Bank taxation - 2025

Tory governments slashed taxes on banks before they left office. Since then, the big banks have been making record profits as the Bank of England has raised interest rates. These eye-watering bank profits come from higher net interest payments being made by households and businesses up and down the country. But profits are also being topped up directly by the government which is footing the exorbitant bill for payments to banks that have arisen through the Bank of England money printing programmes (see Box A).

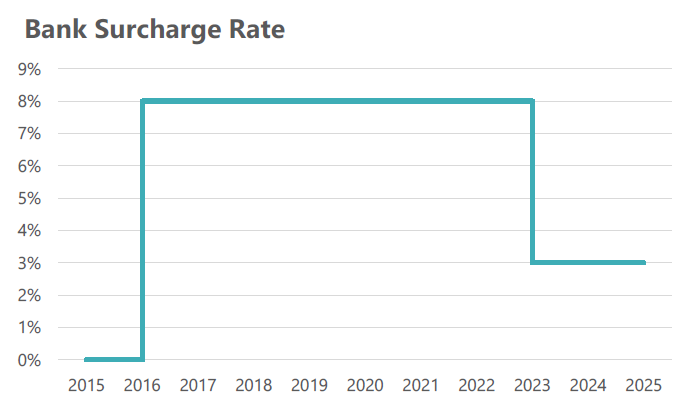

The TUC is now calling for a windfall tax on bank profits. This can be done by raising the Bank Surcharge which directly taxes bank profits. In 2021 the previous government announced a cut in the Bank Surcharge from 8% to 3%. This came into effect in April 2023. At the time decisions were made about cuts in the Bank Surcharge, there was no indication that the Bank of England would raise interest rates significantly, and that banks would make huge windfall profits as a result.

The TUC has previously highlighted bank windfalls and proposed options for taxing these profits.1 Since then bank windfalls have continued to accrue. Here are some updated options for increasing the Bank Surcharge to raise additional revenue from banks:

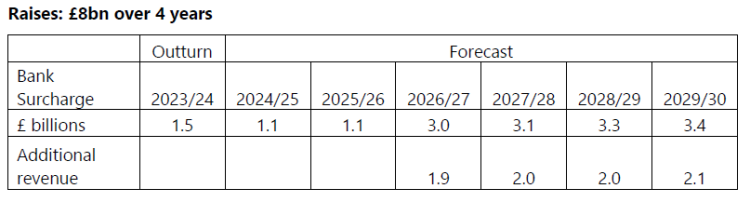

- Reverse the cuts to the bank surcharge raising it from 3% back to 8%. This would raise £8bn over 4 years.

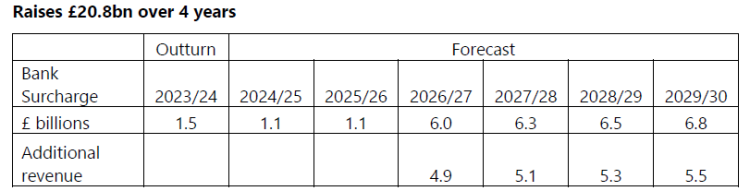

- Raise an additional £20bn over the next 4 years by increasing the Bank Surcharge to 16%. The original rate of the Bank Surcharge was 8% before the previous government cut it to 3%. This proposal doubles the original rate.

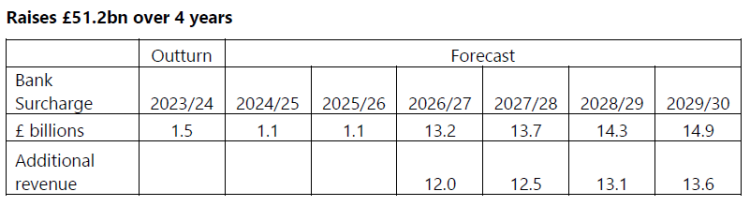

- Raise an additional £50bn over the next 4 years by increasing the Bank Surcharge from 3% to 35%. This is the same level as the windfall tax the Conservatives imposed on energy companies.

These increases could all be time-limited and reviewed at the end of the parliament. A decision could then be made about appropriate rates moving forward, considering whether banks are still making windfall profits.

- 1 TUC (2023) Bank Taxation https://www.tuc.org.uk/research-analysis/reports/bank-taxation

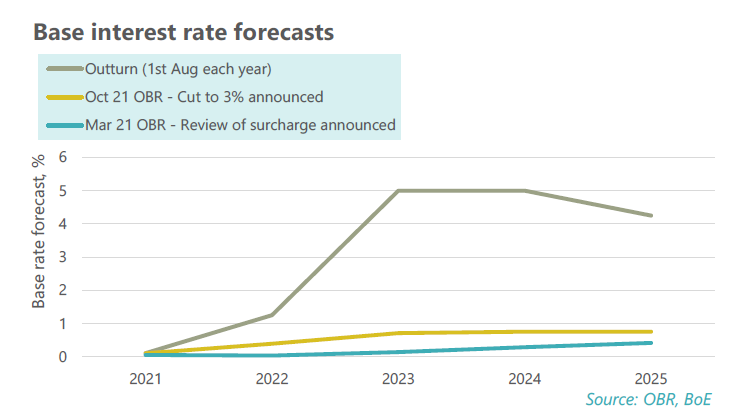

Bank windfalls

At the time decisions were made about cuts in the bank surcharge, there was no indication that the Bank of England would raise interest rates so dramatically, and that banks would make huge windfall profits as a result.

Below are the OBR forecasts for interest rates published in March 2021 (when a review of bank surcharge was launched) and October 2021 (when the bank surcharge cut was announced), alongside the Bank of England base rate outturn and forecast. Interest rates have been much higher than forecasts predicted.

Banks have made significant unexpected profits because of increased interest rates. This happens because of increases in net interest incomes – higher interest rates allow a bigger difference to emerge between interest charged to borrowers and the interest paid to savers.

Banks are also making huge risk-free returns through the interest paid to them on reserves they hold at the Bank of England. The Treasury is in effect funding these payments to banks at a time when the public finances are under serious strain.

Box A: Quantitative easing/tightening, bank reserves, interest payments and the Exchequer

Under the Quantitative Easing (QE) programme, the Bank of England (BoE) created money to buy government bonds (gilts) from the private sector; the mechanics of the transaction meant the higher central bank holdings of gilts was matched with a corresponding increase of retail bank deposits (or reserves) at the central bank.

The BoE pays interest to banks on these deposits, according to the level of Bank rate. When the interest rate was low the BoE made a profit, because the interest on its new holdings of gilts was lower than Bank rate. Under George Osborne the Treasury insisted that this profit was returned to the Treasury. The bank rate is now higher than the interest rate on the gilts held at the Bank of England, and the Bank of England are now making a loss. Worse, under its Quantitative tightening (QT) programme, the Bank of England have been selling gilts into the market at a significant loss (because newly issued gilts currently have a greatly higher interest rates than the ones purchased under QE). Just as George Osborne insisted that the Treasury advantage from gains, the Bank of England’s approach seeks to protect themselves from losses.

This means severe disadvantage to the Treasury and, because of wider repercussions to public spending, to the public. The sums of money are huge: Positive Money suggest the Treasury has paid £86bn over 2022 to 2024-25, and is forecast to pay a further £109bn over the next five financial years. 2

Even insiders like former Deputy Governors Charlie Bean and Sir Paul Tucker have warned that these processes are greatly problematic, and that the position is peculiar to the UK with other central banks operating in a less restrictive way, including not actively selling into the market holdings of government bonds.3 , 4 The current Governor has continued to make the case for these arrangements, particularly when facing scrutiny from the Treasury Select Committee (TSC).5 Though separately he remarked: "Indeed, we have in the past noted that removing remuneration on reserves is akin to a tax on banks. It is only appropriate that such a tax be imposed by the elected Government of the day." 6

The consequent windfall gains by retail banks and the immense damage to the public finances cannot be ignored.

Positive Money and IPPR 7 have suggested tax mechanisms based on identifying banks’ interest revenues that are specific to QE, but we are of the view that tax should be transparent and as simple as possible so that the public knows what is going on. The surcharge would still reflect ability to pay, given overall profits are related to QE and so any fall in cash profits as a result of changes to QE/QT processes would also mean a reduced hit from the surcharge.

- 2 Positive Money (2025) How the government could reclaim the huge payouts to banks https://positivemoney.org/uk/update/how-the-government-could-reclaim-the-huge-payouts-to-banks/

- 3 Bean (2024) ‘Spare UK taxpayers bill for QE losses’, Bloomberg Feb 2024

- 4 Tucker P (2022) ‘Quantitative easing, monetary policy implementation and the public finances’, IFS Report R223. https://ifs.org.uk/sites/default/files/2022-10/Quantitative-easing-mone…

- 5 Bank of England (2025) Letter to Treasury Select Committee committees.parliament.uk/publications/48136/documents/252164/default/

- 6 Bank of England (2025) Letter to Richard Tice https://www.bankofengland.co.uk/-/media/boe/files/letter/2025/letter-to-richard-tice-june-2025.pdf

- 7 IPPR (2025) Fixing the Leak https://www.ippr.org/articles/fixing-the-leak

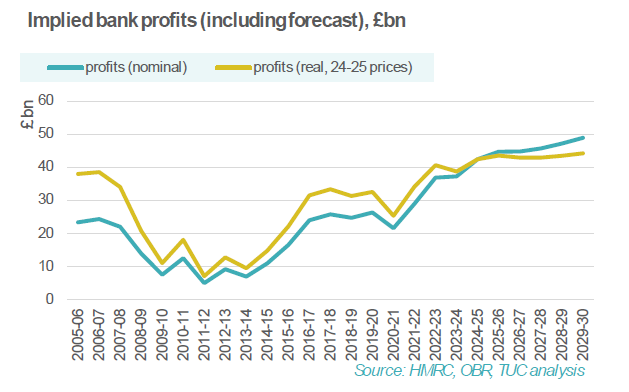

By looking at the HMRC corporation tax take 8 we can calculate the overall level of bank profits. Banks made £37bn of profit in 2023-24, up by 41% from £26.3bn in 2019-20. In real terms the increase was 19% despite significant inflation. More recent figures from Positive Money 9 show the big four banks 10 made £45.9bn profits in 2024 and £24.1bn in just the first half of 2025. Profits have risen significantly from pre-pandemic levels and OBR forecasts shows that profits will remain high over coming years.

Astonishingly, while many are dealing with hardship, banks are making even more money than they were in the bonanza years ahead of the global financial crisis.

- 8 HMRC Corporation Tax Statistics https://www.gov.uk/government/collections/analyses-of-corporation-tax-receipts-and-liabilities

- 9 Positive Money (2025) How the government could reclaim the huge payouts to banks https://positivemoney.org/uk/update/how-the-government-could-reclaim-the-huge-payouts-to-banks/

- 10 HSBC, Barclays, Lloyds and NatWest

Overall bank tax take

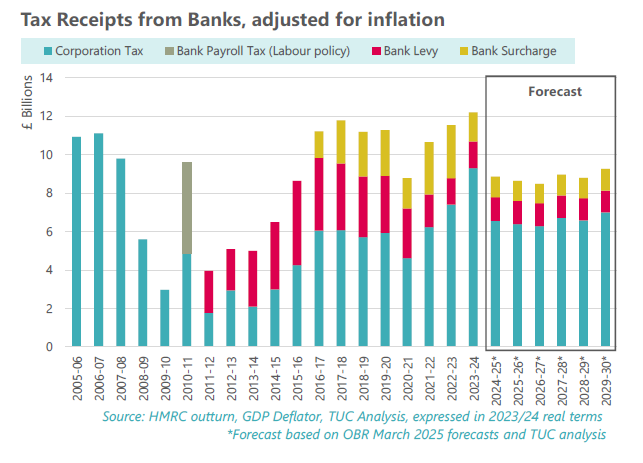

Following the financial crisis, tax revenues from banks fell (chart below). The exception to this was 2010-11 when Labour implemented a one-off tax which collected £4.7 billion 11 in real terms from bankers’ bonuses. In the first tax year after the 2010 election, bank taxation totalled £4 billion in real terms. Tax receipts then rose steadily to £11.8 billion in 2017/18 before levelling off. The three main taxes on banks collected £12.2 billion in 2023/24 despite large increases in profits. This was the first year which saw the Bank Surcharge slashed to just 3%.

- 11 £3.4 billion in nominal terms

Policy options

The TUC is calling for a windfall tax on bank profits. This can be done by raising the Bank Surcharge which directly taxes bank profits as an addition to corporation tax. In 2021 the previous government announced a cut in the Bank Surcharge from 8% to 3%. This came into effect in April 2023. At the time decisions were made about cuts in the Bank Surcharge there was no indication that banks were going to make huge windfall profits in the following years.

Below are some options for increasing the Bank Surcharge to raise additional revenue from banks:

Put the Bank Surcharge back to 8% reversing the recent cut in full

The Chancellor could reverse the bank surcharge cut. This would increase the rate from 3% back to 8%. It would raise an additional £1.9bn in 2026/26 and £8bn over four years.

Raise the Bank Surcharge to 16%

A second option would be to raise the bank surcharge to 16%, double the original rate of the surcharge. This would raise 4.9bn in 2026/27 and £20.8bn over four years.

Windfall tax surcharge of 35%

This is a proposal the TUC has previously put forward. 12 It has also been suggested by Positive Money.13 It would raise the bank surcharge to 35% in line with the Energy Profits Levy under the Conservatives. Like the windfall tax on energy profits, this would be paid on top of corporation tax. It could raise £12bn in 2026/27 and £51.2bn in total over four years.

Appendix

Recent history of bank taxation

Since 2015 the two taxes targeted specifically at banks have been slashed, although there have been wider increases in corporation tax across the economy.

The two targeted bank taxes are the bank levy and bank surcharge. Since cuts were announced to both taxes by the previous government, banks have significantly increased their profits. This is largely because of raised interest rates which were not forecast when these tax cuts were planned. Despite higher profits, banks paid £0.2 billion less tax in real terms in 2022/23 than in 2017/18 when the tax take peaked.

The main taxes paid by banks are currently corporation tax, the bank surcharge and the bank levy.

- The previous government cut the bank surcharge (tax on profits) from 8% to 3% in April 2023.

– The government introduced this cut to partially offset the increase in corporation tax from 19% to 25% that took effect in April 2023.

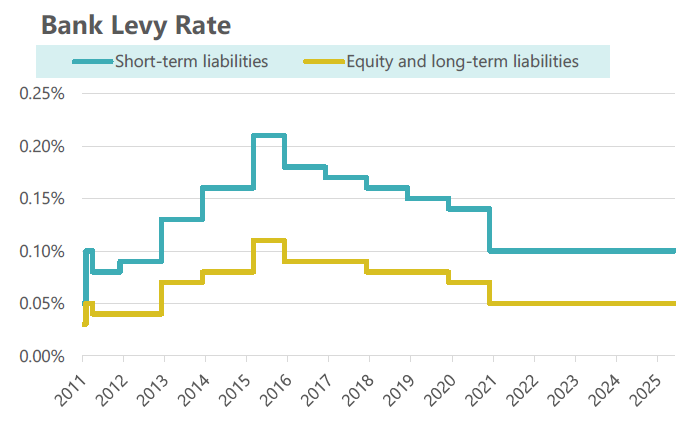

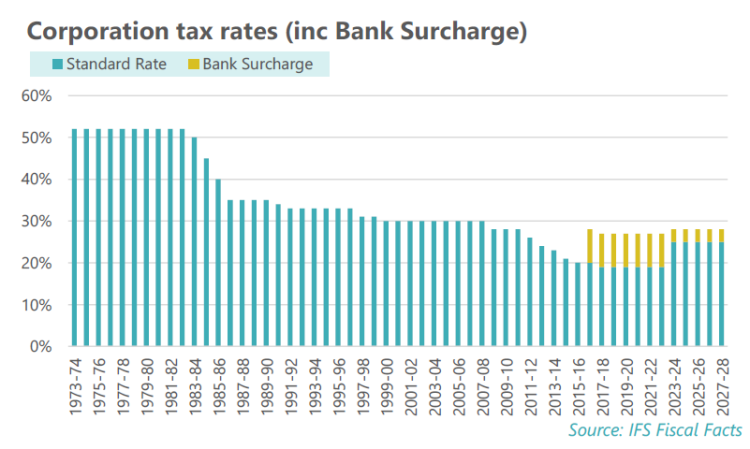

– As a result, the total corporation tax rate on bank profits increased from 27% to 28%. This is still below historic levels which existed before the financial crisis. It is also worth noting that banks only received a 1 percentage point increase to their tax rates, while other businesses had a much bigger 6 percentage point increase to their total corporation tax rates. - The previous government also steadily cut the bank levy (tax on balance sheets) since 2015.

– In 2015 the short-term rate was 0.21% and the long-term rate was 0.11%. These have been more than halved to 0.10% and 0.05% respectively, between 2015 and 2021.

The House of Commons Library summarises the recent history of bank taxation:

“While banks and financial institutions are liable to pay corporation tax on their profits, as other companies, three new taxes have been introduced on the banking sector following the financial crisis in 2008:

- In December 2009 the Labour Government introduced a new bank payroll tax: a special one-off levy of 50% on any individual discretionary bonus above £25,000 to be paid by the bank, not the bank employee.

- In January 2011 the Coalition Government introduced a new bank levy to the balance sheets of UK banks and building societies, and to the UK operations of banks from abroad. Over the 2010-15 Parliament the Coalition Government amended the rates of the levy several times, with a view to maintaining the yield that it had initially anticipated.

- In July 2015 the Conservative Government announced a new bank surcharge – a supplementary 8% charge payable on banking sector profits in addition to corporation tax – alongside a gradual reduction in the rate of the bank levy over the period 2016-21.

In the Spring 2021 Budget on 3 March the Chancellor, Rishi Sunak, announced an increase in the rate of corporation tax from 19% to 25% from April 2023, as part of a series of reforms to corporate taxation. On 27 October [2021] the then Chancellor presented the Autumn Budget 9 and Spending Review, and in his statement announced the bank surcharge would be set at 3%, so that the overall rate for corporation tax on banks will, in 2023, increase from 27% to 28%.”

Source: Taxation of Banking, House of Commons Research Briefing, January 2022

- 12 TUC (2023) Bank Taxation https://www.tuc.org.uk/research-analysis/reports/bank-taxation

- 13 Positive Money (2025) Press Release https://positivemoney.org/uk/press-release/windfall-tax-on-bank-profits-could-raise-ps15bn/

Bank Levy

The bank levy was written into the Coalition agreement and set out in George Osborne’s first budget. Osborne announced, “the failures of the banks imposed a huge cost on the rest of society, so I believe that it is fair and right that in future banks should make a more appropriate contribution, reflecting the many risks that they generate.”

The bank levy came into force in 2011. It applies a charge to certain balance sheet liabilities. The levy took in tax receipts from banks even when corporation tax receipts were down due to reduced profitability after the financial crash.

The bank levy rates were gradually increased over the course of the coalition government from 2010 to 2015. The various reasons given for these increases include: to maintain the overall £2 billion yield from this tax, to offset cuts to corporation tax rates across the wider economy, and “as our banking sector becomes more profitable again … it can make a bigger contribution to the repair of our public finances.” 14

After the 2015 election Osborne announced that the levy would be reduced in scope and the rates would be reduced gradually from 2016 to 2021. This would be done alongside the introduction of a bank surcharge which would more than offset the cost to the exchequer of the reductions in the levy.

As a result the bank levy rates are now less than half of what they were at their peak. In 2015 the short-term rate was 0.21% and the long-term rate was 0.11%. The rates have been more than halved to 0.10% and 0.05% respectively.

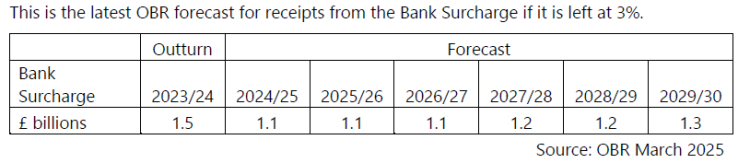

The bank levy is now forecast to stay at these rates. The OBR forecasts receipts of £1.3 billion a year from the levy over the next five years.

- 14 George Osborne, House of Commons debate, 18 March 2015

Bank Surcharge

Introduction by Osborne, 2015

The bank surcharge was announced in the first budget after the 2015 election. Osborne introduced the surcharge at the same time as plans to reduce the bank levy in scope and level over six years. The bank surcharge was set as an additional 8% tax on bank profits paid on top of corporation tax.

In his Budget speech in July 2015 Osborne said, “I will, over the next six years, gradually reduce the bank levy rate, and after that make sure it no longer applies to worldwide balance sheets. But to maintain a fair contribution from the banks, I will introduce a new 8% surcharge on bank profits from 1 January next year.”

The shift away from the bank levy to the new bank surcharge was intended to bring in comparable revenue but shifted the balance of contributions from different banks. The bank levy took a lot of its receipts from large and international banks such as HSBC but the bank surcharge spread the contributions more evenly across UK banks.

Cut by Sunak, 2021

In 2021 Chancellor Rishi Sunak announced a reduction of the surcharge to 3%. This tax cut came into force from April 2023. Sunak’s cut to the bank surcharge were accompanied with an increase to the headline corporation tax rate across the economy but no reversal to the cuts in the bank levy.

Sunak initially announced that the headline corporation tax rate would increase from 19% to 25% in his Spring 2021 Budget. The Budget announced that there would also be a review of the bank surcharge as the increased corporation tax rate would combine with the 8% surcharge rate to create an overall 33% tax rate on profits. The Budget report argued this would “make UK taxation of banks uncompetitive”.

In the October 2021 Autumn Budget, Sunak announced that the bank surcharge would be cut to 3%. The overall rate of tax on bank profits would therefore only increase from 27% to 28%.

However, the new overall tax 28% rate on bank profits was just a return to 2010 levels. The headline corporation tax rate was cut significantly by the Conservative government and the bank surcharge maintained rather than increased overall tax rates for bank profits.

Non-banking businesses saw their corporation tax rate increase by 6 percentage points, while banks only had a rise of 1 percentage point.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox