To boost living standards, we need to strengthen unions and reverse austerity

Andrew Harrop accuses policymakers of “planning for stagnation”, and in a collection of essays seeks to “take on the sense of fatalism that has overtaken Britain’s economic debate”. My contribution sets out the case for ending austerity and raising public spending for the sake of growth, and I am pleased to be among several arguing “that a less flexible labour market is a strategy for income growth” .

I do so through emphasising the role of demand, as not only critical to understanding what is going on, but also because it opens policy options on a wide and bold front. This blog gives you a short introduction to the argument – hopefully as a taster for reading the whole chapter.

Argument

I start with setting out how a Victorian morality of ‘living within your means’ has imbued government thinking, but makes for very bad economics.

Macroeconomics tells us that, unlike an individual, the government’s actions affect the economy as a whole. It tells us what Henry Ford know all along, that his best prospects for sales came from paying his workers enough to buy cars. These processes play out through aggregate demand, the central insight of the macroeconomic approach (and the mechanism through which Keynes’s policies operated).

Cutting government spending and attacking workers’ power amounts to reducing the overall level of demand in the economy. This is a very dangerous thing to do when the economy is too weak – and is the fundamental cause of the “truly terrible” real incomes. I show how government spending cuts damaged economic growth by far more than expected, not only in the UK but in all 32 advanced countries following a similar approach.

The weak growth is the cause of the pay and incomes crises.

But the weak growth also meant greatly lower government receipts, so that fiscal policy targets have repeatedly been missed – no matter what the government may say about ‘balancing the books’. Public sector debt was expected to peak at 70 per cent of GDP in 2013–14; the peak is now expected in the 2017–18 financial year at 86.5 per cent of GDP.

Over the coming years, the government continues to ignore the lessons of the past eight years. Austerity continues, and debt is barely further reduced, even on an OBR forecast that remains optimistic (on productivity and wages).

I also debunk the widespread suggestion that the cause of the pay crisis is not primarily austerity (i.e. demand) but weak productivity (i.e. supply).

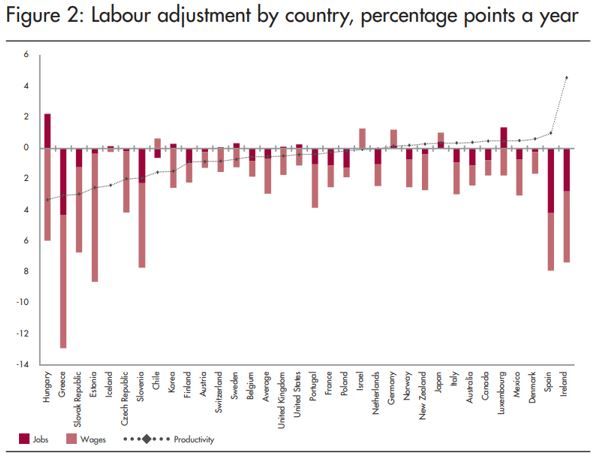

There is a well-established relationship between productivity and pay growth, yet the causality is not clear cut. Eight years of work has failed to uncover any compelling supply-side explanation for the exceptional weakness of productivity since the global financial crisis in the UK and many other countries. Policymakers ignore the possibility that causality is currently running in the opposite direction, with low productivity the result of low wages. On the demand view, bad UK productivity outcomes are the result of the labour market adjusting to (demand driven) weak growth through price – i.e. cuts in wages and the quality of work – rather than cuts in quantity – i.e. jobs.

International figures show the adjustment in other countries has also been skewed to wages, but not as heavily as in the UK.

So the UK has done better than many other countries on jobs, but worse on wages and productivity. This is an awkward contradiction those who think that the answer to our productivity problems lies in further labour market flexibility.

While this self-defeating approach is common to most countries, I show some have stood apart. In Germany, Israel and Japan, government spending was increased rather than cut and they were rewarded with stronger GDP growth, stronger jobs growth, stronger wages growth and stronger productivity growth (see chart above).

The bottom line is that (when the economy is weak) increased government spending boosts demand, strengthens the economy (including the private sector), and is the best way decisively to improve the public sector finances. The demand approach also suggests that both current spending (on public sector wages and services) and capital spending (on infrastructure) are viable and affordable; it also shows why interest rates rises are currently inappropriate.

Andrew Harrop’s call to “end austerity” is welcome and essential.

Other perspectives

On the specific issues discussed above there is a great deal of common ground across all authors, with some helpful additional detail

Several authors discuss the importance of industrial strategies – not least to address industrial and regional imbalances –and the associated investment implications. Emphasis on the ‘foundational’ or ‘everyday’ economy (where the basic needs of society are met – e.g. providing care, producing food, maintaining the environment etc) resonates with demand initiatives. And likewise Dustin Benton’s opportunities from Green initiatives. Onaren and Gushanski from the University of Greenwich offer a full and complementary perspective on demand, leading above all to higher wages. Following from this, virtually all support strengthening unions and voice at work.

But the contributions go far wider than the discussion here, including e.g. financialisation, exchange rate policies and re-distributional initiatives, together amounting to a decisive challenge to ‘fatalism’. It is apt to end with Craig Berry’s call for a ‘grounded capitalism’:

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox