgets is eroded by around £19 billion” relative to the previous forecast (as on their chart below).

In 2023-24 the increased budget is allocated for public sector pay increases (£3.9 billion for the NHS in 2023-24, and £0.4 and £1.4 billion for other departments in 2023-24 and 2024-25, respectively). Overall, the OBR have departmental spending growing by 0.9 per cent a year in real terms, down from 1.1 per cent at the March Budget.

Given the government’s political priorities on spending, the OBR stress that unprotected departmental spending is projected to fall by between 2.3 and 4.1 per cent a year in real terms from 2025-26. They wryly observe this (austerity) would “present challenges” and cite the Institute for Government’s recent report finding that “performance in eight out of nine major public services has declined since 2010”. Plainly there is no intention to resolve the crisis in public services and public service recruitment. And ultimately

The public finances overall

For the public finances as a whole, the government has enjoyed a momentary windfall – with less bad than expected growth outturn and higher inflation meaning tax gains (especially with tax thresholds not being uprated) outweighing higher interest and other costs. This has been spent on the NI cut and expensing.

But the Chancellor has made hollow boasts about the improved condition of the public finances. The overall management of the economy for 13 years has meant a disastrous failure for them. Immediately less bad GDP outcomes (next section) have meant marginally improved ratios for this statement. But overall the Conservatives have presided over a huge increase in debt from 65 per cent of GDP in 2009-10 to 98 per cent of GDP in the current financial year. This is an unprecedented deterioration relative to all economic cycles for more than a century.

Growth crisis unended

At the end of his speech the chancellor proclaimed an “Autumn Statement for Growth”. But nothing announced yesterday changed the bottom line. While the forecasts reflected ONS revisions to GDP data and a less bad than expected 2022, growth over the next two years is revised steeply down. And on a medium term view the OBR warn:

"we have revised DOWN our estimate of the medium-term potential GROWTH rate of the economy to 1.6 per cent, from 1.8 per cent in March" (our emphasis)

The worse growth performance for the UK economy in a century just got worse again.

“Full expensing”

Of the onslaught in policy measures, the most prominent was making permanent the full expensing of business capital investment. The Chancellor chose to disregard OBR analysis showing both precursor measures (the super-deduction and temporary full expensing in the March 2021 and March 2023 Budgets) had a lower impact on investment levels than predicted (see OBR, Economic and Fiscal Outlook, November 2023, pp 33 – 34).

Introducing full expensing is forecast by the OBR to lead to an increase in business investment of £14 billion between now and 2028-29 and to cost £29.5 bn over the same period. This would appear then to be an extremely inefficient means of increasing business investment, reflecting huge ‘deadweight’ effects, whereby businesses gain generous tax relief on investment that would (likely) have taken place anyway.

The OBR estimates that the measure will raise the capital stock by 0.2 per cent by 2028-29 – a positive, but small, and very costly impact.

Pension saving

The chancellor also had high hopes for the role workers’ £2.5tn of pension savings could play in boosting our flagging economy. But while there were some welcome steps such as setting up a new growth fund through the British Business Bank the plans rely mostly on merging pension schemes in ways that are unlikely to be in the interests of their members, and leaning on funds to put more money into global private equity. These measures were also over shadowed by a poorly thought through proposal to upend the workplace pension system. See our fuller commentary here.

Industrial strategy?

As the Chancellor noted, the lack of long-term certainty over policy decisions (including industrial strategy, taxes, and climate commitments) is a drawback to business decisions to invest. But there was no reassurance in the Autumn Statement that the Government would provide that certainty. While reannouncements of investment commitments to support the automotive, advanced manufacturing, and energy sectors – amounting to £4.5 billion are welcome, this represents only a small proportion of the investment requirements of the Biden-style industrial strategy that the UK needs.

Ending the failure

The failure – as Labour have repeatedly identified – is still a failure of growth. The government need to invest in a stronger economy where growth and fairness go hand in hand, where decent pay means workers spend and businesses produce to meet that spending. A virtuous cycle comes when businesses invest in the face of expansion and optimism, and stronger public services re-enforce the upward dynamic. Fairer and sustainable growth will then support the public finances. Yet the government continues to take us in the wrong direction. Yesterday’s Autumn Statement showed more strongly than ever why it is time for a change.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox