Action to protect the economy and public services

Working people need a New Deal to boost their wages and their public services. The Chancellor should use the Spring Statement to deliver increased spending of £25 billion:

- an additional £15bn to provide rapid and material support to the economy and begin to restore the health of vital public services. This will double the planned increase into 2019/20 already set out in the Autumn Budget; and

- an extra £10bn for capital spending to help bring the UK towards the OECD average for infrastructure investment (3.5% GDP).

As well as beginning to repair the UK’s social and economic infrastructure, the actions will provide essential support to the flagging economy. This should be just the beginning of a New Deal for Working People.

Introduction

While Brexit dominates the headlines, working people across the UK are facing a crisis of living standards. Ten years after the financial crisis, wages still haven’t recovered to their pre-crisis peak, and millions face insecurity at work. The public services that people rely on have been cut to the bone – with current plans meaning that spending in five years’ time will still be £500 lower for each person than it was in 2009/10.

The living standards crisis isn’t an accident. Government’s pursuit of austerity has not only decimated public services, it has held back growth. The economic recovery that followed the financial crisis has been the slowest in over a century. A flagging global economy and uncertainty over Brexit mean that UK growth is expected to fall further this year. And even on its own terms austerity has failed, with public debt peaking at the highest level for half a century.

The Government has claimed it has recognised it’s time for a change of course; in October 2018 Theresa May announced that ‘austerity is over’. The Chancellor, Philip Hammond, is reported to be planning a spending package for use in the event of a no-deal Brexit.

But working people across the country facing low wages, stretched public services and rising personal debt can’t wait for the disaster of a no-deal Brexit before action is taken to boost the economy. And austerity is far from being over. Analysis by the New Economics Foundation (NEF), commissioned by the TUC, shows that over the period of the forthcoming spending review, departmental budgets outside of the protected areas such as health, defence and overseas aid could be facing cuts of up to 4 per cent per capita by 2023/24. 1

The living standards crisis

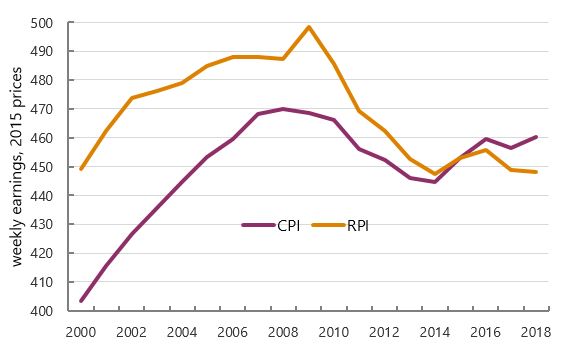

Jobs may be growing, but pressures on households continue to intensify. Real pay growth returned to positive territory in 2018, up 0.8 per cent following a decline of 0.7 per cent in 2017. But overall real pay is still down two per cent on a decade ago, amounting to a stagnation unprecedented for two centuries.2 These figures use the ONS preferred CPIH measure of inflation; looking at the Retail Price Index (RPI) the decline on 2008 is eight per cent.3 Note too that wage figures exclude the self- employed, where incomes are on average greatly below employees incomes; half of self-employed people earn less than the living wage.4

Real earnings, £ per week (CPIH and RPI versions)

- 1 Austerity by stealth? New Economics Foundation, September 2018

- 2https://www.tuc.org.uk/blogs/17-year-wage-squeeze-worst-two-hundred-years

- 3The recent contribution from the House of Lords Economic Affairs Committee has gone some way to vindicating the RPI. https://www.parliament.uk/the-use-of-rpi

- 4https://www.tuc.org.uk/news/two-million-self-employed-adults-earn-less-minimum-wage

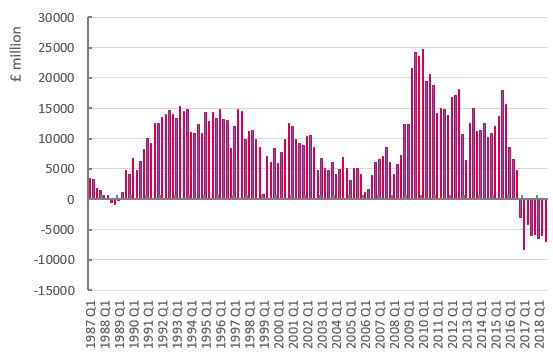

As a result, there has been an abrupt deterioration in household finances. Household income has been outstripped by spending in each of the eight quarters (of published National Accounts figures) since Theresa May took office. The chart below shows the quarterly shortfall in economy-wide terms, summing to a total shortfall of £46bn. This is equivalent to £1,700 per household.

Household net lending/borrowing, £ million

The impact of low wages and cuts to benefits can be also be seen clearly in the in-work poverty figures: the Resolution Foundation have shown that while the child poverty rate for working households averaged 20 per cent between 1996-97 and 2013-14, it is projected to increase to 29 per cent by 2023-24. 5

TUC analysis also showed the likely stress from personal debt. In the third quarter of 2018, unsecured borrowing per household was at an all-time high of £15,400.6 Unsurprisingly the evidence suggests that the greatest pressures are at the lower end of the income distribution; the National Audit Office reported that 8.3 million individuals are struggling with unsecured debts.7

Pressures on the public sector

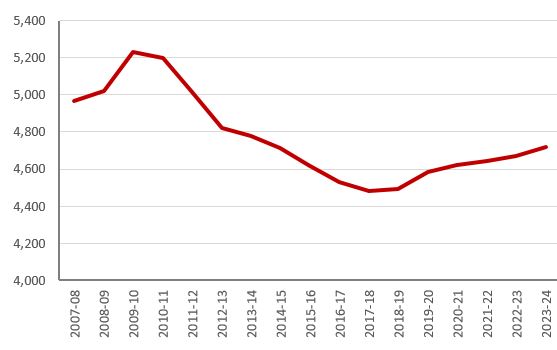

After near a decade of relentless cuts, the government finally acted in Budget 2018 to bring aggregate cuts to an end. But planned increases in spending are dwarfed by the scale of cuts to date. Austerity has reduced real departmental spending per head by 14 per cent (over the decade from 2008-09 and 2018-19), equivalent to £750 per person. Only one percentage point of lost ground will be recovered each year through to 2023-24. Given these projections are fulfilled, each of us will still be 10 per cent or £500 worse off.

Real departmental spending, £ per head

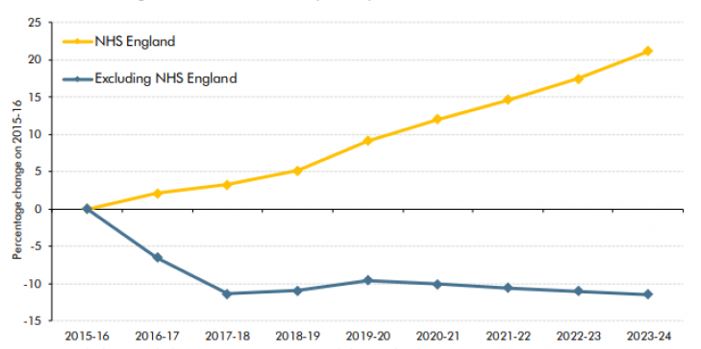

In their October 2018 Economic and fiscal outlook the OBR showed how this changed stance amounted to gains for the NHS, with, at best flatlining spending, and in many cases real terms cuts facing other departments.

Chart 4.6: Change in real RDEL limits per capita from 2015-16: NHS and other

Analysis by the New Economics Foundation (NEF), commissioned by the TUC, shows that over the period of the forthcoming spending review, departmental budgets outside of the protected areas such as health, defence and overseas aid could be facing cuts of up to 4 per cent per capita by 2023/24. That could mean £80m less per year for public health by 2023/24, £70m less for prisons and £30m less for housing.8

Even within protected areas, the promised extra funding is not enough to keep up with increasing demand or to deliver improved services. The government’s promise of an additional £20bn for the NHS by 2023 equates to a 3 per cent per year increase in the Department of Health budget. The Health Foundation and IFS estimate that a minimum of 4 per cent per year is required to maintain current service levels and 5 per cent to achieve the kind of improvements to cancer, mental health and GP services that have been outlined in the NHS Ten Year Plan.9

And, of course, none of this reverses the damage inflicted by the cuts to public spending over the last 8 years. Services have been cutback across all parts of the public sector, while the workforce struggles to cope with rising demand at a time of staff shortages – with 100,000 unfilled vacancies in the NHS alone – with the average public sector worker earning thousands less in real terms than they were in 2010.

A snapshot of local government shows exactly what austerity has done to our public services, with the Local Government Information Unit reporting that 80 per cent of councils are not confident in the sustainability of local government finance, over half will be dipping into their reserves this year and almost 1 in 10 councils expect legal challenges based on reductions in service provision.

24 per cent of councils expect to reduce activity in adult social care, 29 per cent in children’s services, 16 per cent in special needs and disability support and 11 per cent in support for the homeless. Arts and culture, waste collection and parks and leisure are facing even bigger cuts. These are the key services that support vulnerable people, our friends and our family in every community. These are the services that support vibrant, liveable and sociable areas that businesses want to invest in. The current state of play is a shameful indictment of successive governments’ austerity programmes since 2010.10

The analysis provided by NEF for the TUC estimates that departmental budgets require a further 4 per cent increase above the spending review total announced in the budget just to meet increased demand for services and a further 10 per cent to deliver ‘key improvements’ in areas like social care, education and health.

Economic context

A year ago there was widespread optimism about prospects for the UK and world economy, even given the continued uncertainty over Brexit. The growing economy was expected to lead to better wages and jobs, and potentially support increased investment in public services. As Mark Carney, the Governor of the Bank of England, put it earlier this month: 11

For the first time since the financial crisis [over the two years after the referendum], business investment and foreign trade grew strongly across all major regions. Economic uncertainty diminished, and consumer and business confidence firmed. In economies close to full employment, real wages finally began to grow. A new beginning seemed possible.

But by the end of 2018 confidence had evaporated, as Carney concluded: “In the past few quarters, however, these trends have largely reversed”. Following lower than expected growth in 2018, forecasts for 2019 have now also been lowered. ONS figures now show growth of only 1.4 per cent for 2018 (chart below), the lowest figure since the financial crisis. As a result the Bank of England have revised down expectations for 2019 to 1.2 per cent from 1.8 per cent.

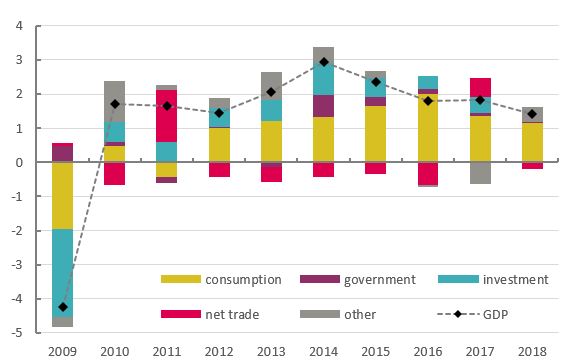

These figures show clearly that the global economy is playing an important role determining growth in the UK. In 2017 UK GDP was supported by a revival in the global economy, with net trade (in crimson) a significant upward factor. But in 2018, as the global economy deteriorated, trade became a drag on UK GDP.

Expenditure breakdown of GDP growth, percentage points

- 8Austerity by stealth?, New Economics Foundation, September 2018

- 9Securing the future: funding health and social care to the 2030s, Health Foundation and IFS, May 2018

- 10State of local government finance survey 2019, LGIU and MJ, February 2019

- 11‘The Global Outlook’, 12 February 2019, https://www.bankofengland.co.uk/speech/2019/mark-carney-speech

In parallel, investment over 2018 ground to a halt (turquoise), having provided a (generally too modest) boost to demand in every year since 2010. Once more the economy was forced to rely on the consumer (in yellow) – with the associated dangers from debt as above.

The exceptional weakness of government spending is perhaps surprising given the fragility of the situation and rhetoric around ‘ending austerity’. Government consumption and investment spending grew by only 0.2 per cent in 2018 following only 0.3 per cent in 2017. The previous chart shows how, when the coalition government boosted spending in 2014 and 2015 (in the run up to an election), GDP growth was significantly higher.

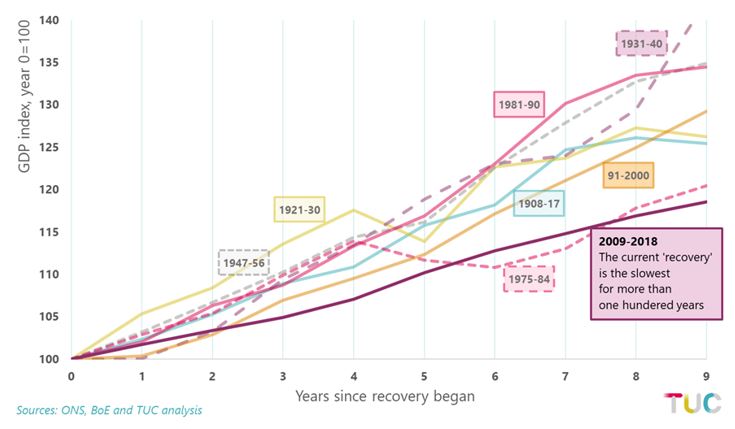

In aggregate terms, the deterioration of growth into 2018 continues the dismal decade since the start of the global recession. The average annual growth of 1.9 per cent since the low point of the recession in 2009 amounts to the weakest economic recovery for over a century.

Recoveries from recession, indices = 100 at low point

Global context

Changes in the global economy have followed changes in policy. Stronger growth in 2017 followed expansionary action by central banks and relaxed austerity policies across Europe. In 2018 policy reversed. Some countries (including the UK) put interest rates up; quantitative easing policies were moderated – with the US beginning to withdraw some of the money that has been pumped into the economy and the EU reducing the amount of money it was pumping. 12 The OECD in their November 2018 Economic Outlook observed that fiscal policy had shifted to a ‘more neutral’ stance, i.e. less support on average.

Global economic growth is now materially weaker than a year ago. In the third quarter of 2018, eight OECD countries showed negative quarterly GDP – up from between one and three over the previous two years and the highest number for around four years. Readings for the fourth quarter are now coming in: recession in Italy is confirmed, Argentina (outside the OECD) was already in recession, Turkey is highly likely to be; Germany avoided recession by a whisker, with flat rather than negative growth in Q4. The most prominent declines are to industrial production, with for example the eurozone falling by 4.2 per cent in the year to December 2018 – the largest decline since the global recession.

Count of OECD countries with negative quarterly GDP growth

- 12 From April 2017 monthly injections of €80bn were reduced to €60bn, from January 2018 to €30bn, from October 2018 to €15bn and the programme halted from January of this year.

The situation illustrates the excess reliance on monetary support. Repeatedly efforts to withdraw support cause panic in financial markets, not least given excessive leverage (e.g. ‘leveraged lending’) and asset (e.g. property) inflations across the globe. Since the start of 2019, policy makers have retreated and further rate rises now look less likely. But the ongoing fragilities strengthen the case for an alternative way forward.

The public sector finances

In his 2010 Mais Lecture to the City of London, 2010 George Osborne appealed to economists Carmen Reinhart’s and Ken Rogoff’s analysis to support austerity policies:

As Ken Rogoff himself puts it, "there's no question that the most significant vulnerability as we emerge from recession is the soaring government debt. It's very likely that will trigger the next crisis as governments have been stretched so wide."

In office, his consequent actions increased not reduced the public debt. The June 2010 plan was for debt to peak at 70 per cent of GDP in 2013-14; instead the peak came four years later at 85 per cent of GDP in 2016-17 and 2018-19. The last time the public debt ratio was at these levels was over half a century ago.13 Austerity meant weaker economic growth and weaker government revenues, so deficit reduction was greatly slower and the public debt greatly higher.

Economists are now increasingly recognising that focusing solely on the level of public debt is not a good route to deliver economic growth and better conditions for working people. Strangely, Ken Rogoff’s is among the most prominent voices: 14

To be frank it has never been remotely obvious to me why Britain chose austerity.

In parallel at the prestigious presidential lecture of the American Economic Association Olivier Blanchard (ex-chief economist of the IMF) made the argument that existing low rates of interest might make public debt costless. 15

In the UK, the IFS have argued that “there may be a strong case for some sort of fiscal stimulus” in the event of a disorderly Brexit. The National Institute of Economic and Social Research have modelled how a government stimulus of around £50bn a year (from 2022) could support the economy in the event of a no-deal Brexit, given monetary stimulus immediately after 29th March.

Increasing government expenditure

Britain is facing low growth in the context of a weakening global economy, and continued uncertainty over Brexit. Working people are experiencing rising in-work poverty and increasingly frayed public services. Britain needs a boost to economic growth now – whatever the outcome of the Brexit negotiations.

In our view government spending is preferable to further monetary stimulus, though the Bank of England should take any further interest rises off the table. Acting on public wages and service spending will impact quickly and help to reach levels that will lead to ‘key improvements’ (section 2). In addition the government should make some real ground in getting investment spending to the OECD average of 3.5 per cent of GDP.16

The government currently plans to increase departmental spending by £15bn into 2019-20; doubling this to £30bn would be more in line with the 10 per cent increase needed to deliver ‘key improvements’.17 Capital spending is expected to rise by £6bn; an additional £10bn would take expenditure about halfway to filling the gap with the OECD average.

The overall increase of £25 billion would provide material support to the economy and provide a starting point to restoring the health of the public sector over the coming years.17

A disastrous no-deal Brexit would hold back working people’s prospects further. But working people need a new deal for their wages and public services now. The Chancellor should use the Spring Statement to begin to deliver it.

- 13From the Bank of England historical data resource: https://www.bankofengland.co.uk/statistics/research-datasets

- 14‘Never mind the debt: if there’s a hard Brexit Britain will have to splash the cash’, Sunday Times, February 3 2019.

- 15 'Public Debt and Low Interest Rates', AEA Presidential Lecture, January 2019.

- 16https://www.tuc.org.uk/research-analysis/reports/tuc-autumn-budget-stat…

- 17 a b Departmental current expenditure (PSCE in RDEL) is currently estimated at 298bn in 2018-19 and is expected to rise to £313bn in 2019-20; the internationally comparable estimate of government investment is expected to rise to £62 bn in 2019-20 from £55bn in 2018-19 (OBR supplementary economy tables, 1.1).

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox