Spring Budget 2024

In last year’s Autumn Statement the Office for Budget Responsibility (OBR) laid bare the dire economic position facing working people and their families. The OBR reported the worst decline in living standards since the second world war, leaving households across the UK facing the poorest performance on incomes across all G7 nations. Real pay is not expected to return to 2008 levels until 2028.

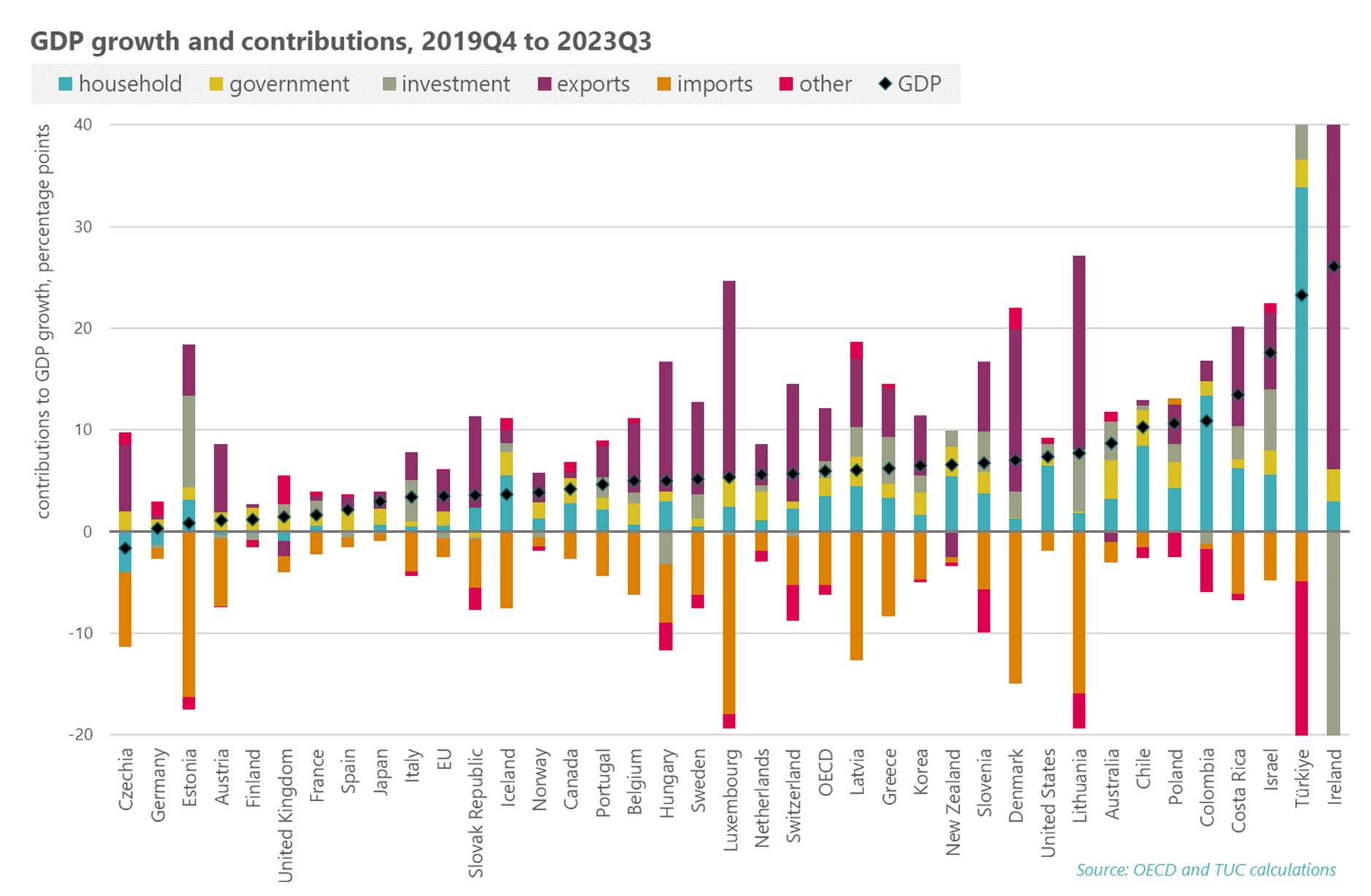

The UK’s wider economic performance since before the pandemic is also among the worst of all advanced economies, with low household incomes meaning outstandingly weak household demand and still terrible export outcomes. Between 2019 Q4 and 2023 Q3:

- UK GDP rose only 1.4 per cent, the sixth worse performance of all OECD countries (average growth 6.5 per cent);

- household spending fell 1.4 per cent, the third worse performance in the OECD (average rise 6.1 per cent); and

- exports fell 4.7 per cent, the second worse performance in the OECD (average rise 9.7 per cent).

Investment in the UK remains exceptionally weak. While growth has increased since 2019 (growing 5.5 per cent, ranking 18 in the OECD), UK investment as a share of GDP was still only 18 per cent against an OECD average of 23 per cent (and ranking fourth from last).

The UK’s economic vulnerabilities are increasingly evident, and a strategy to protect our economy from recession and revive growth and living standards is imperative.

In this submission we show that policy should be aimed at boosting public investment and repairing public services, ending the public sector recruitment and retention crisis. This should be accompanied by real support for jobs and living standards, a minimum wage target of 75 per cent of hourly pay, a jobs guarantee and permanent short time working scheme. Cost of living support should be extended (not halted) and government should set a path to improved social security payments and a new approach for those facing economic inactivity due to their health.

This ambition should be supported by a reformed tax system, so that those who have the very most pay their fair share, and a constructive approach to the UK-EU Trade Cooperation Agreement in 2026. And instead of persisting with draconian and counterproductive regulations on minimum service levels, government should recognise the value that collective bargaining brings for living standards and growth.

This is not the time to repeat the economic policy errors of the past. The last 14 years of failure have hammered the living standards of working people, increased insecurity, decimated public services and left us with the worst economic performance for more than a century (which in turn has pushed up public debt). It is not too late for the government to change course. As ever, should Ministers choose to listen, the TUC stands ready to help.

Living standards under persistent pressure

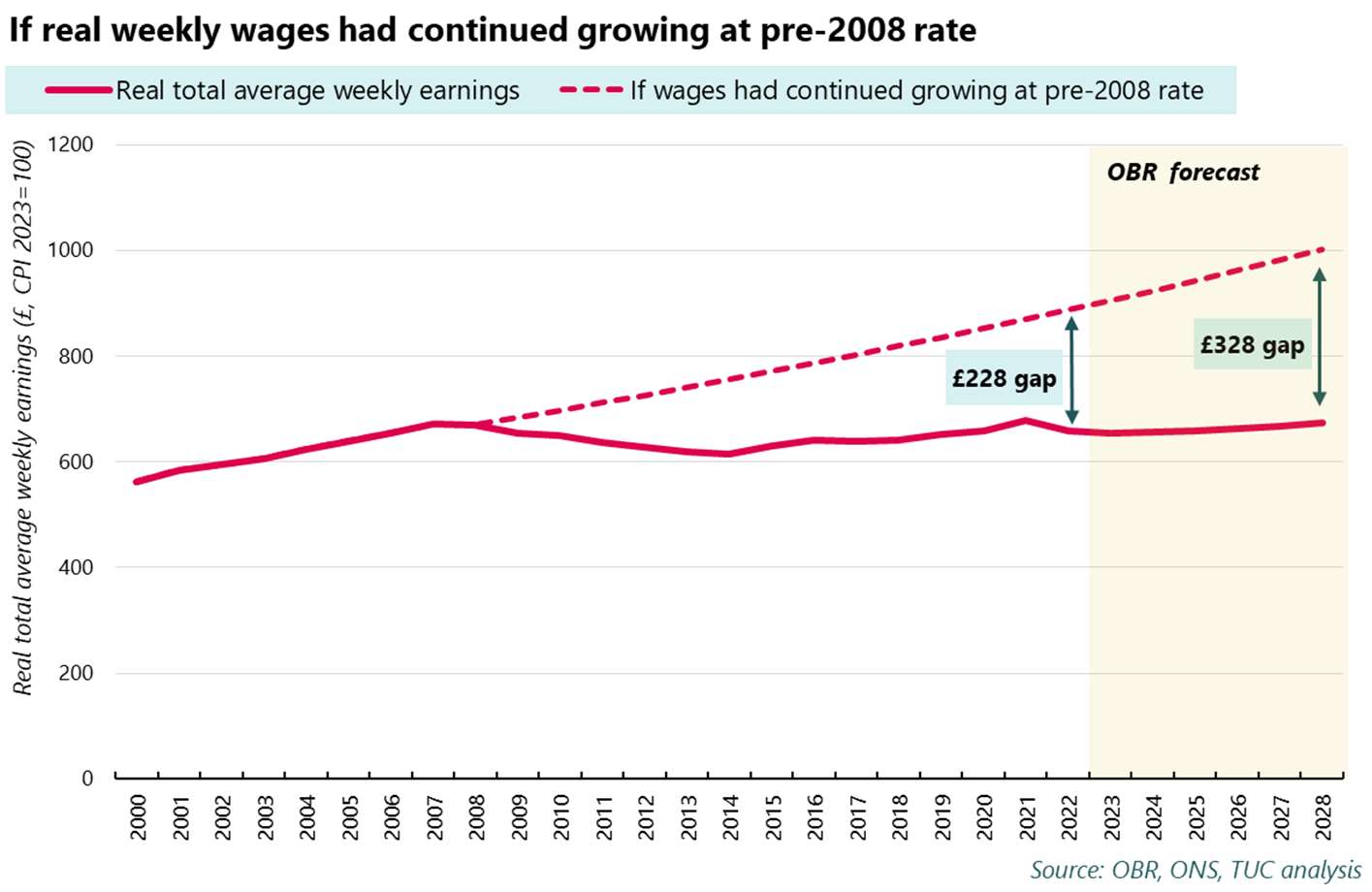

The UK remains in the midst of a two-decade long real pay crisis. Before the financial crisis, real wages typically grew by two per cent each year. Between 2008 and 2022 (the most recent year we have full data for) average real pay growth has been slightly lower than flat (-0.1 per cent). This means that real wages in 2022 remained below where they were in 2008. Based on OBR’s November 2023 forecasts, real average weekly wages are not to set to recover until 2028.

If real weekly wages had instead grown at their pre-crisis trend between 2008 and 2022, they would have been £228 higher by 2022. This equates to £11,900 across the year. By 2028, the gap between real average weekly earnings and where they would have been had they continued to grow at pre-crisis rates is set to grow to £328 (£17,100 across the year).

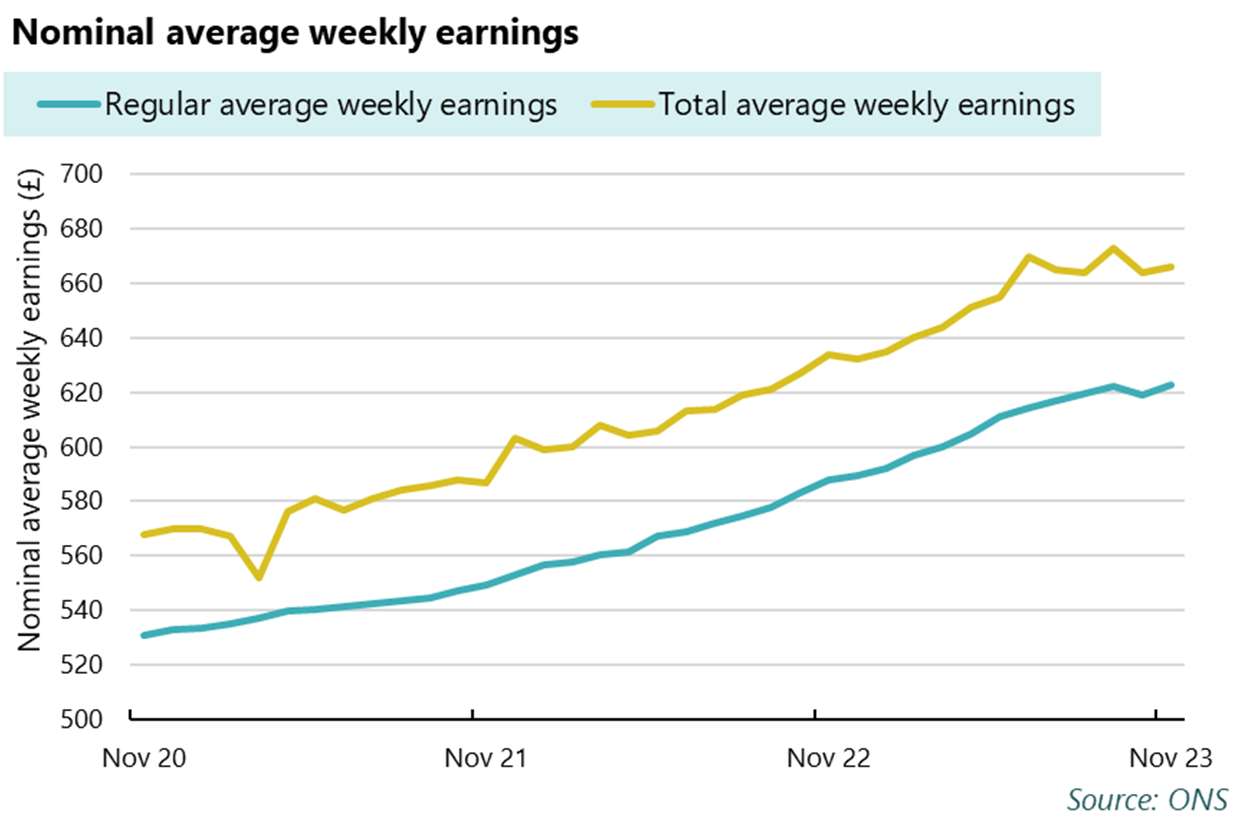

The latest data, covering November 2023, shows that after a period of growth (albeit often lower than inflation) nominal pay growth is starting to slow. This is true for both regular and total average weekly earnings. Quarter-on-previous-quarter regular and total wage growth has dropped to 0.7 per cent and 0.2 per cent respectively, the lowest in two years.

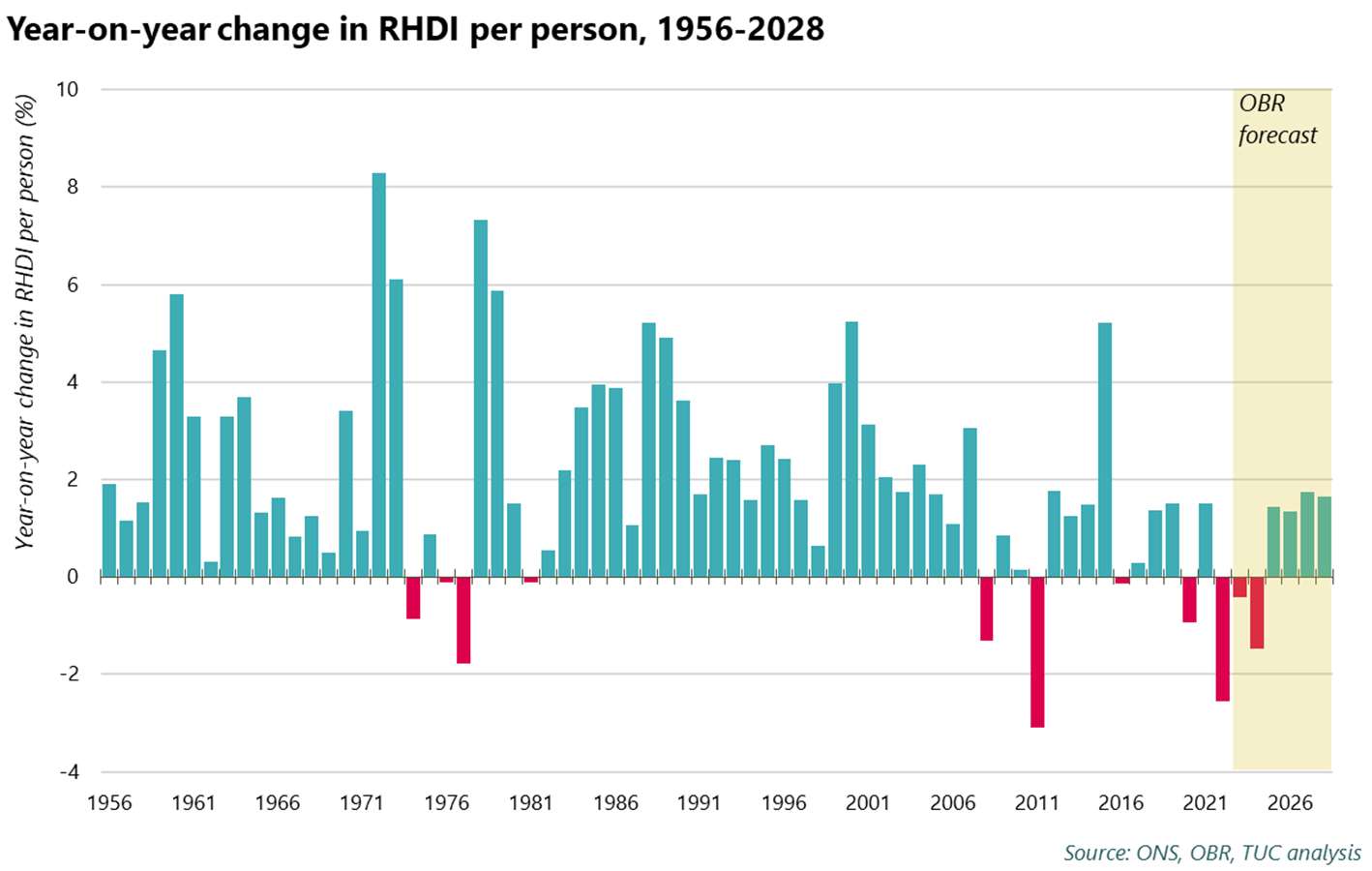

Alongside the pay crisis, the living standards crisis is intensifying. In November 2023, the OBR forecast real household disposable income per person (a measure of living standards) to fall in both 2023 and 2024. This follows a fall in 2022. If this happens, it will be the first time living standards have fallen in three consecutive years since records began in the 1950s.

The period between 2022 and 2024 is set to be, by a distance, the worst three-year period for living standards on record. The 4.4 per cent drop in real household disposable income (RHDI) per person across these three years is over twice as high as the current worst period on record (-2.0 per cent, also under this government, between 2019 and 2022).

UK was 1.2 per cent lower in the second quarter of 2023 than at the end of 2019, compared to a rise of 3.5 per cent, on average, across the G7.1

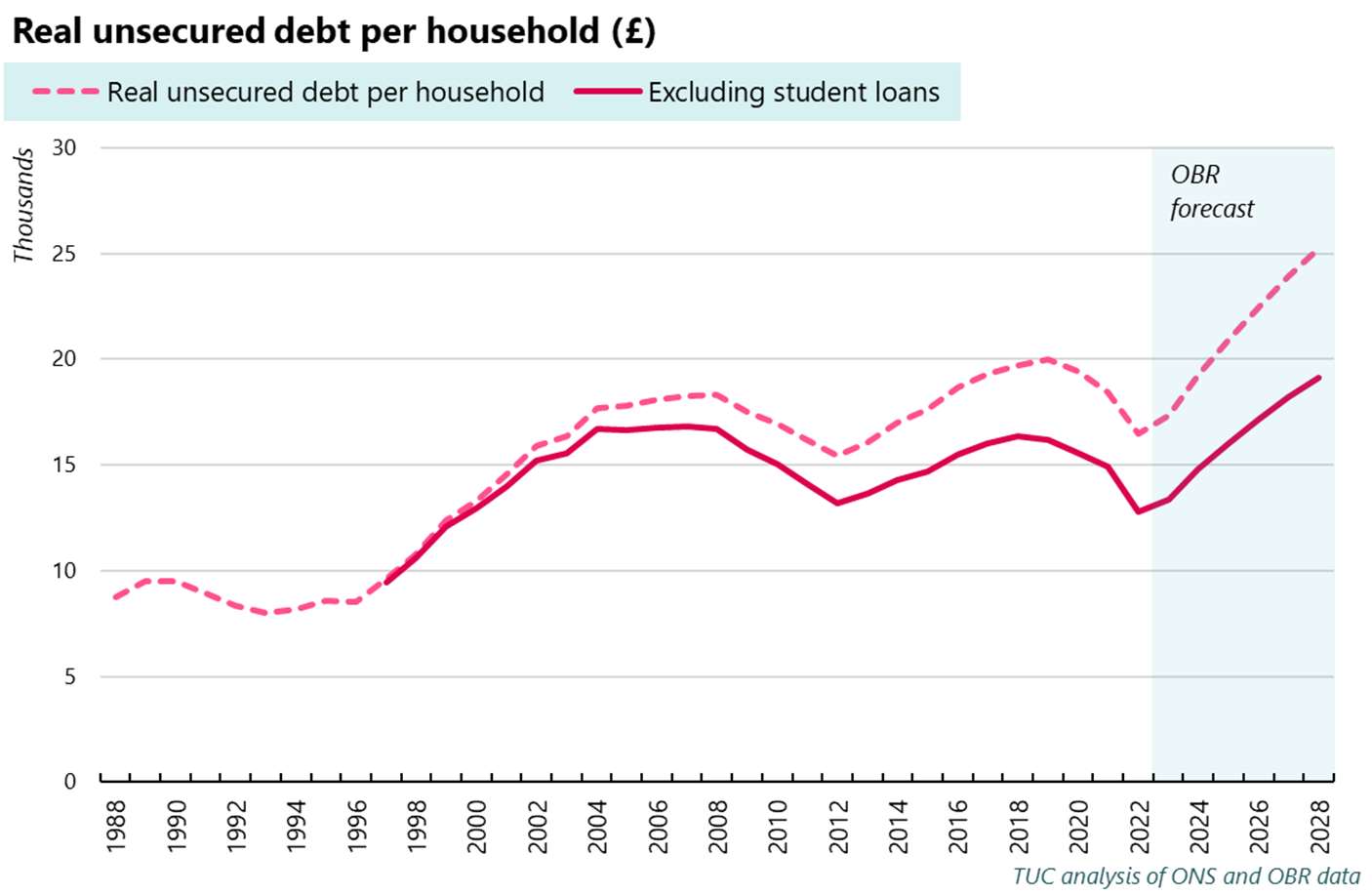

Household debt figures also show the extent to which household finances are in crisis. TUC analysis released in December 2023, based on the OBR’s November forecasts, shows that unsecured debt per household is set to rise by £1,430 (11%) in 2024, and will hit a new record high of £17,180 by 2026. It is then set to rise even further, hitting £19,120 by 2028.

Of course, pay is not the only factor impacting living standards and household debts. As well as overseeing a two-decade long real pay crisis, the government has consistently made real cuts to social security, alongside making the benefits system crueller and harsher. Cuts in social security since 2010 have left millions in poverty. The current levels of benefits are simply not enough to live on, and the rising cost of living is making it even harder to survive on them. The standard benefit payment for over 25s without housing costs is £85 a week.

Jobs are also under threat. Unemployment is up 220,000 on a year ago. Real time data on employees showed, for the private sector, jobs peaking in April 2023 and since then falling by 100,000. Vacancies have declined consistently for 18 months. While employment in the public sector (or rather, sectors traditionally dominated by the public sector) has seen some limited recent growth, as a share of the workforce, public sector jobs are greatly below the position after the global financial crisis.

Government failures have also allowed the unchecked growth of insecure work. TUC analysis of official figures shows that by the end of 2022 there were around 3.9 million people in insecure employment, with Black and minority ethnic (BME) workers disproportionately affected by the growth of insecure work. Since 2011, the proportion of the working population in insecure work grew from 10.7 per cent to 11.8 per cent.

BME workers have borne the brunt of this increase. In the last 11 years the proportion of BME workers in insecure employment has risen from 12.2 per cent to 17.8 per cent. 2 Facing both low pay and a lack of certainty over hours and patterns of employment, workers and households in this position are at the sharpest end of the living standards crisis.

A stagnant economy

With household incomes in reverse, spending has been restricted and the downward pressure on the economy has been intensified. As the chart below shows, since 2019 Q4 UK economic growth of 1.4 per cent is the 6th weakest growth of all OECD countries (with average growth of 6.5 per cent). As the figures on the chart for contributions show, the overall UK position is driven by falling household spending, exacerbated by a steep decline in exports and still weak investment expenditure. Since 2019Q4:

- household spending fell 1.4 per cent, the third worse performance in the OECD (average rise 6.1 per cent); and

- exports fell 4.7 per cent, the second worse performance in the OECD (average rise 9.7 per cent). 3

The barriers imposed on trade between the UK and EU following the poor terms on which the UK left the EU has caused a significant decline in UK exports to the EU;4 while the additional paperwork exporters are required to fill out now has created a significant burden on businesses. Both these factors threaten good jobs and pay. NIESR research indicates that impact of the government’s Brexit deal has been a 4% drop in productivity in the UK and a likely 6% reduction in GDP by 2035. 5

UK investment has been consistently poor. While investment growth has been less bad since 2019 (growing 5.5 per cent, ranking 18 in the OECD), UK investment as a share of GDP was still only 18 per cent against an OECD average of 23 per cent. As the IPPR have recently pointed out “For the past two decades the UK has consistently ranked amongst the worst performers in the OECD for business investment”.6

- 2 https://www.tuc.org.uk/research-analysis/reports/insecure-work-2023

- 3 The UK export deterioration is exaggerated by a particularly strong 2019Q4, but the overall position is still down on the basis of a rolling four quarter average.

- 4 https://cepr.org/voxeu/columns/impact-brexit-uk-economy-reviewing-evide…

- 5 https://www.niesr.ac.uk/publications/revisiting-effect-brexit?type=global-economic-outlook- topical-feature

- 6 Cutting corporation tax is not a magic bullet for increasing investment | IPPR

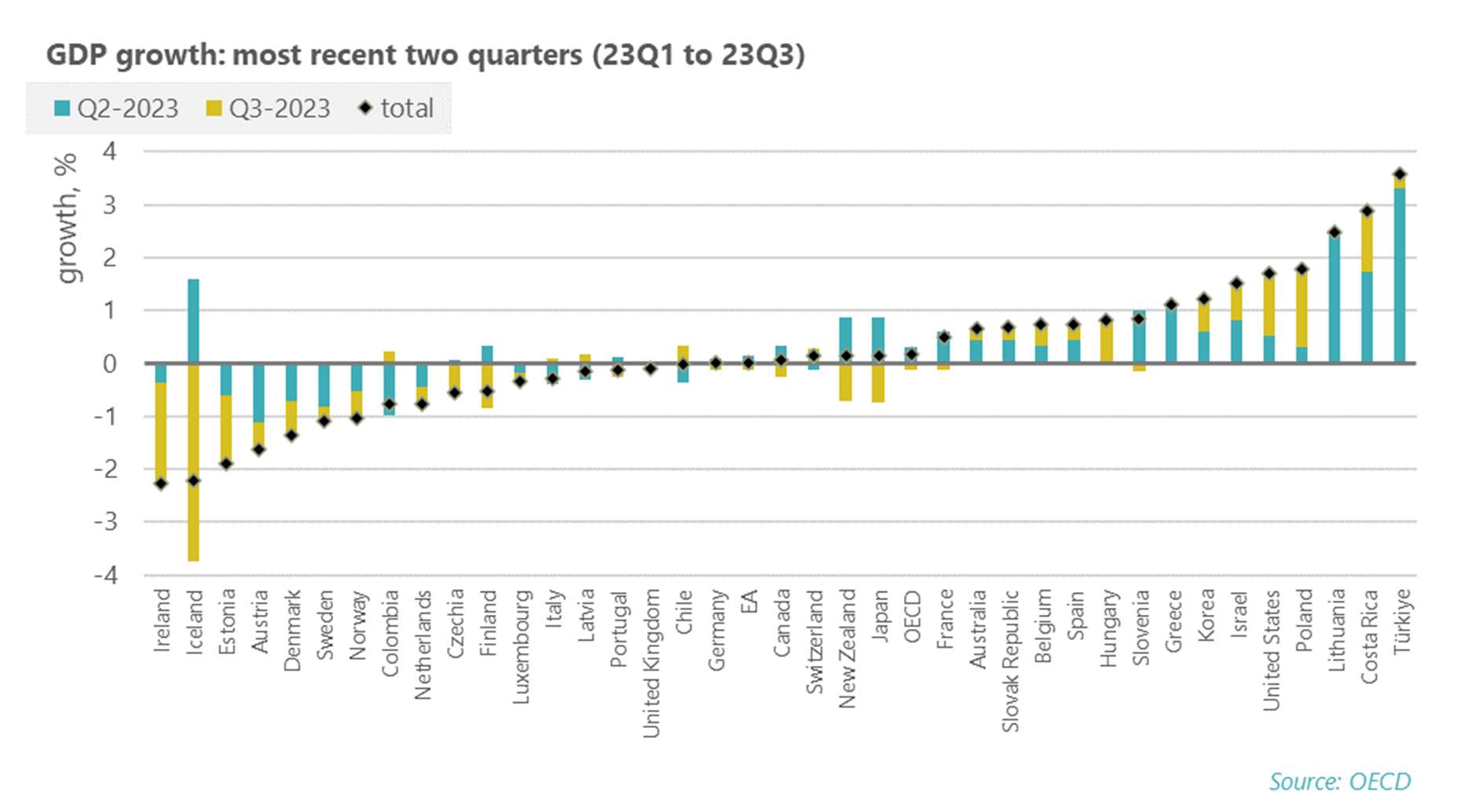

Even in the two months since the Autumn Statement the UK economy has looked a little more vulnerable. Over the second and third quarters of 2023 taken together, GDP is now estimated to have fallen by 0.1 per cent against the OBR forecast for a marginal rise of 0.2 per cent.

Vulnerabilities are also evident across many advanced economies. The chart below shows quarterly GDP growth for 2023 Q2 and Q3. The UK is one of 17 countries with negative growth over the two quarters taken together – and in fact is second worse of the G7 economies (Italy is worst) and worse than the European aggregate. Eight countries have both quarters negative, and so are in technical recession.

Economic policy failure

Instead of securing the recovery, the government has delivered stagnation. Household incomes are falling, investment outcomes are poor, and, instead of improving our failing public services, government plans imply substantial future cuts (of around £20bn).

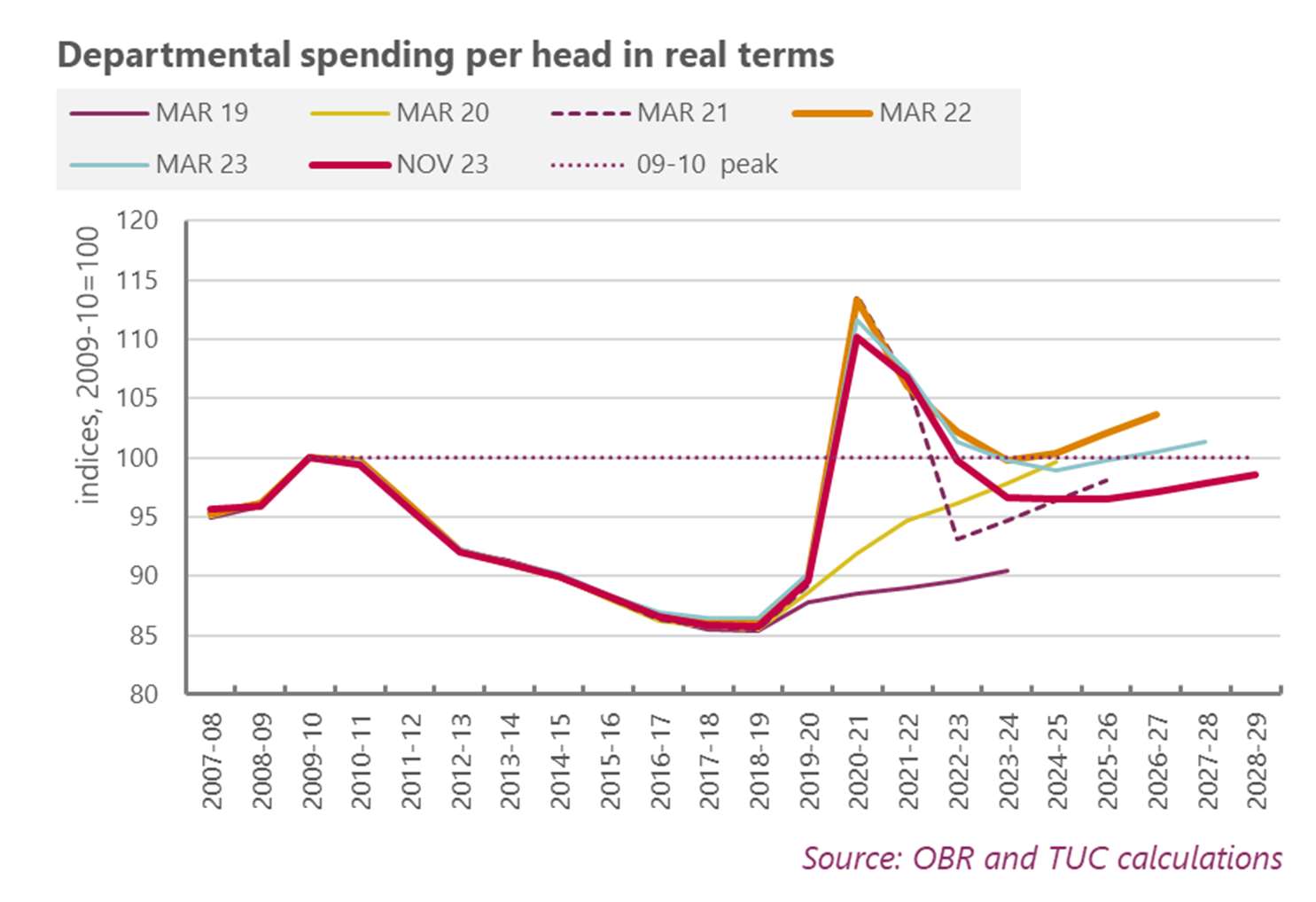

This means both departmental spending and public investment are facing increasingly serious retrenchment. As the chart below shows, two years ago real departmental spending per head was expected to resume the pre-pandemic path, with the orange path (Mar 22) picking up from yellow (Mar 20). But over the years since this path has been progressively undermined. The latest forecast (red line) shows substantial spending cuts (beyond those previously anticipated) within the current year (2023-24), with public spending then flatlining into 2024-25 and 2025-26.

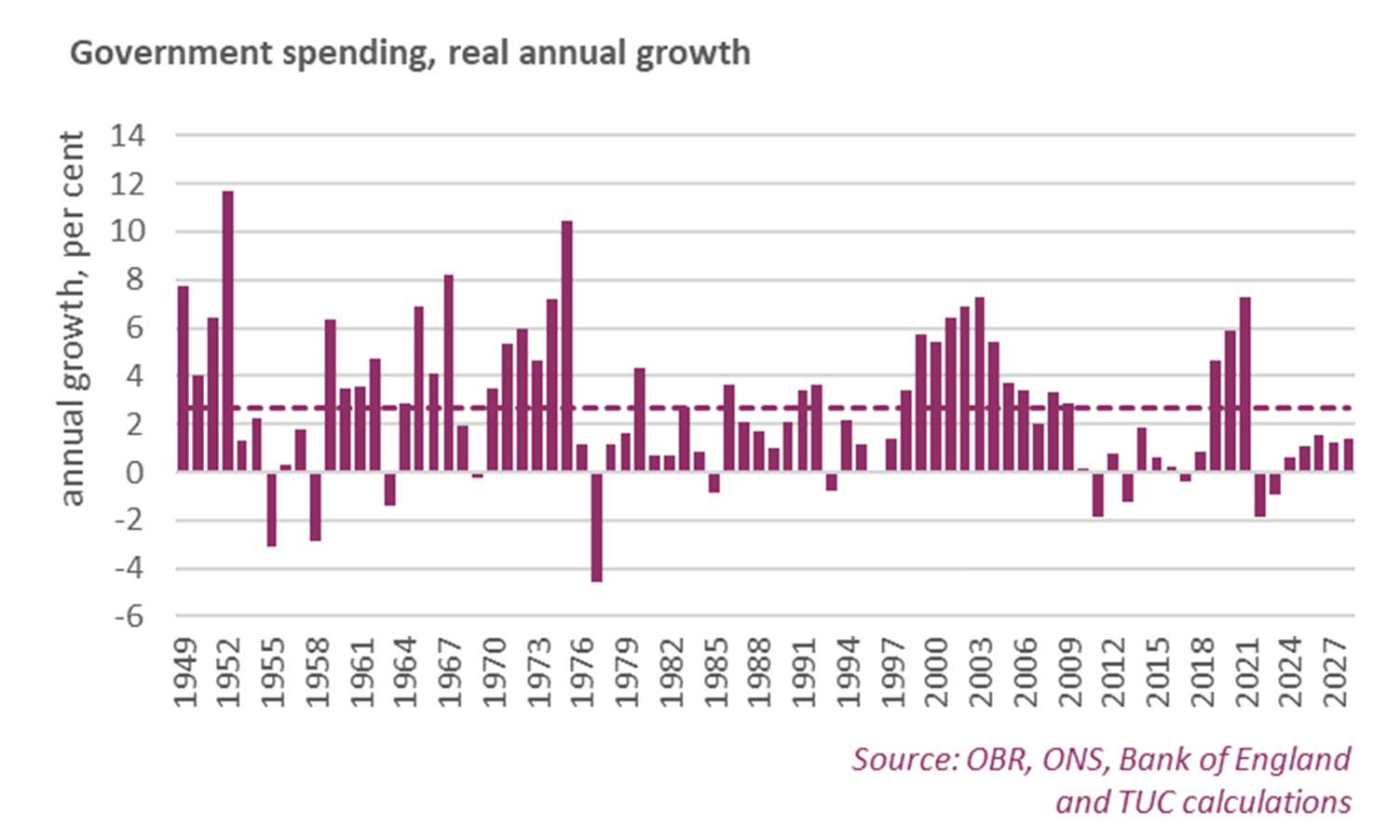

Using a national accounts measure,7 after two years of cuts, government spending is forecast to grow only by an average of 1.2 per cent a year (from 2024 to 2028), less than half the long run average of 2.7 per cent.

- 7 General government final consumption expenditure adjusted for price with the GDP deflator.

So following years of retrenchment, public service investment remains depressed. The TUC have warned for years that the intense financial pressure on public services is unsustainable, and now our services are in crisis. A decisive change is essential.

In ring-fenced departments such as the NHS, we have record wait times for hospital treatment and cancer care, and target ambulance response times are routinely exceeded, putting patients’ lives at risk. For non-ring-fenced departments such as local

7 General government final consumption expenditure adjusted for price with the GDP deflator.

government, chronic underfunding means councils face bankruptcy as they struggle to provide essential statutory services such as child and adult social care and temporary accommodation and homelessness support. Research by UNISON reveals councils face a collective funding shortfall of £3.65bn for the coming financial year (2024/25), rising to £6.99bn the year after. 8

The Institute for Government 9 has shown how far public service performance has fallen across most key areas of provision, considering performance since before the pandemic in areas including prisons, general practice, hospitals and social care. They report that in 2022/23, just over half of those attending A&E were admitted, transferred or discharged within four hours (56.7%), compared to three quarters in 2019/20 (75.4%).

They show rough sleeping is on the rise, the crown court backlog is at a record high and that among children who are at significant risk of harm, the proportion whose child protection plans are reviewed within the required timescales has fallen from 91.5% to 89.3%. More than one in six primary school pupils (17.2%) and more than one in four secondary school pupils (28.3%) are estimated to have been persistently absent in 2022-23.

Acute staffing shortages, fuelled by a toxic mix of real terms pay cuts, excessive and unmanageable workloads and lack of flexible work, exacerbate these issues. Public sector workers are, on average, earning £177 less in real terms compared to 2010. Restoring public sector pay is vital to fixing the recruitment and retention crisis affecting public services.

Failures in public services in turn hold back growth. The impacts that the growing NHS waiting list for elective care are having for labour market participation have been widely reported. Productivity growth has been further restrained by massive disinvestment in skills. The government is presiding over the lowest levels of workplace-based skills participation since records began, despite strong evidence that return on investment in skills benefits employers, workers and the whole economy (for example valuations of the Union Learning Fund show a return of over £12 for every £1 invested).

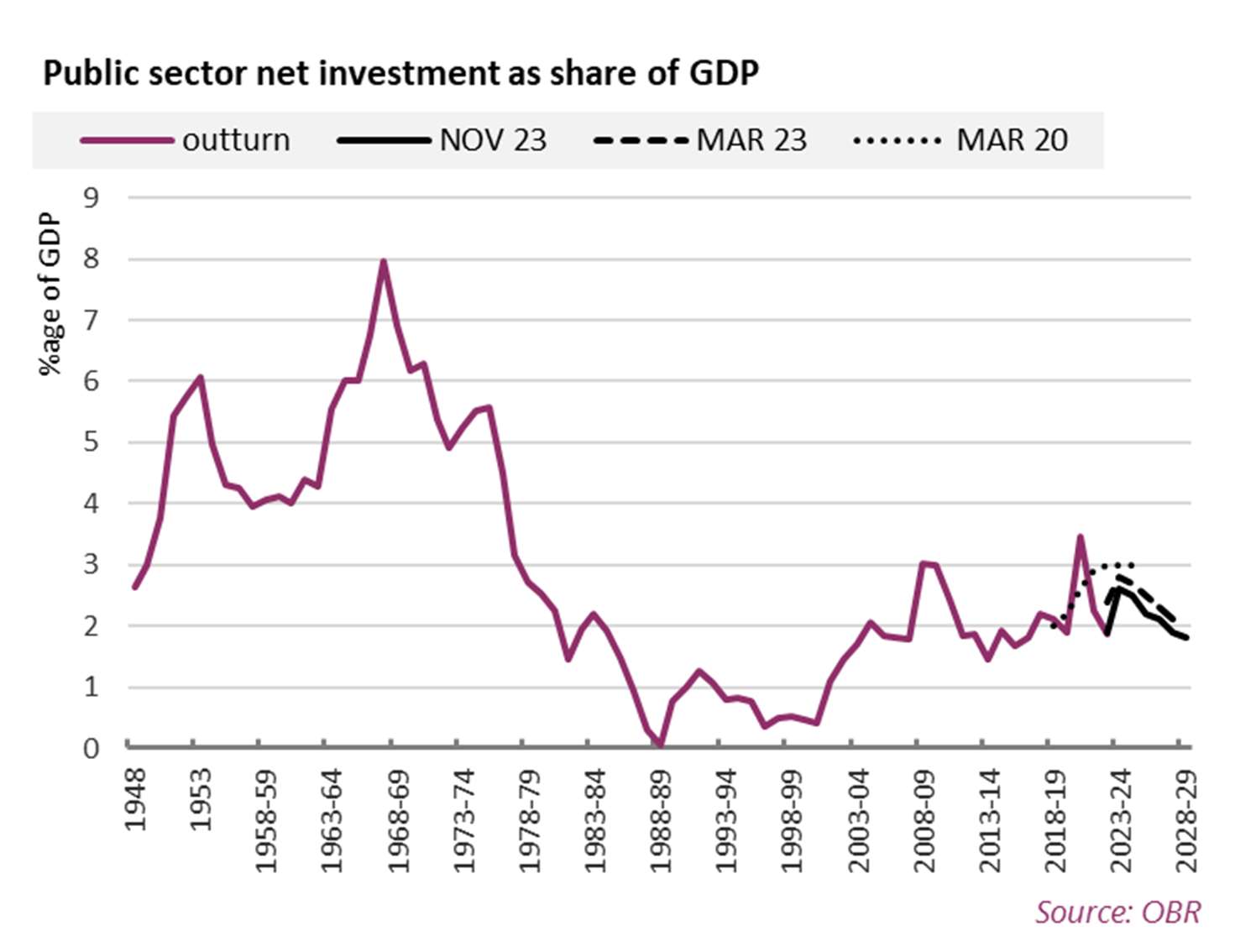

Likewise, while government has sought to support private investment with so-called full expensing, wider public capital investment also has been progressively undermined. As the chart below shows: ahead of the pandemic public sector net investment spending was projected at 3% of GDP; now it is projected at 2% of GDP. The government has already reduced investment by 1% of GDP, i.e. £25 billion. This level of investment puts us far behind our economic competitors and undermines our future growth potential.

Breaking out of the doom loop

The government is now in danger of repeating the mistakes of 2010, when huge public spending cuts decimated services and undermined economic growth. The result was the worst economic recovery for more than a century.10

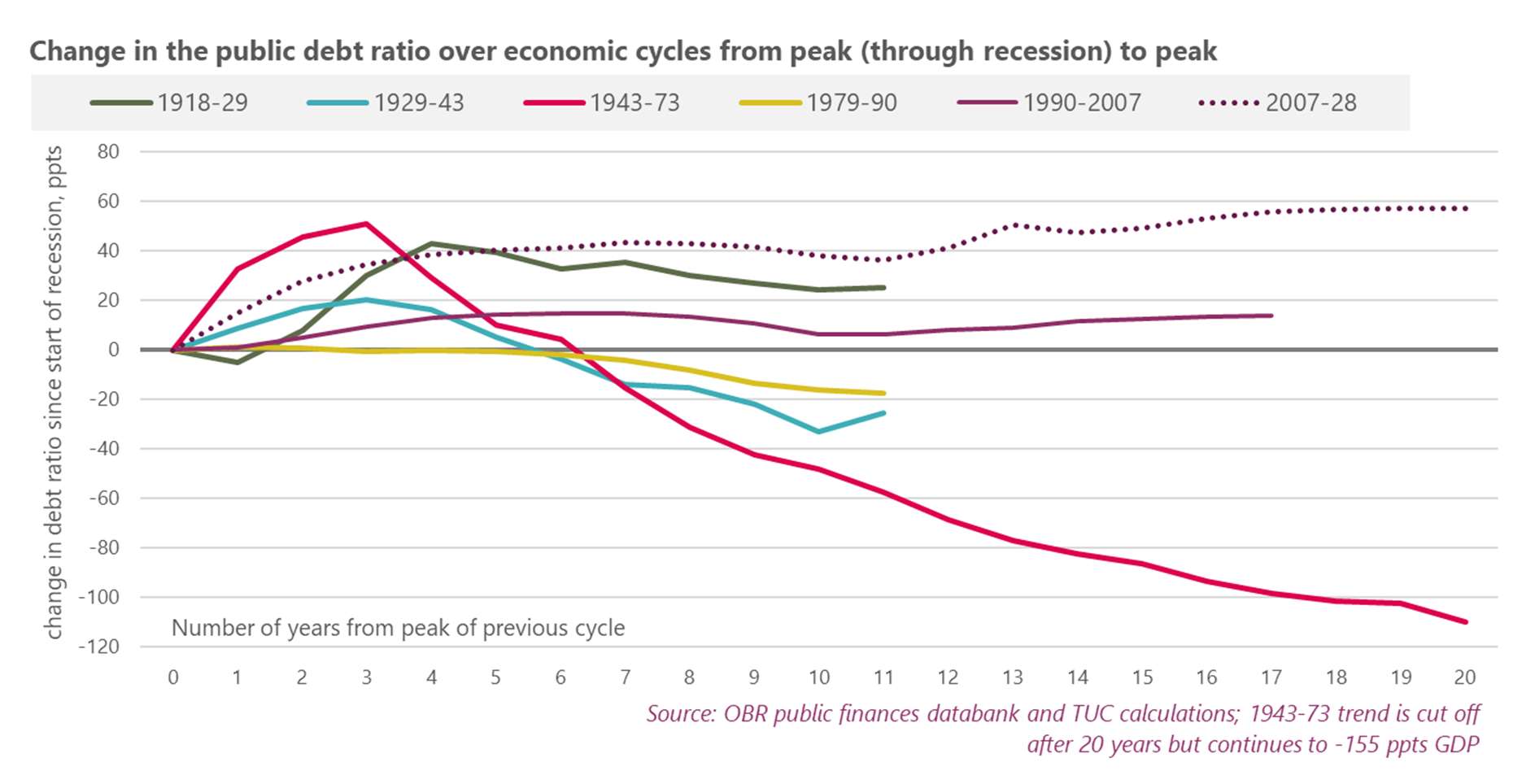

Such poor economic outcomes also mean the debt ratio has barely stopped rising (chart below), a disastrous outcome and unprecedented for at least a century. In cash terms public sector net debt has risen by an average of £120 billion a year (from 2010- 11 to 2023-24).11

- 10 https://www.tuc.org.uk/news/tuc-conservatives-are-presiding-over-worst-period-economic- growth-1920s

- 11 OBR public finances databank, December 2023 version: https://obr.uk/data/

After the experience of the last decade, the case for public capital and service investment to boost growth (and subsequently reduce public debt) should be self- explanatory. While monetary and fiscal restraint was highly contentious in the face of cost inflation, the steep inflation falls in recent months negate even any flawed justification for holding spending down.

The growing need to secure a fairer distribution of the rewards of growth has also been ignored. Pressing down on wages and spending undermines production, while supporting wealth results in excessive speculation and unwarranted gains concentrated at the very top. These inequalities have real consequences: a weaker economy, worse quality of work and dangerously unstable finance.12 The Biden administration understands that for too long the US economy has served wealth and not work, and as a result the Democrats have focused action on “levelling the playing field “.13 It is time for the UK to take the same approach.

Over the last 14 years successive governments have made the wrong choices. But they have not been helped by their approach to economic modelling. We remain concerned that government economic models fail to recognise the gains that public investment brings and downplay the importance that workers’ spending has for growth. As incomes fall there is a very material hit to the economy; when the government further cuts back spending, the economy is hit again. Our analysis has show this ‘doom loop’ might have needlessly written off £400 billion from the UK economy (for 2023). Even the IMF has admitted "On average, fiscal consolidations do not reduce [public] debt-to- GDP ratios". 14

We are not alone in having reservations about the Treasury and Bank of England models. The IPPR have called for a “more forward-looking approach” from the OBR. 15 And the Bank of England have tasked former Chairman of the Federal Reserve Ben Bernanke with a "review into the Bank’s forecasting and related processes during times of significant uncertainty”.16 The Economic Affairs Committee of the House of Lords warned of groupthink around economic policy more generally, 17 and have now opened an inquiry into “whether the Government’s fiscal rule … is fit for purpose”.18

As the GDP figures show, the danger is that our economy remains on a path of stagnation or at worst tips into recession. Instead, the imperative is for policy action to protect against recession and then set a course from stagnation to growth. So we repeat our largely ignored calls for immediate action that we set out at the Autumn Statement. These would be the first steps towards a stronger, fairer economy with growth outcomes improving rather than stagnating.

The government should:

- Halt plans for the roll-out of Minimum Service Levels to more services, repeal the regulations it has already imposed and focus on fostering positive relationships between workers and employers.

- Begin a process of costing and planning public investment for a rapid and just climate transition and a richer Britain (as outlined in the recent TUC report ‘Investing in Our Future’).19

- Recognise the importance of intermediate labour market programmes and introduce a paid jobs guarantee. This should provide six-months of paid work (at least the national minimum wage) with accredited training to young unemployed people who have been out of work for three or more months and to older workers who are facing long-term unemployment. Instead of castigating claimants for not looking for work, the government should act to ensure those who are seeking work can gain real world paid experience that will give them the best chance of sustained employment.

- Following the success of the furlough scheme, introduce a permanent short- time working scheme to protect workers and businesses at times of economic change.21

- Set a path to significant and permanent improvements in the levels of social security. They should also immediately stop policies that are needlessly taking money out of families’ pockets, including harsh benefit deductions, the arbitrary benefit cap and the five-week wait in universal Credit.

- Introduce further cost of living support, rather than halting payments in March 2024. The energy price cap has increased again to £1,928 raising the average bill by a further £94, 22 and over only two years food prices are up by more than 25 per cent.

- Take a new approach to supporting people who are economically inactive due to their health. It is time for Ministers to recognise that the best way to bring down the numbers of people who are out of work and not actively seeking it is urgently to improve access to decent healthcare, proper employment support and good quality, secure employment.

- Put in place the first steps towards an overhaul of the UK’s skill system. This would include introducing much more flexibility into the apprentice levy, providing resources for low earners with low qualifications to pay for training and introducing a right to retrain for workers who are at risk of losing their job due to industrial dislocation or technological change.

- Row back from their intention to remove funding for level 2 courses, which provide a vital means for low skilled and low paid workers to progress towards further and higher-level skills. At the same time, Ministers should reinstate funding for the Union Learning Fund in England.

- Use the forthcoming review of the UK-EU Trade and Cooperation Agreement in 2026 to reduce barriers to trade and services through closer alignment with EU rules, as well as ensuring the UK and EU maintain common high standards of workers’ rights.

- 12 https://www.tuc.org.uk/research-analysis/reports/doom-loop-economy-work-not-wealth

- 13 https://www.ft.com/content/33a86191-3a75-452b-b3ce-d3d35ae90e06

- 14 https://www.imf.org/en/Publications/WEO/Issues/2023/04/11/world-economic-outlook-april- 2023

- 15 https://www.theguardian.com/commentisfree/2024/jan/08/britain-investment-spending- green-projects-keir-starmer

- 16 https://www.bankofengland.co.uk/news/2023/july/ben-bernanke-to-lead-review-into- forecasting-at-bank-of-england

- 17 https://committees.parliament.uk/work/7356/bank-of-england-how-is-indep…- working/publications/

- 18 https://committees.parliament.uk/call-for-evidence/3299

- 19 https://www.tuc.org.uk/research-analysis/reports/investing-our-future[ /fn]

- Implement a long-term, sustainable and comprehensive investment plan to repair and rebuild our public services, with a focus on early intervention and preventative support. Increased spending for ring-fenced and non-ring-fenced departments is essential.

- Ensure the necessary financial provision for decent pay increases in the public sector for 2024-25 and beyond to ensure we can recruit and retain the staff we desperately need. Government should work with employers and unions to develop and implement fully-funded workforce strategies for every part of the public sector, bringing down excessive workloads and clearing backlogs.

- Beyond April 2024, heed the growing international and national evidence that higher minimum wages can be achieved without rising unemployment while bringing economic gains from lower paid workers’ increased spending power. The Low Pay Commission should be charged with achieving a minimum wage of 75 per cent of median hourly pay as soon as possible.

https://www.tuc.org.uk/blogs/we-need-15-minimum-wage - 21 https://www.tuc.org.uk/blogs/beyond-furlough-why-uk-needs-permanent-short-time-work- scheme

- 22 https://www.tuc.org.uk/news/energy-price-cap-rise-will-hammer-households-even-harder- 2024

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox