Nationalising water is affordable, keeping it private might not be

The Social Market Foundation (SMF) released a report yesterday arguing that nationalising the water industry could cost £90bn and lead to a decrease in investment.

The report is in line with others that make similarly dire warnings. The Centre for Policy Studies recently put a figure of £86.5bn. These might seem like huge amounts, but the cost of keeping it private could be much higher.

SMF admit that their figure is only one of a range. Different methodologies will calculate different figures, based on how we value the industry and what costs we think the government would be liable for. The claim that the government would have to pay market rate for the service, for instance, is disputable.

For a hypothetical, let’s allow that the figure is accurate. I want to ask whether this £90bn valuation will end up as a cost to the tax payer, and if so whether it might not still be cheaper than the eventual cost of carrying on as we are. You probably won’t be surprised to learn I think the answer to the first question is “probably not” and the answer to the second is “probably yes”.

Advocates of nationalisation (including myself) say that the cost to the tax payer would be minimal, because interest rates are so low. Initially the government will need to issue debt to transfer ownership. This does not add to the stock of debt in the economy, but moves it from the private sector to government sector. As such it is unlikely even at face value to increase interest rates, so the cost of servicing the debt is unlikely to increase. And at the same time the government gets a big, new asset on its books. That means the government could borrow the money to purchase the services, and then the value derived from the services supplied and assets gained would likely cover the cost.

SMF warn that should the government buy out the 9 companies that currently provide water and sewage treatment in England (Wales, Scotland and Northern Ireland have their own systems) then the current rate of interest at which government can borrow would increase, as the market would be spooked by the spectre of a nationalising government.

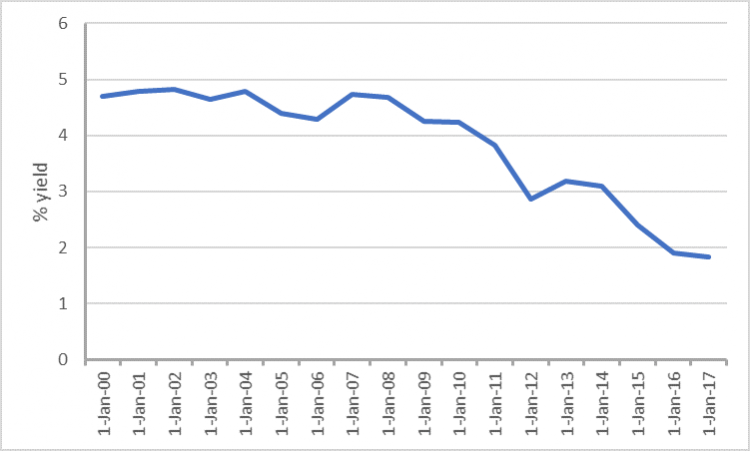

The assumption here is that issuing debt to take a service back into public ownership will appear to the markets as fundamentally different from the massive debt that governments have taken on over the past decade, during which rates have remained low. I think this argument is fundamentally unsound. If we consider interest rates over the past ten years, during which time the government engaged in a period of massive spending to bail out banks (effectively partial nationalisation), then drastically cut back government spending, before opening the proverbial taps again, with the programme of quantitative easing, during which the yield on government debt has stubbornly refused to rocket. Despite the fluctuations in government spending, the market remained confident that government debt is a safer bet than the alternatives.

20 yield on government debt

It is possible that the market would change their mind about this following a change of policy, but it seems unlikely that they would subsequently revise their opinion so decisively that it would result in interest rates that rival or exceed the commercial rate.

Even if they did begin to approach this level, it may still be cheaper to take the industry into public ownership as the government would not be obligated to pay dividends to shareholders. Over the last ten years Anglian, Severn Trent and Yorkshire water all paid more in dividends than they generated in profits. The gap is made up by huge debts. Companies that were debt free when privatisation occurred in 1989 owe a total of £40bn. This borrowing has financed over three-quarters of their assets. This has funded the majority of the £126bn that the SMF report holds up as a mark of the success of privatisation. Without the need to pay shareholders, government would not need to take on debt to carry out investment.

And this debt is the crux of the problem. Because, as we have seen with Carillion, with Southern Cross, and across the rail industry the fact is that if this highly unstable, industry collapses it will be the government that has to step in anyway. Privatisation is meant to transfer risk as well as profits away from the tax payer and onto the company. But for a service as essential as water, the tax payer is always the backstop.

Better to invest in bringing these assets into public ownership when we can, rather than have to pay more to bail them out when we must.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox