How the shareholder-first business model is contributing to inequality

We studied the total net income, dividends and share buybacks for the current FTSE 100 companies index over the last five years.

From 2014 to 2018 we found that:

- The FTSE 100 companies generated net profits of £551 billion and returned £442 billion of this to shareholders. This means that overall the FTSE 100 paid shareholders an average of £1.7bn a week over the period.

- Across the FTSE 100 as a whole, returns to shareholders increased by 56% (despite net incomes falling by 3% over the period). This resulted from a 45% increase in dividends, while share buybacks more than doubled. If pay across the UK economy had kept pace with shareholder returns, the average worker would now be over £9,500 better off.

- While FTSE 100 returns to shareholders rose by 56%, the median wage for UK workers increased by just 8.8% (both nominal).

- Payments to shareholders primarily benefit a wealthy minority. UK taxpayers earning over £150,000 (barely 1% of all taxpayers) captured around 22% of all direct income from UK dividends.Dividend income accruing via pension savings also primarily benefits those at the top – 46% of pension wealth is owned by the wealthiest 10% of households.

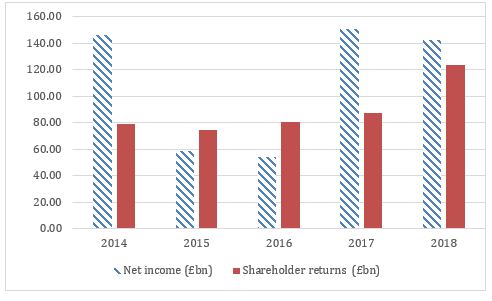

- In 27% of cases, returns to shareholders were higher than the company’s net profit, including 7% of cases where dividends and/or buybacks were paid despite the company making a loss. In 2015 and 2016, total returns to shareholders came to more than total net profits for the FTSE 100 as a whole.

- The theory is that when profits fall, returns to shareholders should fall too. Our research found that in practice this is not the case and that profits varied significantly more than returns. Total profits ranged from £53 billion in 2015 to £150 billion in 2017, a variation of £97 billion, with a fall between 2014 and 2015 and a sharp rise in 2017. Returns to shareholders had less than half as much variation, ranging from £74bn in 2015 to £122 billion in 2018. This contradicts the idea that shareholders are exposed to the greatest risk of all business stakeholders, as it suggests that they can expect consistent returns, regardless of profitability.

Examining sectors, we found that:

- In 2018, the two largest energy companies spent at least 11 times more on their shareholders than they invested in low carbon activity.

- In 2018, the 4 largest food and drinks companies paid shareholders almost £14bn – more than they made in net profit (£12.7bn). To put that into perspective, just a tenth of this shareholder pay-out is enough to raise the wages of 1.9 million agriculture workers around the world to a living wage. These companies source raw material from some of the poorest people in the world – none take sufficient steps to ensure that a living wage is paid to workers in their supply chains.

- The UK’s largest house builders paid their shareholders £6bn between 2014-2018 - enough to buy 25,000 homes. It would take the workers who build the houses 92 years to pay for the average UK house and 19 years to save for the deposit.

Download full report (pdf)

New analysis of dividends and share buybacks paid by the FTSE 100 over the last five years reveals the extent to which companies protect and increase payments to shareholders, even when company finances are struggling. Putting shareholders first means less money for workers and other stakeholders, hampering efforts to tackle in-work poverty and climate change.

From 2014 to 2018, returns to shareholders across the FTSE 100 rose by 56%, growing nearly seven times faster than the median wage for UK workers, which increased by just 8.8% (both nominal).

Over the same period, the UK’s largest listed companies generated £551 billion in profit (net income attributable to shareholders), and paid out £442 billion in dividends and buybacks. Even a small proportion of this money could mean better wages and working conditions for their staff and workers in their supply chains.

The UK’s largest companies could play an important role in reducing poverty and inequality, but the current business model is designed to maximise profit for shareholders. Employing 6.3 million people worldwide , with many more in their supply chains, their actions have a major impact on global working conditions and living standards.

1 in 10 working households in the UK live in poverty, comprising 8 million people in total, while at the same time the richest 34 people own the same wealth as the poorest 40% of the UK combined . The TUC and The High Pay Centre are calling on our political leaders to take immediate steps to fix the broken economic model that puts shareholders first.

About the report

The objective of this work is to contribute to the debate on the role of business in society and corporate governance reform. Our joint ambition is to advocate to all UK political parties to adopt policy reforms that tackle in-work poverty and promote sustainable development in the UK and internationally.

This paper builds on, TUC and High Pay Centre’s long-standing policy and advocacy work on corporate governance. Over the last two years this has included submitting evidence to the Government on corporate governance reforms and meeting with Department for Business, Energy and Industrial Strategy civil servants and the Financial Reporting Council. Both organisations have independently published research and policy papers on corporate governance issues.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox