Mrs May's legacy: the 'just about managing' are worse off today than when she took office

- When Theresa May became prime minister, she promised to stand up for working families who were ‘just about managing’ to make ends meet.

- But according to new TUC analysis, households have spent on average £2,000 more than they earned over the period May’s been in charge.

- The next prime minister must forget Conservative in-fighting and take urgent action to improve pay and living standards.

When Theresa May became prime minister in July 2016, she promised to stand up for working families who were 'just about managing'.

The so-called ‘JAMs’ are people from working families who worry about paying their mortgage, the cost of living and getting their kids into a good school.

But as Mrs May prepares to vacate Downing Street, it’s now clear that they’re significantly worse off today they were the day she took office.

According to new TUC analysis, households have spent on average £2,000 more than they earned over the period May’s been in charge.

That’s £54 billion in total – the first income shortfall in 30 years.

This hasn’t been driven by excessive spending, but by stagnant incomes. Thanks to almost a decade of austerity, people simply aren’t earning enough to get by.

So rather than just about managing, many working families just aren’t managing at all.

Households drowning in debt

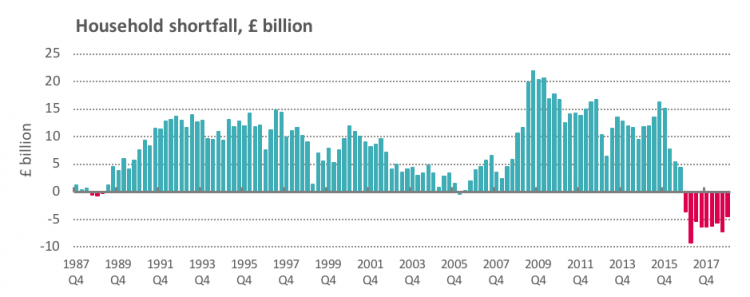

Let’s put Mrs May’s performance in context. The following chart examines how household budgets have changed over the last 30 years.

We can see that in every quarter since Theresa May became PM in July 2016, household outgoings have outstripped income (2016Q4 to 2018Q4):

The total shortfall is now £54bn across all households – an average of £1,964 per household.

In July last year, the ONS pointed out that the annual shortfall for 2017 of £900 per household (now revised up to £990) was the first for 30 years.

Even in the run-up to the 2008 financial crisis – an era of 100% (or more) mortgages – we never reached a point when the average household was a net borrower.

And that shortfall has now continued for a whole more year.

Bust not boom

The only other recorded shortfall came in the late 1980s during the so-called ‘Lawson boom’, when the Tories lost control of the economy. Yet even then outgoings lagged behind incomes for only three quarters (1988Q3-1989Q1).

During the three negative quarters of the ‘Lawson boom’, real terms spending grew by an annual rate of 6½ per cent, while income increased by 5½ per cent.

But over the six quarters of the May premiership, household spending has grown by an average annual rate of only two per cent. Meanwhile average disposable incomes have only risen by one per cent a year on the back of incredibly weak wage growth.

So households are borrowing today just to maintain a basic standard of living, unlike in the heady (though deluded) 1980s boom.

Wages going nowhere

In 2018 real pay (or pay adjusted for inflation) finally started to rise. But as so often in the past decade, growth has now stagnated.

That means the chance of any change in household budgets is unlikely any time soon. And our own research suggests that what little wage growth there has been went to the better off.

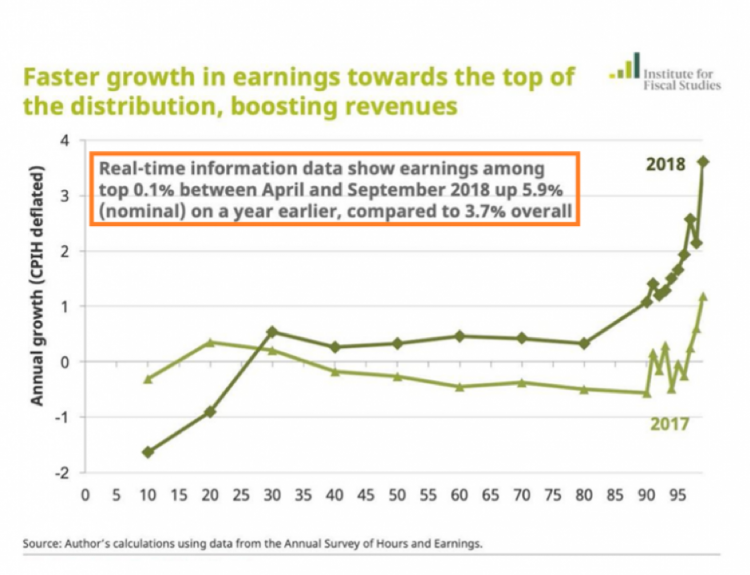

The IFS chart below examines real (weekly) pay growth across the income distribution between April 2017 and April 2018.

It shows that 90 per cent of the population has barely had any pay increase – and the lowest earners have actually seen their pay drop. By contrast pay has shot up for the top 10 per cent of earners.

Welfare cuts

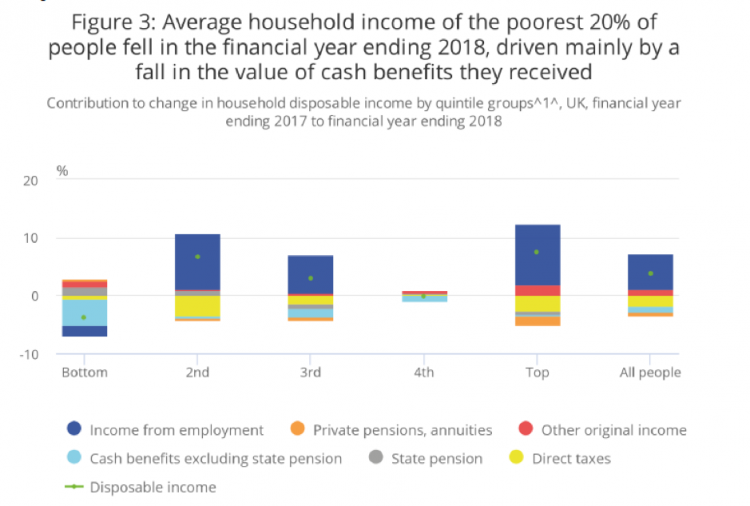

Just last week the ONS released figures showing how the government themselves has made the impact of re-emerging pay inequalities even worse. The headline of the ONS chart says it all:

Government welfare cuts have caused a "10.4% decline in the average real value of benefits (excluding state pensions) households received".

This is what led a UN poverty expert to describe the government’s welfare policies as a “digital and sanitised version of the nineteenth century workhouse, made infamous by Charles Dickens”.

Not exactly what Mrs May promised on the steps of Downing Street is it?

Rising debt

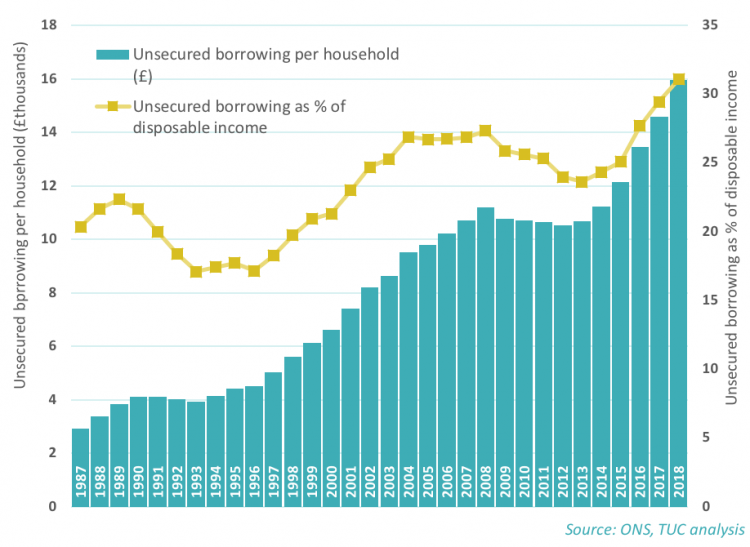

Inevitably, these shortfalls mean households are turning to borrowing. TUC analysis showed unsecured borrowing per household rose to £15,945 in 2018 – the highest figure on record. The sharp rises from 2016 are very obvious on the chart below. Some of that increase will be down to student loans, but so what ?

Needless to say, debt levels among the poorest households are of greatest concern.

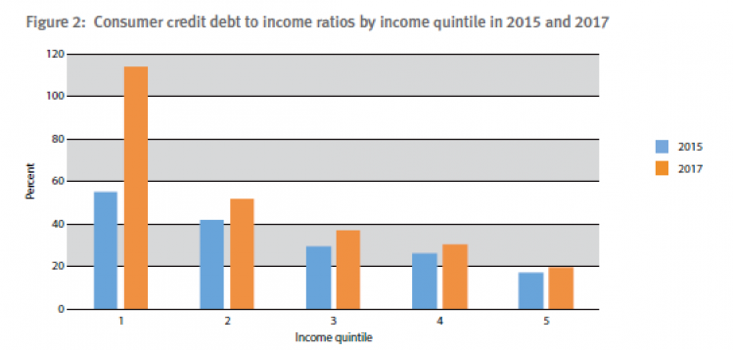

A year ago the Centre for Responsible Credit and Jubilee Debt Campaign showed staggering rises in the consumer credit debt to income ratio for the poorest households, from around 55% in 2015 to 110% in 2017:

Not managing at all

While Theresa May’s government has torn itself to shreds over Brexit, working families have been left high and dry.

In her first speech as prime minister, Mrs May promised to tackle burning injustices. But as she prepares to leave Number 10, pay growth has stalled and millions of people are stuck in low-quality and insecure jobs.

That’s the legacy that Mrs May is leaving behind.

And that’s why we need a prime minister who will actually do something to help the working families who can’t make ends meet without falling into debt.

Methodology notes

The analysis is based on commentary produced by the ONS in July 2018 but extended to look at quarterly figures through to the latest quarter.

The household shortfall is measured by the national accounts net/lending borrowing measure, which compares all household revenues with current and investment expenditures. See the UK economic accounts for the household sector, table 6.2.7. The March dataset is used, with figures extending to 2018Q4:

Household figures are based on the ONS projections issued 3 December 2018.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox