Unsecured borrowing hits another record high

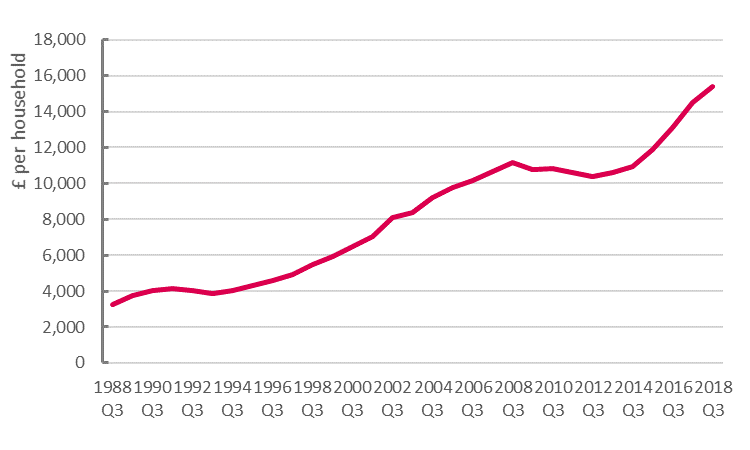

Today the TUC can reveal that debt has hit a new record of £15,400 per household.

Unsecured debt per household (including consumer credit, student loans and pay-day lending but excluding mortgages) rose to £15,400 in the third quarter of 2018 – a rise of £890 on a year ago:

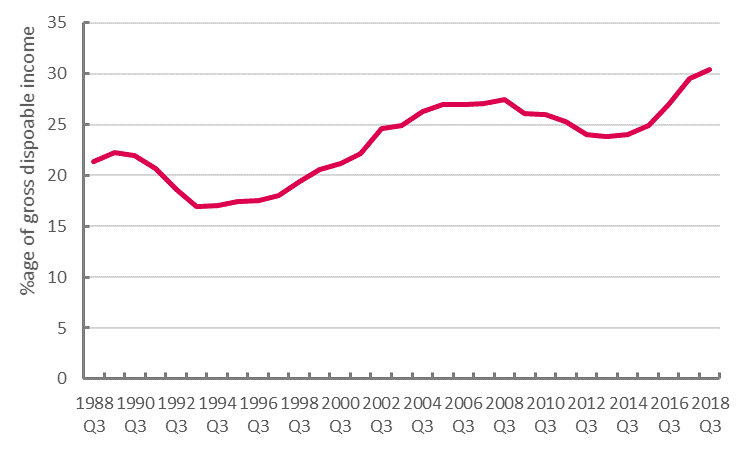

Total unsecured debt has risen to £428 billion. At 30.4 per cent of household income, this is higher than before the financial crisis:

Debt crisis and the ‘May bust’

With households enduring the worst pay crisis for two centuries this is hardly a surprise.

The analysis we produced ahead of the 2018 Congress showed household incomes outstripping incomes every quarter since Theresa May took office.

Official figures show this now continuing for eight quarters, with a cumulative shortfall of £47 billion or £1,700 per household.

This shortfall must be met partly by credit.

Some might charge households with living beyond their means, but this is a very different episode.

During the ‘Lawson boom’ of the late 1980s, for example, spending grew by 6.5% a year and incomes by 5.5%.

But over the ‘May bust’, spending has grown at an annual rate of 1.5% a year and disposable incomes by 0.5% a year.

Evidence of change?

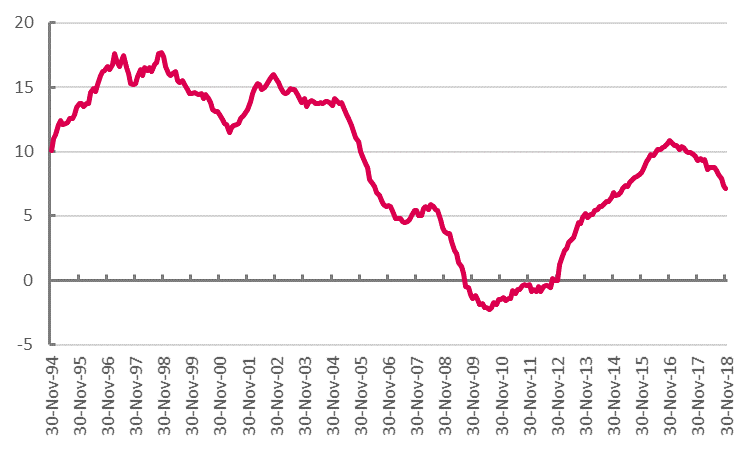

As last week’s figures from the Bank of England showed, there is some evidence of a slowdown in unsecured borrowing.

Consumer credit annual growth has slowed from a peak of 10.9% in November 2016 to 7.1% in November 2018 – with the latter the lowest rate of growth since March 2015.

This in part follows policy action in 2017, as the Bank of England acknowledged concerns about the pace of credit growth.

Moreover, much of the rise in unsecured debt over the year is down to student loans. Of a total rise of £27 billion on the year, the stock of student debt rose £17bn (source) and Bank of England consumer credit figures by £11bn.

But the reliance on credit is still there and for too many the damage has already been done. (And student debt is very much still debt.)

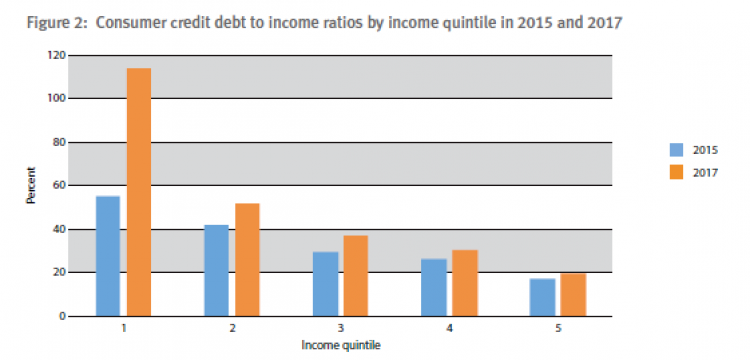

The Centre for Responsible Credit and Jubilee Debt Campaign have shown (unsecured) debt to income for the poorest households rising by a staggering extent from around 55% to 110% from 2015 to 2017:

A failed model

In their 2010 manifesto, the Conservative Party’s central pledge was to “create a new economic model built on investment and savings, not borrowing and debt”. A full page of the manifesto proclaimed:

Since the crisis growth has been unprecedentedly weak, yet it has still been built on borrowing and debt.

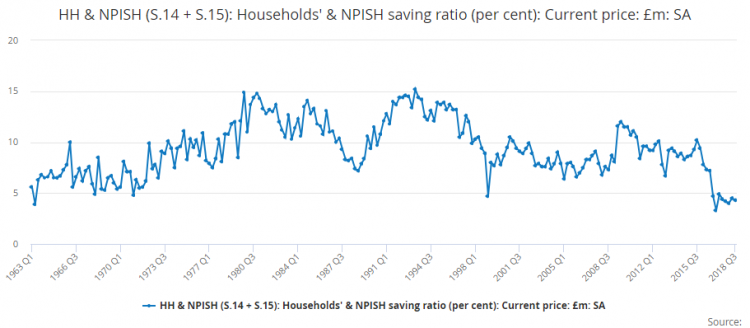

The saving ratio has been below 5% in the eight quarters since Teresa May took office.

ONS figures show that it has been below 5% only four other times since 1963:

Annual growth in investment is now negative.

The Tory model has failed. Austerity has proved a self-defeating strategy.

By smashing the economy, there has been increased not reduced reliance on debt. The biggest victims are those struggling hardest with these debts.

We were never all in it together, and we now know that the weakest – unsurprisingly – are paying the highest price.

Note on methodology: Unsecured debt includes bank loans, payday loans, credit cards, store cards, purchase loans and student loans, but excludes mortgages. The figures are derived from the balance sheet for the household sector, comprising short-term loans issued by UK (NNRG) and overseas (NNRK) banks and building societies and ‘other (i.e. non-mortgage) long-term lending issued by UK residents’ (NNRU). Income is an annual figure derived as a sum of the latest four quarters of household disposable income (QWND). Data sources: UK Economic Accounts, tables 6.1.4 (for income) and 6.1.9 (for debt), Office for National Statistics.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox