Ending the Pay Crisis

The spring statement comes in the context of the Russian invasion of Ukraine, posing a terrible toll on the Ukrainian people. The TUC has called on the government to support all efforts towards a diplomatic resolution of the conflict, and written to the Chancellor to ensure that sanctions are backed by effective enforcement, and that we provide the funding to secure support both for humanitarian aid and for refugees to come to the UK. The conflict is also likely to lead to significant price rises, leading to further pressures on working people in the UK.

Summary

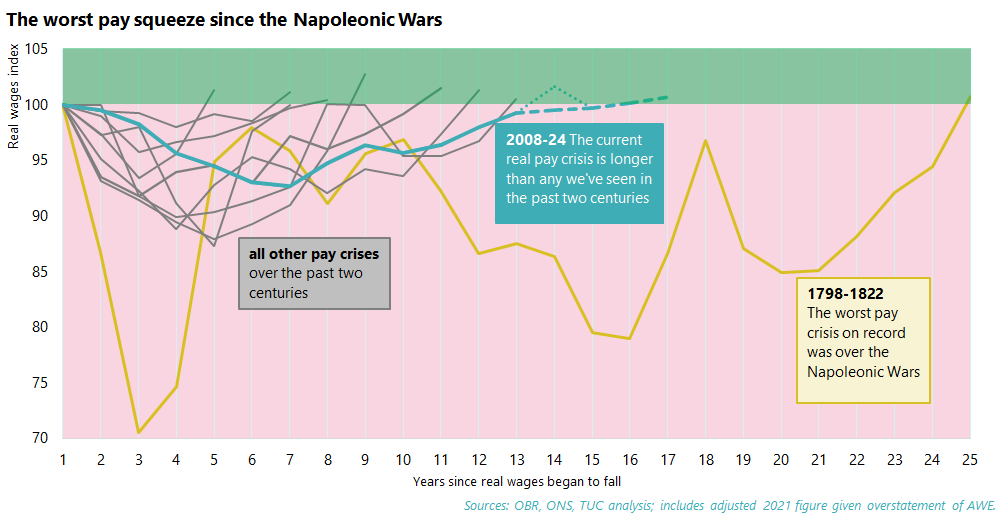

We are now in the fourteenth year of a pay crisis, intensified over 2021 and 2022 by sharply rising inflation.

While the furlough scheme has successfully protected the economy, growth is fragile, employment still well down and many industries far from recovered.

And the debate around inflation, pay and monetary policy has thrown deep rooted injustices into sharp relief. Governor Bailey’s ill-judged call for wage restraint was met with astonishment and anger by working people and trade unions. While subsequently slightly refined, those remarks were a stark reminder that workers are now being asked to bear the brunt of rising global prices, having already borne the brunt of a decade of austerity, the hardship of the pandemic, and the longest pay squeeze since the Napoleonic wars (as illustrated on the chart below).

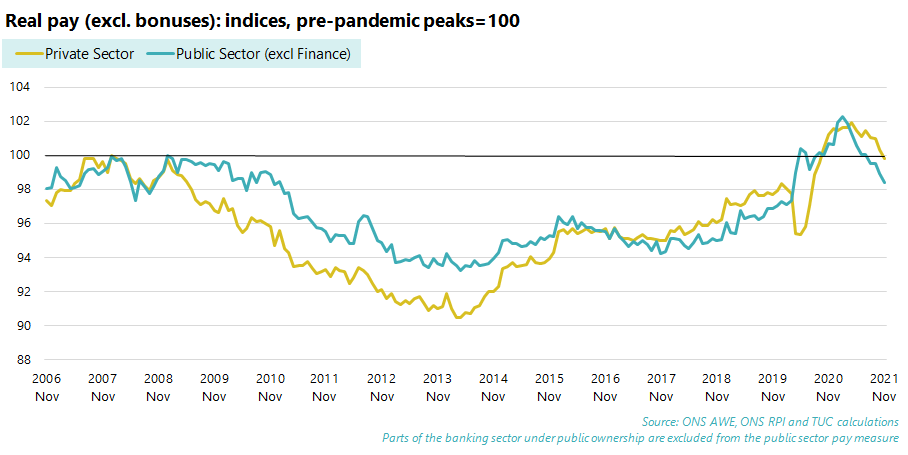

Public sector workers have suffered some of the worst pay cuts, following government imposed pay restraint throughout the 2010s. Looked at over the period since the financial crisis, real public sector pay is down 1.6 per cent and real private sector pay down (on the CPI figure of inflation – using RPI both figures are down around 10 per cent), and the latest real pay figures show pay falling 1.6% in health, 4.6% in education and 4.2% in public administration.

A different approach is possible. Government must recognise that boosting workers’ pay will help the economy, without leading to inflationary spirals.

In this submission to the spring statement process we first set out our analysis of current economic conditions, and their impact on working people. We then outline the action government must take to:

Deliver an immediate boost to pay:

Government should:

- Boost the minimum wage immediately to at least £10 an hour, for all workers irrespective of age.

- Fund decent pay rises so that all public service workers get a pay rise that at least matches the cost of living and begins to restore earnings lost over the last decade, through fully independent pay review bodies or collective bargaining.

- Ensure all outsourced workers are paid at least the real Living Wage and receive pay parity with directly-employed staff doing the same job.

- Recognise that collective bargaining is the most sustainable way to boost pay, and use the long-promised employment bill to give trade unions new powers to negotiate fair pay agreements across sectors.

- Take measures to support equal pay including strengthening gender pay gap reporting requirements, and introducing ethnicity and disability pay gap reporting.

- Ensure that fiscal policy is supporting growth and pay.

Fund efforts towards a peaceful solution to the conflict in Ukraine

- We welcome the proposed register of wealthy overseas owners of UK property through the Economic Crime (Transparency and Enforcement) Bill, but this needs to be backed up by sufficient powers and funding for Companies House to enforce.

- Government must fund additional humanitarian assistance for displaced people, and welcome refugees to the UK.

- Government should consider implementing a new 100 per cent tax on additional profits made by UK based companies from their shareholdings in Russian state backed enterprises that have profited from the gas price crisis.

Take additional measures to support families in the UK with rising energy prices

- Government must improve its support for families facing rising energy costs, by providing support for households in the form of a grant, not a loan (replacing the energy price rebate), an increase in the warm homes discount, and rapid implementation of an accelerated and expanded domestic home retrofit programme, delivered by local councils who are best placed to deliver fast.

- Provide funding for these measures by the implementation of a windfall tax on North Sea oil and gas companies’ profits

- Government must also fix the holes in the safety net which have made families less resilient to rising costs. This should start with an immediate boost to the value of Universal Credit and other related benefits to the value of 80 per cent of the real living wage.

- Families also face a rising cost of being sick, as the final parts of covid-related support are removed. Now is the time to fix sick pay by removing the lower earnings limit, paying sick pay from day one, and raising the value of sick pay to the level of the real living wage.

- Childcare costs are also posing a rising burden on families. Government must provide an urgent funding boost to the childcare sector.

- Measures must also be taken to boost the value of both public and private pensions, including restoring the triple lock for 2022/23 and extending auto-enrolment to include more low-paid workers.

Deliver the long-term changes needed for a high-wage, high skill, high productivity economy

The Chancellor should also set out how the government will deliver the changes needed to achieve the Prime Minister’s ambition of a high wage, high skill, high productivity economy. These include:

- New funding for the skills system to deliver access to fully-funded learning and skills entitlements and new workplace training rights throughout the life course.

- Reforms to corporate governance to embed long-termism and sustainable business models in corporate decision making, including reform of directors’ duties and including elected worker directors on company boards.

- Delivering an industrial strategy that delivers good jobs as we transition to net zero, including funding for industrial decarbonisation, and new commitments to deliver supply chain jobs in the UK.

- An expansion in the public sector workforce, delivering the decent public services we need to level up.

There is still the chance to fulfil the promise to build back better after covid. The Chancellor must commit to that at the spring statement.

The economic context

Pay and inflation

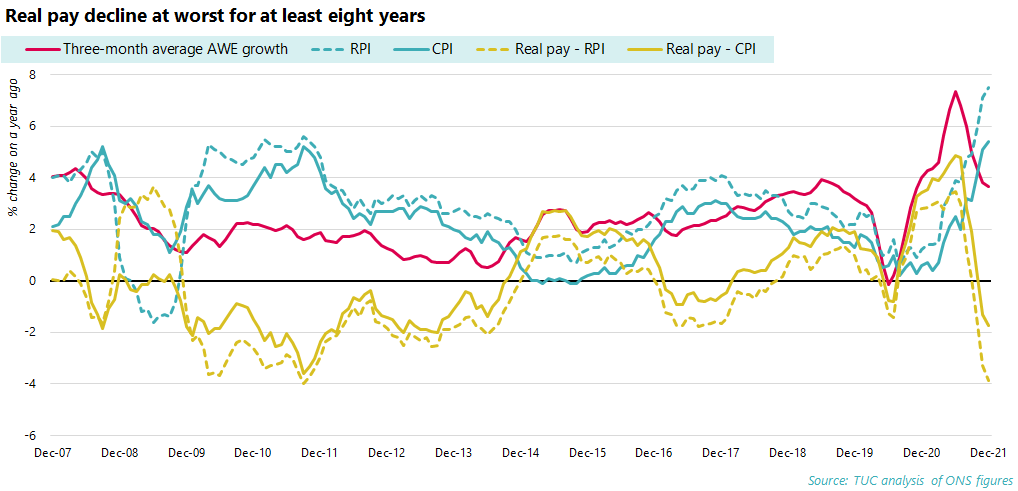

As set out above, workers are in the longest pay squeeze in 200 years. This real pay crisis is two sided. Alongside inflation at a 30-year high, nominal wage growth has been slowing. Inflation in January 2022 was 5.5 per cent on the CPI measure, and 7.8 per cent on the RPI; comparing with the same month a year ago, regular pay grew by 3.7 per cent. The sum of the parts is real pay growth falling by 1.8 per cent on the year on CPI, the worse decline for eight years, and by 3.8 per cent on RPI, the worse decline for eleven years. The longest pay squeeze since Napoleonic times is intensifying, and barely any gains are expected over the next three years.

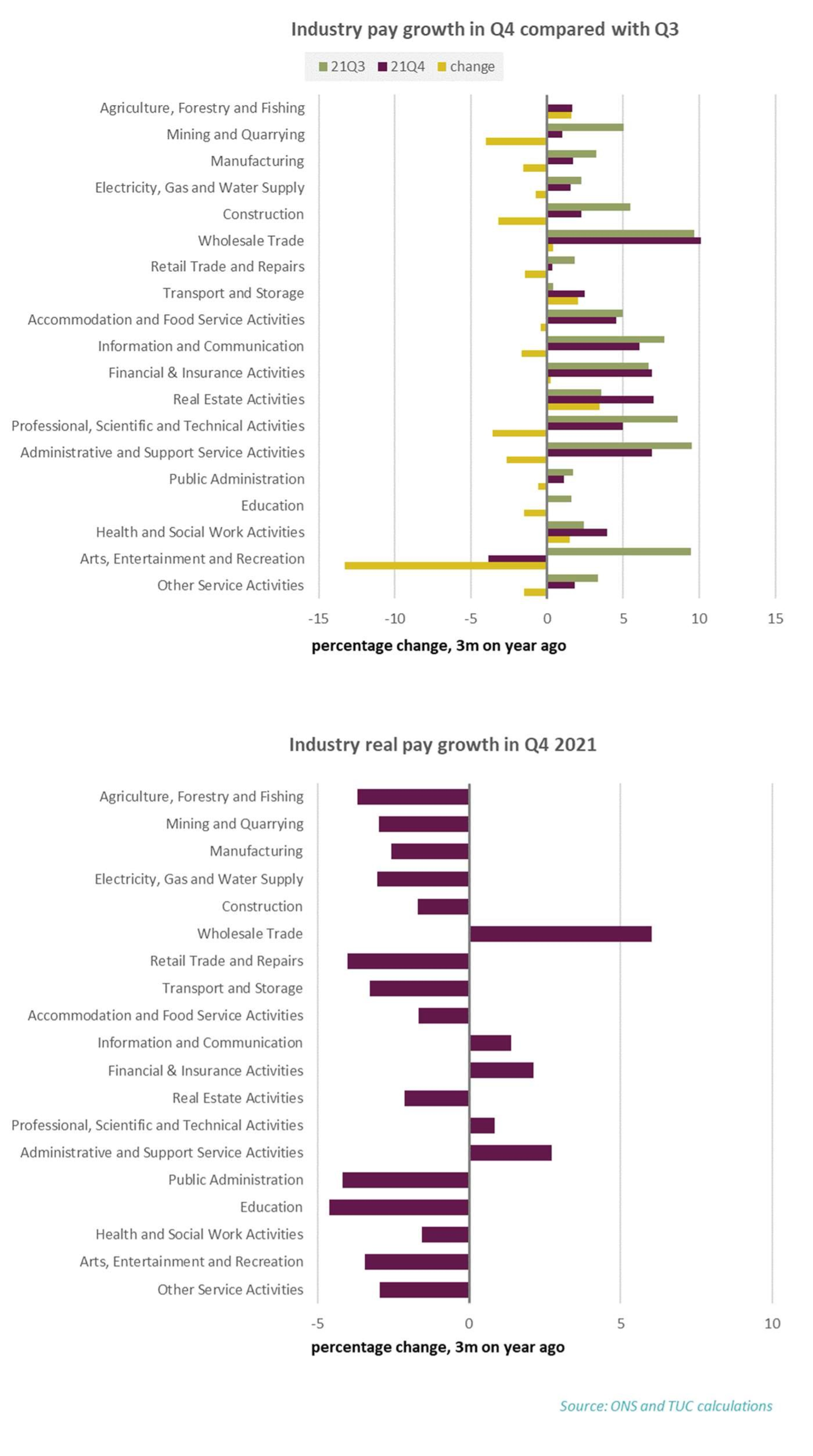

The marginal increase in the Average Weekly Earnings on the chart above was down to an increase to 7.0 per cent from 6.2 per cent for finance and business (with also very large bonuses, excluded from these figures). While the distortions from the furlough scheme mean the great part of the recent slowdown in nominal pay growth is artificial, there is virtually no evidence of any acceleration in pay growth.1 At the industry level, between Q3 and Q4 pay growth is slowing in thirteen of nineteen industries and real pay is negative in 14 industries.2 Pay for the public sector industries is in the worst place, with real pay down 1.6 per cent in health, 4.6 per cent in education and 4.2 per cent in public administration (on CPI) following government imposed pay restraint.

- 1 ‘Let’s get real on pay’, Afzal Rahman, 25 Feb. 2022: https://www.tuc.org.uk/blogs/lets-get-real-about-pay

- 2 Jobs and recovery monitor, #10, ‘Wage squeeze continues’: https://www.tuc.org.uk/researchanalysis/reports/jobs-and-recovery-monit…;

These figures will get worse. In February the Bank of England expected inflation to peak in April at 7¼ per cent. The conflict in Ukraine is now likely to mean this peak will be higher and perhaps more sustained.

GDP

GDP may have recovered to around the pre-crisis level, but growth has been flagging over the second half of 2021, in part because of renewed pressures from the pandemic and the omicron variant. Comparisons with other countries are misleading, with the UK’s stronger growth this year a consequence of catching up with a the steeper decline last year. Over the two years of the pandemic the UK was fifth of the G7 economies, ahead of Japan and Italy.3

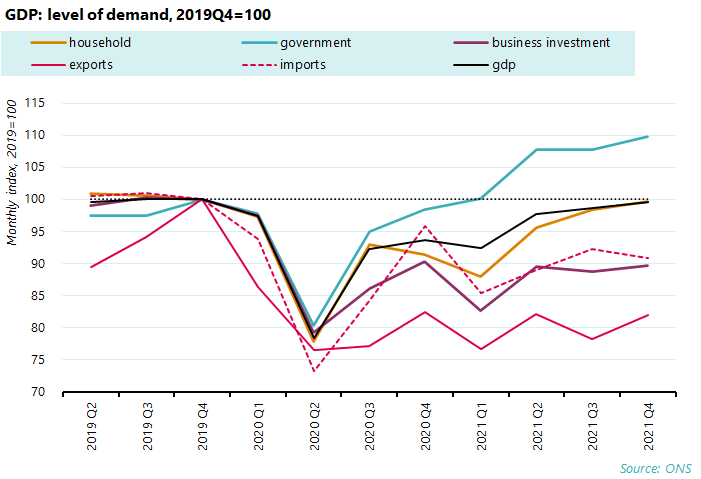

The key concern for the economy is uneven aggregate demand, with signs that consumer spending is slowing. Since coming back from the most severe phase of lockdown, the economy has been sustained by a combination of government spending and revived household spending. As the chart below shows, over the past year, exports (red), imports (dotted red) and investment (purple) have basically flatlined (in fact exports have barely recovered any lost ground since the peak of lockdown and Britain’s withdrawal from the EU). Comparing the year from 2021Q4 with 2020Q4: exports are down -0.6 per cent, imports down -5.3 per cent and business investment down -0.8 per cent. Supporting the economy were government expenditure, up 11.6 per cent (blue), and household demand, up 8.9 per cent (orange).

- 3 ‘Beyond the GDP headlines, alarms ring as households cut back’, TUC blog, 11 Feb. 2022: https://www.tuc.org.uk/blogs/beyond-gdp-headlines-alarms-ring-household…;

But the contribution from household spending is slowing. Up vigorously by 8.9 per cent into the second quarter, it slowed to 2.9 per cent in Q3 and then to 1.2 per cent in Q4. Some of this slowdown may be related to omicron at the end of the year, but on top of this comes the increased hit to real pay and so real incomes, and an intensifying loss of confidence – especially in the wake of the conflict in Ukraine.4 Monthly retail sales data for example has been falling steadily since a high in April 2021; in January 2022 sales were up only 1.7 per cent, regaining less than half the ground lost after the fall of 3.9 per cent in December – and overall stand 5.7 per cent below the level in April. As discussed below, this is how the Bank of England see events playing out over coming years: a big hit to real incomes will reduce spending, and economic growth will slow to a snail’s pace. GDP growth is expected to slow from 3¾ per cent this year to only 1¼ per cent in 2023 and 1 per cent in 2024. And worse of course is that the government is planning to cut its own support: the Bank reckon on support in the “near term”, but “fiscal policy gradually tightens over the forecast period”.5

Jobs

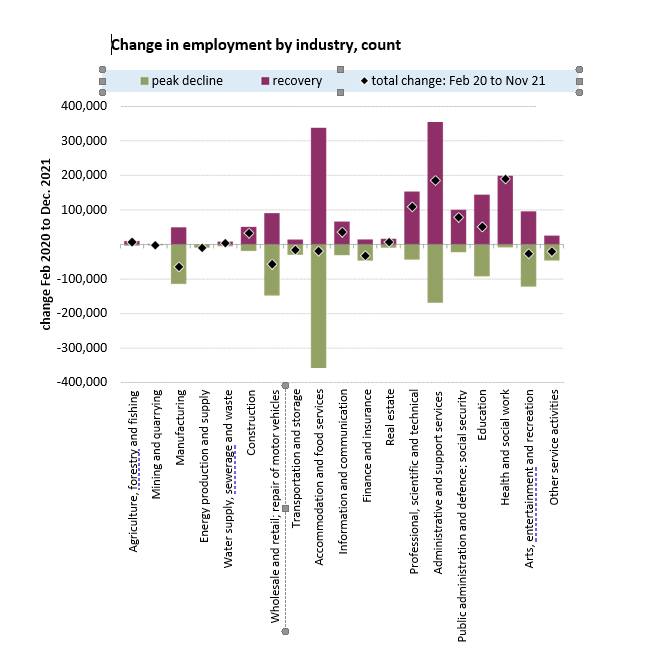

While the furlough scheme has worked effectively to protect jobs throughout the pandemic and measures of employees show jobs now above the pandemic position, the self-employed have been hit very hard. Employee jobs are up around 350,000 on before the pandemic, but self- employment is down 850,000. While there has been a net loss of 600,000 jobs, unemployment has not risen. Instead, inactivity has increased by 700,000 (and the working age population has risen by 100,000). 6

The big employment gains have been concentrated in industries closely related to the pandemic – most obviously health, but also business services, and public and private administration. In a number of other industries –notably, manufacturing, retail, finance and arts and entertainment – employee jobs are still down on the pre pandemic position.

- 4 UK consumer confidence plunges as surging living costs take toll, FT, 25 Feb. 2022: https://www.ft.com/content/8d4a29e6-4bef-4c52-92c4-ab588f6af51f

- 5 Monetary Policy Report, Bank of England, Feb. 2022: https://www.bankofengland.co.uk/-/media/boe/files/monetary-policy-repor… 6 The rise of 100,000 in the working age population matches the rise of 700,000 in inactivity and fall of 600,000 in activity.

- 6 TUC Jobs and recovery monitor #9 – disabled workers: https://www.tuc.org.uk/researchanalysis/reports/jobs-and-recovery-monit…

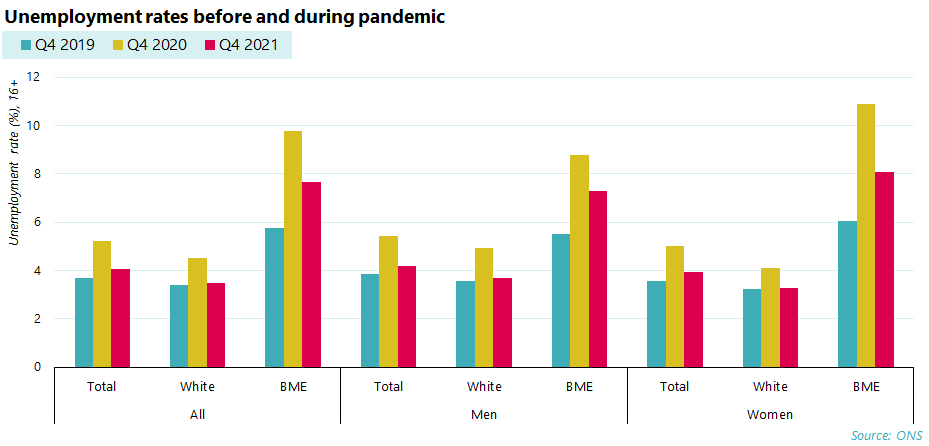

The pandemic has also exacerbated existing workplace inequalities. Black workers’ jobs were hit hardest during the pandemic. The unemployment rate for BME workers rose to

9.8 per cent in Q4 2020, compared to 4.5 per cent for white workers. The peak of the unemployment rate for white workers (4.5 per cent in Q3 and Q4 2020) was actually lower than the BME unemployment rate before the pandemic hit (5.8 per cent in Q4 2019). BME women were particularly hard hit, with the unemployment rate hitting 10.9 per cent in Q4 2020.

Across all workers, the unemployment rate has recovered to 4.0 per cent in Q4 2021. This headline figure, however, is masking racial inequalities. As the chart below shows, the unemployment rate for white workers is at 3.5 per cent, only 0.1 percentage points higher than it was pre-pandemic. The unemployment rate for BME workers, however, is

7.7 per cent, almost 2 percentage points higher than it was pre-pandemic.

The chart below also shows the unemployment rate for BME women now up to 8.1 per cent compared to 6.1 per cent before the pandemic. Likewise for BME men, unemployment is up to 7.3 per cent from 5.5 per cent. For white women, unemployment is now basically unchanged, at 3.3 per cent compared with 3.2 per cent before the pandemic; and the same is the case for white men, standing at 3.7 per cent compared with 3.6 per cent.

The gap between the unemployment rates for white and BME workers has therefore widened during the pandemic, from 2.4 ppts (69 per cent) in Q4 2019 to 4.2 ppt (120 per cent) in Q4 2021.

Disabled workers continue to face severe disadvantages relative to other workers. The disability employment gap is 28.7 percentage points, with the employment rate down to 52.2 in 2020/21 from 53.3 per cent in2019/20 before the pandemic. The fall was in line with the workforce as a whole, with the employment rate down over the same period to 80.9 per cent from 81.9 per cent.7

But the intersectionalities with other inequalities are increasingly serious. With an unemployment rate of 8.0 per cent in 2020/21, disabled workers are almost twice as likely to be unemployed than non-disabled workers (4.3 per cent). For disabled BME workers, the unemployment rate is 13.7 per cent, compared to 3.7 per cent for white non-disabled workers. The unemployment rate is highest among disabled BME men.

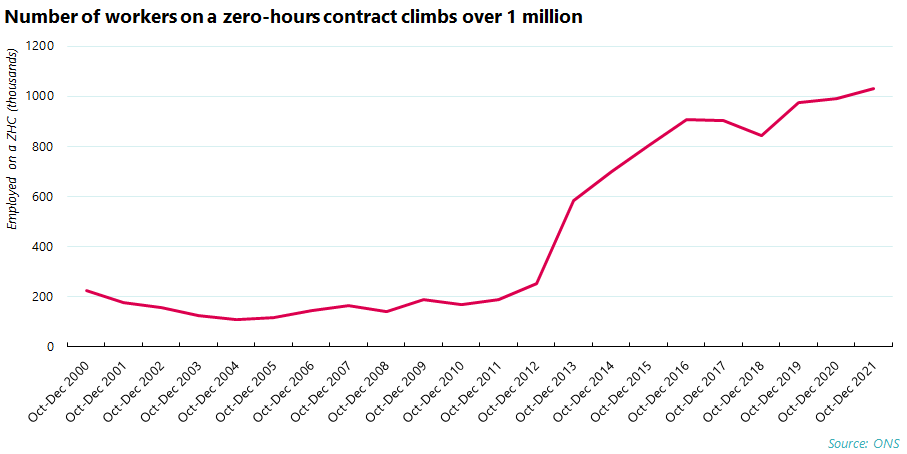

Insecure work has also increased over the pandemic. The latest figures for the fourth quarter of 2021 show zero-hour contracts back above one million. BME women are twice as likely to be on these contracts, which do not guarantee any hours, compared to white men.8

- 7 TUC Jobs and recovery monitor #9 – disabled workers: https://www.tuc.org.uk/research- analysis/reports/jobs-and-recovery-monitor-disabled-workers

- 8 TUC analysis of Labour Force Survey

The impact on working people

The failure of pay to keep up with the rising cost of living is having real impacts on working people’s daily lives.

Throughout the pandemic, low-paid workers have been hit harder than well-paid workers. Low-paid workers have been more likely than well-paid workers to face a hit to their household finances, were more likely to face job losses, more likely to have inadequate or no sick pay when self-isolating, more likely to be furloughed without having their wages topped up, and much less likely to be able to work from home.

Workers in lower-paid occupations have also been more likely than those in better paid jobs to die from the virus.9

Low paid workers are also suffering most from rising prices. Research 10 undertaken over Christmas by the TUC showed that:

- One in eight workers (12 per cent) say they will struggle to afford the basics in the next six months. And a fifth of working people (22 per cent) say they’ll struggle to afford more than the basics.

- Low-paid workers are more likely to be struggling. One in six (17 per cent) low- paid workers (those earning less than £15,000 a year) say they will struggle to afford basics in the next six months, and three in 10 (29 per cent) say they’ll struggle to afford more than the basics.

- Nearly one in five families (18 per cent) with children under 11 will struggle to afford the basics

- Over one in five (21 per cent) disabled workers will struggle to afford the basics, compared to 10 per cent of non-disabled workers

- 14 per cent of key workers say they’ll struggle to afford the basics in the next six months, compared to 10 per cent of non-key workers

- 14 per cent of BME workers say they’ll struggle to afford the basics in the next six months, compared to 11 per cent of white workers

- a fifth of workers (21 per cent) say they have Christmas debts to pay off this year – a number that rises to over a quarter (28 per cent) for workers with children of school age.

The interaction with monetary policy

Decisions taken by the Chancellor in the spring statement will interact with those taken independently by the Bank of England. The Bank of England have raised rates to 0.5 per cent in two steps: December (0.15%) and February (0.25%). Reckoning inflation threatens economic stability, they are acting deliberately to reduce aggregate demand, restrain economic growth and contain pay rises. Even with (in February, ahead of the Ukraine conflict) inflation expected to fall below target by 2024, real pay is at that point to be expanding by only ½%. These rate rises will mean a hefty hit to households with mortgages and who rely on loans, and likewise to businesses.

The inflationary pressures come from the cost side, and MPC members have been clear that domestic policy cannot prevent rises in energy and other prices set in international markets – for example transportation costs. Instead they warn of ‘second round effects’, and the need to ensure “households and businesses” recognise that “persistent high inflation in their own wage and price setting” will not be “tolerated” (in the words of committee member and deputy governor Dave Ramsden).11

We think this the wrong approach: the case for higher pay is stronger than the case for higher interest rates.

On the latter, there is very limited evidence to suggest pay is rising in the way the Bank think. As set out above, nominal pay growth may be higher than before the pandemic, but by only a little and falling far short of compensating for inflation. Across industries the slowdown in pay growth of course is exaggerated and to some extent artificial, but the only areas where pay growth is both relatively high and accelerating are wholesale industries, real estate and finance.

In our latest Jobs and recovery monitor we contest the argument that further upward pressures lie ahead deployed by the Bank. 12 Any rise in workers registered as inactive is normal in a recession, and likely quickly to reverse when economic activity picks up pace. Likewise arguments motivating inflationary pressure by low unemployment conveniently forget that the same argument was used throughout the austerity decade without wage inflation materialising. The Bank of England Agents’ survey offers a new perspective on higher pay growth, but TUC and ONS survey sources suggest

otherwise. Beyond the position on pay, the robustness of wider macro conditions is also over-blown: investment and trade are very weak, and consumer demand is already fragile. Jobs growth has slowed in recent months, and, along with hours, is still some way below the pre-pandemic position. On top of fragile economic conditions and higher inflation, workers’ real spending power will also be hit by rises to NI and income tax thresholds.

But even if pay were rising as the Bank think, it would be a good thing and should not be contained by raised rates. Higher pay is necessary to protect workers and to support spending in the economy. And there are good reasons to believe that allowing workers’ pay to rise will not lead to further inflation.

First – even according to the zero-sum mindset that defines policy thinking 13 - firms could increase pay and take a hit on profits. The labour share in the UK has fallen significantly over the past 60 years, from 59% in the two decades after the Second World War to 48% in the five years ahead of the pandemic. The hit on profits might be absorbed as lower dividend payments, which have for the past decade risen rapidly as pay has stagnated.14

Second – outside the zero-sum mindset – a pay rise will further advantage the economy. Treating workers properly should lead to productivity or supply side gains. And, likely more importantly, higher pay will mean demand is strengthen rather than reduced.

Third, pay and prices might be allowed to rise together so that firms and households are both immediately advantaged – this has been called ‘running the economy hot’. Under these conditions any disadvantage is to the wealthy, with asset values hit by higher inflation but workers and firms protected (though asset holders might also be protected as in the case of index-linked gilts - in this case by the taxpayer). Increasing interest rates now risks privileging wealth over workers.

The response we need from government: a boost to real pay

With workers’ pay squeezed for well over a decade, it has been significantly harder for families to weather the rise in prices experienced this year. Boosting workers’ pay is the best way to help address these pressures, as well as essential for ensuring a secure recovery and stronger and fairer growth in the future.

In the next section we set out the additional measures that government must take to address temporary price pressures, including those stemming from the conflict in Ukraine. But raising pay must be at the centre of the government’s response to raising living standards, as the Prime Minister recognised when he called for a ‘high wage, high skill, high productivity economy’15.

Achieving that aim requires immediate policy action on minimum wages, public sector pay and collective bargaining, and an approach to economic policy which supports workers rather than holds them back. It also requires longer term change to the way economic growth is delivered, which we address in section five.

The government should boost minimum wages

The TUC has called for an immediate rise to the minimum wage to £10 an hour. While the increase to £9.50 for older workers is a step towards that goal, the TUC strongly believes that:

- The wage rise should apply to all workers, not only those over 23; and

- The government should set a much more ambitious target for the minimum wage.

The government must fund decent pay rises in the public sector

Public sector workers have endured pay freezes and pay restraint since the coalition took office in May 2010.

Reduced pay meant reduced spending by public sector workers, this damaged the economy and so meant reduced private sector pay. Over the fourteen years since before the global financial crisis, public and private sector pay have moved together and have ended up virtually no different from their relative starting points. Real public sector pay is down 1.6 per cent and real private sector down -0.2 per cent (on the basis of RPI real pay on both measures if down by about 10 per cent).

- 9A tale of two pandemics: low-paid workers hit hardest by Covid class divide, TUC (2021). Available at: https://www.tuc.org.uk/blogs/tale-two-pandemics-low-paid-workers-hit-hardest-covid-class-divide

- 10 BritainThinks conducted an online survey of 2,209 workers in England and Wales between 14th and 20th December 2021, based on the same nationally representative sample criteria as previous waves. See TUC (7th Feb 2022) ‘Number of workers on universal credit up by 1.3 million since the eve of the pandemic’ at https://www.tuc.org.uk/news/number-workers-universal-credit-13-million-eve-pandemic

- 11 Shocks, uncertainty, and the monetary policy response’, speech by Dave Ramsden, 22 Feb. 2022: https://www.bankofengland.co.uk/speech/2022/february/dave-ramsden-speech-at-the-national-farmers- union-conference-2022

- 12 TUC Jobs and recovery monitor, note 2.

- 13 See Heather McGhee (2021) The Sum of Us: What Racism Costs Everyone.

- 14 Over 2014 to 2018, dividends to FTSE 100 shareholders rose by 58.3 per cent while average UK worker wages increased by just 8.8 per cent (in nominal terms). ‘How the shareholder first business model contributes to poverty, inequality and climate change’, 2019, briefing note from High Pay Centre and the TUC: https://www.tuc.org.uk/sites/default/files/2019-11/Shareholder%20Returns%20report.pdf

Government must not make the same mistake again. Instead, it should provide funding to ensure that:

- all public service workers get a pay rise that at least matches the cost of living and begins to restore earnings lost over the last decade, through fully independent pay review bodies or collective bargaining

- all outsourced workers are paid at least the real Living Wage and receive pay parity with directly-employed staff doing the same job.

The government must give workers greater powers to negotiate through their trade unions for better pay

The best way to ensure decent work, and workers who are happy to work in these jobs, is through collective bargaining between workers and employers – a flexible way to drive up conditions, discuss recruitment and training, and ensure fair pay. This approach has been common across Europe for decades, and Governments across the world from the US to New Zealand, are now recognising the benefits, with New Zealand introducing new fair pay agreements to regulate pay and conditions across sectors through bargaining.16

The government’s long delayed employment bill offers a further opportunity to support this approach through strong legislation, including a ban on zero hours contracts, and fair scheduling rules to ensure decent notice for shifts, payment for cancelled shifts, and a right to guaranteed hours. Government should:

- allow trade unions to access workplaces to tell people about the benefits of joining a union

- begin the process of setting up fair pay agreements which allow workers to negotiate a minimum rate for the job across whole sectors

- finally introduce an employment bill that bans zero hours contracts, and fair and fair scheduling rules to ensure decent notice for shifts, payment for cancelled shifts, and a right to guaranteed hours.

Government must act to close pay gaps

Government must take measures to support equal pay including strengthening the gender pay gap reporting requirements, and introducing ethnicity and disability pay gap reporting.

Pay gap reporting measures should require employers to publish actions plans on what they are doing to close the pay gaps they have reported. Action plans should cover recruitment, retention, promotion, pay and grading, access to training, performance management and discipline and grievance procedures relating to staff and applicants. It is vital that intersectional issues – for example, those affecting disabled women – are acknowledged and addressed.

Government must use fiscal policy to support higher pay

We are concerned that policymaker’s (ongoing) reaction to the present inflation will needlessly make matters worse for workers. As we set out above, the strength of the economy and pay growth is exaggerated, and action based on the idea that pay is rising strongly will further threaten recovery. Holding back pay in order to protect assets held by the wealthy from inflation is not the right strategy. As trade unions have always understood, doing so is counterproductive both in terms of fairness and in terms of a stronger economy. The present inflation should not be one of a number of repeated excuses to avoid action to build back better.

According to the Treasury and the Bank of England, fiscal and monetary policy need to be tightened to reduce activity, restrain pay and improve the public sector finances.17 We argue instead that higher pay and so higher spending power are necessary to support the economy in the short term and as foundations to building back better.

The government should learn from both the good lessons of the pandemic and the bad lessons of the austerity decade. Under the furlough scheme the government supported businesses to pay wages, and in doing so sustained household spending. Other government expenditure, not least on healthcare, also served to support the wider economy, and those of other countries. These actions aided a rapid recovery from lockdowns, and also meant that the hit to public finances was far lower than expected. For example public sector net borrowing in 2021-22 was expected in March 2021 to be £234bn, and this was reduced to £183bn in October, and is currently running £18bn below that forecast.18 The contrast with the austerity decade could not be sharper, when reduced spending on public sector salaries, investment and services reduced incomes and spending in the economy. The consequent greatly slower growth meant the public debt ratio was not reduced at all. 19

Yet inflationary pressures have led again to the approach that has been so toxic over the past decade. In particular, the government has restored the zero-sum thinking that dictates its approach to pay. Last year’s promises of a real terms rise to public sector pay across the board have been disregarded. The Treasury submission to pay review bodies now calls for restraint.20

As set out above, this is precisely the wrong approach. The idea that pay in the private and public sector should broadly match on average is nonsensical.

The response we need from government: immediate action to tackle the rising cost of living - and action to ensure our response to the invasion of Ukraine is effective

As we set out in a letter to the Chancellor on the 2nd of March, the Trade Union movement is united in its condemnation of Russia’s illegal invasion of a sovereign nation. Our solidarity is with the working people of Ukraine. Working people always suffer in conflict and the pursuit of peace is a fundamental trade union value, an essential condition to secure safety, social justice and workers’ and human rights.

The UK government must now take further action to support and strengthen international efforts to impose significant and effective sanctions on Russia and to support all diplomatic efforts towards peace. And it must play its part in supporting humanitarian assistance for forcibly displaced people and welcoming refugees seeking to come to the UK.

The government must also ensure that it takes every step possible to protect working people here at home from the impact of the conflict and measures taken in response to this. This must include addressing longstanding issues – including inadequate social security, sick pay, and childcare, that have made working families more vulnerable to the impact of price rises.

Measures in direct response to the conflict:

Target sanctions on wealthy elites linked to the Russian government - and ensure they are effective

- We welcome the proposed register of overseas owners of UK property through the Economic Crime (Transparency and Enforcement) Bill, but this needs to be backed up by sufficient powers and funding for Companies House to enforce

Fund humanitarian assistance for displaced people, and welcome refugees to the UK

- The new Ukrainian visa proposals are inadequate and fall well short of what is needed. Limiting asylum to Ukrainian immediate family members, of those already settled in the UK, will not reassure Ukrainians fleeing war and bloodshed that they will be able to seek sanctuary in our country. The government must establish a safe route, so all Ukrainian families, who through no fault of their own have been forced from their homes, can eas ily apply for a humanitarian visa to travel to the UK. The Nationality and Borders Bill must be scrapped. Thousands of Ukrainians fleeing war may try to find sanctuary in the UK. If the Bill is passed many of these Ukrainians, along with others around the world fleeing conflict, threats to their lives and seeking safety may find themselves treated as criminals and deported, instead of being offered sanctuary.

Measures to tackle the impact of rising prices and support families with the cost of living:

Protect working families against rising gas prices, by raising funds through a windfall tax on energy profits and the tax on profits made by UK companies invested in Russian state businesses.

The current energy price crisis is hitting workers hard, and prices are likely to rise further. Government should implement existing TUC calls for:

- Support for households in the form of a grant, not a loan (replacing the energy price rebate proposed by the government).

- An increase in the warm homes discount.

- Rapid implementation of an accelerated and expanded domestic home retrofit programme, delivered by local councils who are best placed to deliver fast

- Funding for these measures by the implementation of a windfall tax on north sea oil and gas companies’ profits.

Protect jobs in supply chains now and build future supply chain resilience.

For companies sourcing parts and supplies from Russia, sanctions could have a significant impact. To protect jobs, the UK government should:

- Re-introduce the furlough scheme or a permanent short-time working scheme in order to allow companies to protect jobs while they seek to shift their supply chains. 21

- Begin an urgent programme to provide investment support to help companies to invest in UK supply chains and jobs.

Fix the holes in the safety net which have left working people vulnerable to rising prices

The degradation in the level of social security over the last decade has meant that families are significantly more vulnerable to the impact of rising prices. There are now over a million more working people claiming Universal Credit than at the start of the pandemic,22 and although the reduction in the taper rate announced at the last budget will provide some additional support, they still face a significant squeeze on their incomes, with those who have lost their jobs hit even harder.

- The basic level of Universal Credit and legacy benefits, including jobseekers allowance and employment and support allowance, should be raised to a value worth at least 80 per cent of the national living wage.

- The arbitrary benefit cap should be removed permanently.

- The government should significantly increase benefit payments to children and remove the two-child limit within universal credit and working tax credit.

- Government must also remove the No Recourse to Public Funds (NPRF) restrictions. Everyone living in the UK must have access to public funds.

Sick pay for all

The government response to the consultation on ‘Health is everybody’s business’ stated that “now is not the right time to introduce changes to the sick pay system.”23 The TUC believes that the time is long overdue to ensure that everyone can afford to take time off work when they are sick, ensuring a health recovery for themselves, their workplace and the wider economy. Government should:

- Remove the ‘lower earnings limit’ that prevents around two million people from qualifying for sick pay. The estimated cost of this is around £150m a year, if government chose to subsidise the costs.

- Increase statutory sick pay to the level of the real living wage, around £330 a week. The estimated cost of this to employers is around £110 per employee a year for those employers who don’t currently pay occupational sick pay. 24

- Introduce day one sick pay for all workers. With the return of waiting days for coronavirus, workers will now receive just £38 for their first week of isolation.

A funding boost for childcare

Childcare costs add significantly to the cost of living for working families. The pandemic has had a devastating impact on the childcare sector for childcare workers, parents and children. In the six months up to March 2021 there were 14,385 fewer childcare places and 3,292 fewer providers in England.25 Research has also shown that the pandemic has exacerbated recruitment and retention problems in the sector and many childcare workers have been pushed below the poverty line, made worse by a lack of access to sick pay during Covid-19.26

Working parents have seen their access to formal and informal childcare impacted by the pandemic, this is particularly true for working mothers. Our 2021 research found that a fifth of working mothers who responded to a survey were going to have to take unpaid leave to manage their childcare over the summer holidays.27 Children and families from disadvantaged backgrounds were most likely to be unable to access formal childcare during the pandemic.28 Before the pandemic, according to data from Coram Family and Childcare, for disabled children in England, only 25 per cent of local authorities reported having sufficient childcare in 2020.29

Lack of access to affordable childcare was an issue before the pandemic, and again has been exacerbated by it. Long term we know the disproportionate burden of care on women, and the lack of affordable childcare provision and access to flexible working have negative impacts on women’s career progression and are key drivers of the gender pay and pension gaps at 15.4 per cent and 37.8 per cent respectively.

We must recognise childcare as vital infrastructure for any levelling up agenda, and the enabler of employment that it is. We need a new deal for childcare workers and parents and their children alike. Government should invest in good quality, affordable childcare to help the sector and families recover from the pandemic and build a sustainable future for the childcare sector.

Immediately government should:

- Give an urgent cash boost for the sector – like the financial help given to transport networks – to give childcare workers better wages, and a long- term settlement to make sure childcare is affordable and available for families

- Raise the minimum wage to 10 per hour immediately. Our analysis shows that over 170,000 childcare workers would benefit, particularly women and young workers.30

Improving pensions

Pensioners also face significant pressures from rising prices, adding to the impetus for reforms to deliver more secure pensions to all workers.

Improving the state pension

The decision to suspend the triple lock for 2022/23 and increase state pensions in line with the September Consumer Prices Index means the state pension will not keep up with price rises this year. At 3.1 percent, CPI inflation in the 12 months to September was less than half Bank of England’s central projection for April 2022 of 7¼ per cent.

The TUC has argued that the low level of the UK state pension31 and the low ratio of government spending on state pensions to GDP32 relative to other OECD countries, meant the triple lock should have been maintained. At the very least government should recognise the unusually rapid increase in inflation from September to April, and use the latter figure for uprating. Failing to do so will reduce real incomes this year by

£388 for someone on the full new state pension and £297 for someone on the full basic state pension. This cut will hit the lowest income pensioners the hardest, with those in the lowest income quintile relying on benefits for over 80% of income.33

The government must also use the current Independent Review of the State Pension Age to urgently rethink plans to increase the state pension age to 68 by 2039. The latest life expectancy projections show this is completely incompatible with the government’s policy aim over the last decade of maintaining the proportion of adult life people spend in receipt of the state pension at one third.34

The TUC also believes that planned increases should be shelved to prevent existing inequalities of class and ethnicity from widening in old age. TUC analysis has found that workers in low paid and manually intensive jobs and BME workers are already significantly more likely to be forced out of the labour market before state pension age by ill health, or because of caring responsibilities.35

Workplace pensions

The TUC supports cross party calls to expand auto-enrolment to bring more low-paid, part-time and young workers into the occupational pension system.36 In particular the government should implement the recommendation from the 2017 Review of automatic enrolment to phase out the lower earnings limit as soon as possible. The government has pledged to do this, but TUC analysis found that delaying implementation by 6 years could reduce the pension pot of a low paid worker by £12,000.37 Removing the lower earnings limit should be followed by the phasing out of the earnings threshold and setting out plans to increase statutory minimum contribution rates to ensure all workers have automatic access to a decent workplace pension.

These measures to expand auto-enrolment would particularly benefit women, who are more likely to be in part-time or low-paid work, and help reduce the gender pensions gap, which stands at 37.9 percent.38

The response we need from government: Creating an economy based on decent work

Government needs to take longer term steps to change the way our economy works and the incentives that shape it so that economic growth translates into good quality jobs. This requires an institutional environment that encourages the development of business models based on high-wage, high-skilled and secure jobs, rather than a reliance on low-paid and insecure work.

We need a new skills strategy that gives people rights to training and development throughout their working lives. It also requires reforms to our corporate governance system so that companies are encouraged to focus on long-term, sustainable growth that distributes a fair share to workers, rather than prioritising short-term returns to shareholders. We need to develop a new, green industrial policy with effective measures for creating and supporting good quality jobs in sectors that will equip the UK for the transition to net-zero and trade policies that will raise employment standards in the UK and around the world. And we need sustainable public services that support decent jobs and communities across the UK.

A skills strategy for all workers

The TUC is calling for a new national lifelong learning and skills strategy based on a vision of a high-skill economy, where workers can quickly gain both transferable and specialist skills to build their job prospects. Some key measures could be rolled out swiftly now, with longer-term reforms put in place to tackle entrenched failings in our skills system that limit employment prospects and personal development. A strategic approach along these lines could be delivered at pace by a National

Skills Taskforce that would bring together employers, unions and other key stakeholders along with government.

There are four key areas of reform that should be at the heart of a lifelong learning and skills strategy to address these challenges:

- A significant boost to investment in learning and skills by both the state and employers is essential.

- People should have access to fully-funded learning and skills entitlements and new workplace training rights throughout their lives, expanding opportunities for upskilling and retraining.

- Expand access to high quality apprenticeships for all young people wishing to take up this option.

- We need a national social partnership, bringing together employers, trade unions and government, to provide clear strategic direction on skills - as is the case in most other countries.

- Our college workforce must be empowered and properly rewarded for their work; an immediate priority must be to tackle the long-term decline in pay in the sector.

Government should also restore funding for the successful Union Learning Fund.

Corporate governance reform to promote long-term, sustainable growth

Shareholder primacy in corporate governance encourages directors to prioritise shareholder returns over wages and long-term investment, fuelling short-termism and poor employment practices. We need to address shareholder primacy through reform of directors’ duties and promoting workforce voice in corporate governance.

The inclusion of worker directors on company boards would bring people with a very different range of experiences into the boardroom, which would help to challenge ‘groupthink’ and change the culture and priorities of the boardroom, improving the quality of board decision-making.

- Directors’ duties should be reformed so that directors are required to promote the long-term success of the company as their primary aim, taking account of the interests of stakeholders including the workforce, shareholders, local communities and suppliers and the impact of the company’s operations on human rights and on the environment.

- Company law should require that elected worker directors comprise one third of the board at all companies with 250 or more staff.

An industrial strategy for good, green jobs

The UK’s industrial and manufacturing base has experienced a hollowing-out since the 1980s. Between 1960 and 2015, UK manufacturing employment declined more sharply than any other advanced economy except Switzerland.39

UK industries risk falling further behind if the pace of industrial retooling for Net Zero does not match that of international competitors. The need to update business models and technologies to support a decarbonised economy will create fierce international competition for investment, for example, in the automotive components manufacturing industry.40 Ensuring adequate and timely support for industrial decarbonisation and retooling will secure the future of up to 600,000 jobs in manufacturing and supply chains, according to TUC research.41

Industrial strategy has an important role to play in levelling up, but supporting good quality employment must be a core part of the strategy. We need an ambitious programme that rebuilds the UK’s industrial capacity, tackles regional inequalities, and positions UK industries to be ready for, and benefit from, the transition to Net Zero.

Strengthen supply chain commitments for infrastructure and energy projects

To boost domestic manufacturing, services and technology development, and reap the full benefit of developments in infrastructure and renewable energy, the government should adopt strong trade and procurement policies to strengthen local supply chains and employment standards.

While mindful of restrictions on the use of local content requirements in WTO and EU trade treaties, the UK government should use such policies where they are legal and needed.

- To bid for infrastructure contracts or energy subsidies auctions, companies should be required to demonstrate commitments to strong labour and human rights standards across their supply chain, and to lay out how they will strengthen local supply chains and what level of local content they expect to achieve. Companies should be held accountable for these commitments.

- The UK Government’s Offshore Wind Sector Deal’s ambition for 60% lifetime UK content is clearly insufficient. An estimated 35% of windfarm expenditure is in operations, maintenance and service 42

(most likely to be local regardless of targets). The local content target for offshore wind should be brought up to at least 80%. - The UK should make use of geographical exceptions to state aid rules (e.g. successor to the EU Assisted Areas Map), and where appropriate, apply for sectoral treaty exceptions based on public interest, to strengthen local supply chain rules.

- The UK should also use future international trade negotiations to expand governments’ ability to use conditions on investment to strengthen domestic supply chains.

Future-proofing industrial workplaces

Greater public investment is needed to decarbonise and retool UK industry and supply chains, protect local jobs and economies and maintain international competitiveness. This is especially important for high carbon sectors already affected by UK and international carbon regulations and increased international competition, for example, steel production. Without sufficient support, high-carbon employers may choose to relocate production to jurisdictions with a lower cost of carbon (a process known as carbon leakage), or conversely to countries that offer more support for developing and scaling-up zero-emissions technologies. Either process would risk losses to skilled jobs and productivity in the UK.

- The government should invest at scale in future-proofing industrial workplaces.

- Fund regional economic diversification, to meet climate targets and support levelling up

The relative success of past regional transition programmes in Europe demonstrate that a long-term commitment to public investment is key – for example, the 25-year regional funding for economic diversification in the coal centre of Limburg in the Netherlands.43

The EU committed €17.5 billion towards its Just Transition Fund, financed through the EU budget and Recovery Instruments and to be further match-funded through the European Regional Development Fund (ERDF) and European Social Fund (ESF).44 This will be invested in small and medium enterprises (SMEs), land restoration, emission reduction and research & innovation, targeted at any regions at risk of being left behind through the decline of high-carbon industries

- Where local economies depend on high carbon local employment that cannot be retooled, the UK should provide funding equivalent to the EU’s ‘Just Transition Fund’ to support communities to diversify and develop alternative industries.

Decent public services

Public services were weakened by a decade of needless austerity. Government must now put in place a plan to ensure that we have the strong resilient services we need to face the future. In addition to the measures on public sector pay set out above, this must include:

- Creating 600,000 new jobs in public services, including 355,000 jobs in health and social care, 80,000 jobs in education and 50,000 jobs in the civil service.

- Investing in an NHS for today and tomorrow, working with unions on a fully- funded, long-term workforce strategy.

- A sustainable funding settlement for social care based on equalising the rates of capital gains tax with income tax, generating an additional £17 billion per annum.

- A significant boost to the funding of justice to address backlogs and excessive workloads.

- Introducing a comprehensive programme of investment in education to reverse the damage to pupil’s learning as a result of the pandemic.

- The government should demonstrate a firm commitment to the protection of public service pension schemes in line with the 25-year commitment following revisions to public sector pensions from 2015.

Conclusion: building back better

The promises to ‘build back better’ after the pandemic must not be forgotten. Beyond the immediate challenges of rising prices and falling real pay, government needs a strategy to deliver a better economy for working people.

Any such approach must recognise that the economy has for too long served the interests of the wealthy ahead of labour. As a result there is vastly excessive money in the hands of the few, and too little in the hands of the many. Looking at the inflation debate in this broader context, former US Secretary of Labour Robert Reich warned last year:

“Here’s the thing. The wealthy spend only a small percentage of their income – not enough to keep the economy churning. Lower-income people, on the other hand, spend almost everything they have – which is becoming very little. Most workers aren’t earning nearly enough to buy what the economy is capable of producing”. 46

In this way, low wages put production out of reach of workers. Moreover, excess wealth is constantly seeking new outlets for capital gain, fostering excesses in property, production in cutting edge technologies, and in ripe-for-exploiting overseas economies. Today, think high end residential property, the FAANG – Facebook, Amazon, Apple, Netflix and Google (now Alphabet) – companies, and the notions (courtesy of Baron O’Neill, then of Goldman Sachs) of BRIC – Brazil, Russia, India and China – and MINT – Malaysia, Indonesia, Nigeria and Turkey – economies.47

The ongoing and unresolved private debt crisis across the world follows as unsold production leads firms to rely on borrowing, and deficient incomes mean too many households rely on credit and loans to get by. Policy since the global financial crisis has exacerbated these imbalances, with austerity meaning workers’ incomes were restrained, while quantitative easing advantaged the wealthy as asset values soared.

High levels of debt create additional risks to monetary policy. Actions that might protect against price inflation are much riskier, with high levels of debt meaning greatly higher interest payments and a threat to financial confidence more generally. So while central banks have tried repeatedly to tighten policy, they have retreated when financial markets reacted badly.48 The pandemic struck in the aftermath of the latest retreat with growth across much of the world grinding to a near halt in 2019; the systemic risk council remarked:

"Covid-19 strikes the world at a time when too many corporations around the world are over-indebted, and after a period during which persistently favourable market conditions caused traders to take aggressive positions, exposing them and the system to spikes in volatility, let alone a collapse in asset values”.49

Even ahead of the conflict in Ukraine financial markets were nervous about the tightening of monetary policy that is happening across the world. This policy dilemma may fall to the Bank of England, but should be understood a symptomatic of the unsustainability of the system as a whole. 50 Policymakers have not found a way forward to resolve the global financial crisis, and instead keep falling back on old broken ways. The head of the IMF Kristalina Georgieva has called out a Bretton Woods moment,51 “to fight the crisis today – and build a better tomorrow”. Trade unions contend any such approach must reset the balance to labour from wealth.

The system that sacrifices the needs of the many to the interests of the few needs to be brought to an end.52 As trade unions have always understood, doing so is counterproductive both in terms of fairness and in terms of a better economy. The present inflation should not be one of a number of repeated excuses to avoid discussion of building back better.

- 16 See for example Employment New Zealand: https://www.employment.govt.nz/starting- employment/unions-and-bargaining/collective-agreements/collective-bargaining

- 17 “In the current context, where inflation is expected to temporarily peak at its highest rate in over a decade, it is imperative that Pay Review Bodies also have regard of the government’s objective for price stability, defined in the Monetary Policy Committee’s remit as a 2 per cent inflation (CPI) target”; HMT Economic Evidence to the Pay Review Bodies, Dec. 2021: https://www.gov.uk/government/publications/hmt-economic-evidence-to-review-bodies-2021

- 18 From the relevant Office for Budget Responsibility Economic and fiscal outlook documents; and their commentary on the latest ONS public sector finance dataset: [ref]

- 19 Lessons of a Decade of Failed Austerity, TUC, 2019: https://www.tuc.org.uk/research- analysis/reports/lessons-decade-failed-austerity

- 20 See n.17.

- 21 For further details on the TUC’s proposal for a permanent short-time working scheme see TUC (August 2022) Beyond furlough: why the UK needs a permanent short-time work scheme at https://www.tuc.org.uk/research-analysis/reports/beyond-furlough-why-uk-needs-permanent-short-time- work-scheme

- 22 See TUC (7th February 2022) ‘Number of workers on universal credit up 1.3 million since the eve of the pandemic’ https://www.tuc.org.uk/news/number-workers-universal-credit-13-million-eve-pandemic

- 23 HM Government (2021) Government response: health is everyone’s business at https://www.gov.uk/government/consultations/health-is-everyones-business-proposals-to-reduce-ill- healthrelated-job-loss/outcome/government-response-health-is-everyones-business

- 24 See Andrew Harrop (2021) Statutory sick pay: options for reform Fabian Society, available at https://fabians.org.uk/wp-content/uploads/2021/06/SSPreport.pdf

- 25 https://wbg.org.uk/analysis/access-to-childcare-in-great-britain/

- 26 https://childcare-during-covid.org/final-report-essential-but-undervalu…- covid-19/

- 27 https://www.tuc.org.uk/sites/default/files/2021-07/SummerholidayReport.pdf

- 28 https://childcare-during-covid.org/final-report-essential-but-undervalu…- covid-19/

- 29 https://wbg.org.uk/analysis/access-to-childcare-in-great-britain/

- 30 https://www.tuc.org.uk/news/increasing-minimum-wage-ps10-hour-would-give-over-170000- childcare-workers-pay-rise-says-tuc

- 31 At 21.6 per cent, the percentage of an average workers income replaced by the state pension in the UK is just over half the OECD average of 42.2 percent, see OECD Pensions at a glance 2021, table 4.2, https://www.oecd-ilibrary.org/sites/ca401ebd-en/index.html?itemId=/content/publication/ca401ebd-en

- 32 At 7.1 per cent of GDP, UK spending on old age benefits was below the OECD average of 7.7 per cent, see OECD Pensions at a glance 2021, table 8.3

- 33 DWP, Pensioners’ Incomes Series: financial year 2019 to 2020, March 2021, https://www.gov.uk/government/statistics/pensioners-incomes-series-financial-year-2019-to- 2020/pensioners-incomes-series-financial-year-2019-to-2020

- 34 LCP, Twenty million adults could be in line for ‘state pension age reprieve’ as life expectancy improvements ‘collapse’ even before the Pandemic, December 2021, https://www.lcp.uk.com/media- centre/2021/12/twenty-million-adults-could-be-in-line-for-state-pension-age-reprieve-as-life-expectancy- improvements-collapse-even-before-the-pandemic

- 35 TUC, Older workers after the pandemic: creating an inclusive labour market, February, 2022, https://www.tuc.org.uk/research-analysis/reports/older-workers-after-pandemic-creating-inclusive-labour- market

- 36 Pensions (Extension of Automatic Enrolment) Bill, January 2022, https://hansard.parliament.uk/Commons/2022-01-05/debates/2A349903-229D-…- BDAE9C7420D8/Pensions(ExtensionOfAutomaticEnrolment)

- 37 TUC, Government "dithering” on pension reforms could cost low earners thousands, February 2019, https://www.tuc.org.uk/news/government-dithering-pension-reforms-could-cost-low-earners-thousands-0

- 38 Prospect, What is the gender pension gap?, September 2021, https://prospect.org.uk/article/what-is-the- gender-pension-gap/

- 39 International Monetary Fund (2018) World Economic Outlook, April 2018: Cyclical Upswing, Structural Change, available at: https://www.imf.org/en/Publications/WEO/Issues/2018/03/20/world-economi…

- 40 PWC (2019) ‘Merge ahead: Electric vehicles and the impact on the automotive supply chain’ https://www.pwc.com/us/en/industrial-products/publications/assets/pwc-m…

- 41 TUC (2021) Safeguarding the UK’s manufacturing jobs with climate action: carbon leakage and jobs https://www.tuc.org.uk/research-analysis/reports/safeguarding-uks-manuf…

- 42 TUC calculation based on BVG Associates (2012), Guide to an Offshore Wind Farm. https://www.thecrownestate.co.uk/media/2860/guide-to-offshore-wind-farm…. 20 year operational lifespan assumed.

- 43 Ben Caldecott et al., Lessons from Previous 'Coal Transitions’, IDDRI and Climate Strategies. 2017,p.8 https://coaltransitions.files.wordpress.com/2016/09/coal_synthesisrepor…

- 44 European Parliament (2020), Just Transition Fund: helping EU regions adapt to green economy, https://www.europarl.europa.eu/news/en/headlines/economy/20200903STO863…

- European Parliament (2020) Just Transition Fund, https://www.europarl.europa.eu/thinktank/infographics/JTF/index.html

- 46 ‘The problem isn’t ‘inflation’. It’s that most Americans aren’t paid enough’, Robert Reich, Guardian, 13 Aug. 2021.

- 47 See the TUC submission to the Lords Economic Affairs Committee enquiry on QE: https://committees.parliament.uk/writtenevidence/23786/html/

- 48 Philip Turner, formerly deputy head of the monetary and economic department and a member of the senior management of the Bank for International Settlements (BIS), has observed “Central banks have seen successive plans (in 2009, in 2013 and in 2018) to ‘normalise’ monetary policy frustrated by weak growth and low inflation”.

- 49 SRC Statement on Financial System Actions for Covid-19’, 19 Mar. 2020: https://www.systemicriskcouncil.org/2020/03/src-statement-on-financial-system-actions-for-covid-19/

- 50 The US NASDAQ index of technology stocks was down on the end of 2021 by 16.67 on 23 February; since then it has rebounded 3.8% (last reading 4 March); Source: https://fred.stlouisfed.org/series/NASDAQCOM

- 51 ‘A New Bretton Woods Moment’, October 15, 2020:

- 52 TUAC have set out a fuller argument that is global in scope in a paper presented to the OECD liaison committee. https://tuac.org/news/oecd-tuac-liaison-committee-meeting-policies-for-…- recovery-en-fr/

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox