Pay growth falls again as workers continue to suffer

Today’s labour market statistics fly in the face of the Bank of England’s predictions that pay growth would continue to rise this year.

Instead, they show that wage growth has slowed for the second month in a row.

The figures are another nail in the coffin for the theory that low employment must lead to higher wages.

In fact, the exact opposite is happening – low wages and poor working conditions are enabling bosses to take on more workers rather than to improve the way they work.

Working people have endured years of low pay and rising prices because ministers and economists promised light at the end of the tunnel.

It’s time for a different approach – one that includes higher pay, more spending on public services and increased investment in the UK economy.

What’s in the figures?

Six months ago, the Bank of England reassured us that “the firming of shorter-term measures of wage growth in recent quarters…suggests pay growth will rise further in response to the tightening labour market”. (Monetary Policy Summary, Inflation Report, February 2018)

But it turns out that just as the ink was drying on that report, pay growth was about to fall rather than rise.

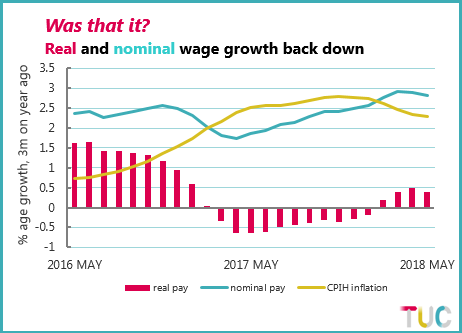

According to the latest figures, wage growth slowed to 2.7 per cent in May 2018 from 2.8 per cent in April – the second month in a row that this has happened:

While nominal pay growth remains above inflation, the gap has also narrowed.

And real pay growth has taken another dive at a time when any real pay revival already looked decidedly shaky.

So what’s going on?

The fall in wage growth can perhaps be explained by the use ofr shorter-term wage growth measures referred to in the quote above.

A short-term measure looks at wage inflation over a shorter period than a year – here comparing the latest three months with the previous three months.

That figure is then multiplied by four to change a quarterly figure to an annual figure.

While longer-period measures can be slow to react to recent developments in the economy, the trouble with shorter-term measures is that they can be erratic and misleading.

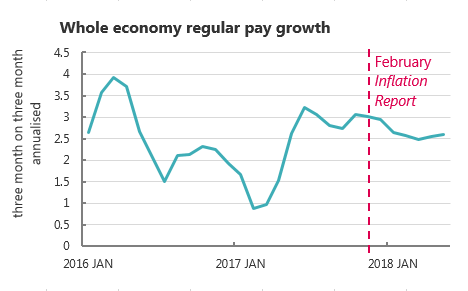

So let’s look at how the shorter-term measure now looks:

The chart above shows that it’s fallen from 3 per cent when the Bank published its report to just above 2.5 per cent over the last three months.

While the inherent volatility of the short-term measure requires caution, there is no upside here.

And industry figures also show 2.5% as the norm across much of the economy, excepting a surge in pay in construction (to 5.6% in the latest month) and a reversal in the public sector (to 2.2%).

History repeating

This is not the first time this has happened.

In 2014, Bank of England Governor Mark Carney told the TUC Congress that wages should start rising in real terms "around the middle of next year" and "accelerate" afterwards” .

They did rise in the first half of 2015, but then decelerated afterwards.

So why are the experts repeatedly wrongfooted by events?

The trouble is that the Bank of England and others cling doggedly to the flawed theory that low unemployment always leads to higher wages.

The exact reverse is happening, yet this theory continues to drive economic policymaking.

As a result, the Bank appears committed to putting up interest rates to stem a projected wage inflation that is apparently just around the corner.

It’s time that the experts changed course and accepted that the relentless weakness in pay growth mirrors the underlying weakness in the economy following the financial crisis and the imposition of austerity.

Policymakers need to enable the economy to expand, not force it to contract.

They should act decisively to put up pay, increase spending on public services and boost investment.

When events keep proving your theory wrong, it’s time to try a different approach.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox