Inflation measures aren't boring: they matter

Inflation measures may sound like dry economics, but they have a real impact on the amount of cash in our pocket.

If economists want ordinary people to understand why this is the case, we must do more to explain how these measures work and how they differ.

Because let’s be clear: the way that inflation is calculated is something that everyone, not just economists, needs to care about.

Three choices

There are three main measures of inflation:

- Consumer Prices Index (CPI)

- Consumer Prices Index including owner occupiers’ housing costs (CPIH)

- Retail prices index (RPI)

So how do these actually work?

CPI and RPI are measured by tracking the prices of a “basket of goods”, which you’ve probably heard about already.

The basket of goods is a sample of around 700 consumer goods and services. It’s updated once a year so that new goods are added in and the stuff no one really buys any more is taken out.

This year the new arrivals were quiche and leggings, while bottles of lager from nightclubs got the chop.

The Office of National Statistics (ONS) collate price quotes from across the country for each item in the basket, but it can’t just say “some items went up in price, some went down, and the price of quiche stayed about the same”.

Instead, the ONS uses weightings and formulas to turn these price changes into an inflation figure, and it’s at this point that the differences in inflation figures emerge.

CPI and RPI differ because different formulas are used to convert individual goods prices into a top-line inflation figure.

We won’t go into detail about the formulas here, because life’s too short, but the important thing to note is that they produce different results – typically, RPI is a percentage point or so higher than CPI.

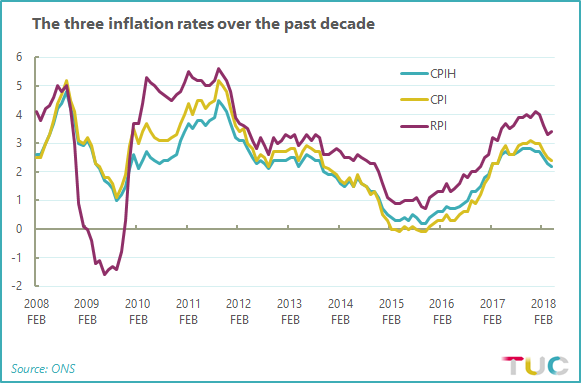

CPIH is then different from CPI because it adds in housing costs for home-owners and council tax. It’s currently lower than CPI, as you can see from the chart below:

Inflation matters

This all matters because the three measures not only vary quite a bit but are also used for different things, such as setting prices, determining pay rises, and uprating benefits.

So if you get a pay rise in line with inflation, it really matters whether your employer uses the CPIH or RPI measure. And if your annual season ticket is rising in line with inflation, you’ll pay even more if the train company uses the higher rate.

Unfortunately, the rule of thumb seems to be that organisations that take your money use the higher inflation figure, while those paying you tend to use the lower.

For example, your phone contract and rail fares probably rise by at least the rate of RPI each year. Similarly, if you rent there might be a clause in your tenancy agreement stating that your rent will rise by RPI annually.

Then there’s student loan interest for some graduates, which is calculated using the RPI figure from March of each year plus an extra three percentage points. So the current interest is an extortionate 6.3 per cent - much higher than the current rate of CPIH.

The bigger picture

The inflation measure used by individual companies is only one part of a bigger picture.

After all, it is the measure used by the ONS and the media that fundamentally frames how we view the economy as a whole.

In March 2017, the ONS switched from CPI to CPIH, arguing that the latter is a more comprehensive and reliable measure. It ditched RPI a few years back, deeming it pretty much unusable as a national statistic.

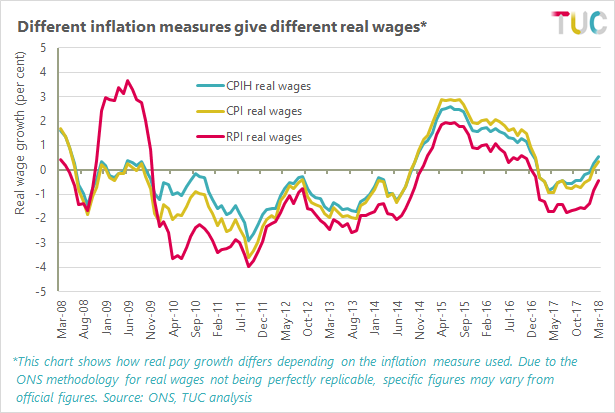

We can see the impact of switching from CPI to CPIH if we look at real wages (the wages we get paid once inflation is taken into consideration).

It’s important to do this, because a 2 per cent pay rise means very little if the leggings and quiches you buy are also 2 per cent more expensive.

Recently, we’ve celebrated the return of real-pay growth after a year of decline. But that’s only the case if CPIH or CPI is used rather than RPI.

Even then, growth is more muted if we use CPI than it is under the CPIH measure, as the following graph shows:

Similarly, in real terms, we’re being paid on average £13 less per week than we were back in 2008.

Again, this is if we use CPIH to define “real terms”. If we use CPI instead, the amount rises to around £20. That’s a difference of about £360 per year – a significant chunk of money for many working people.

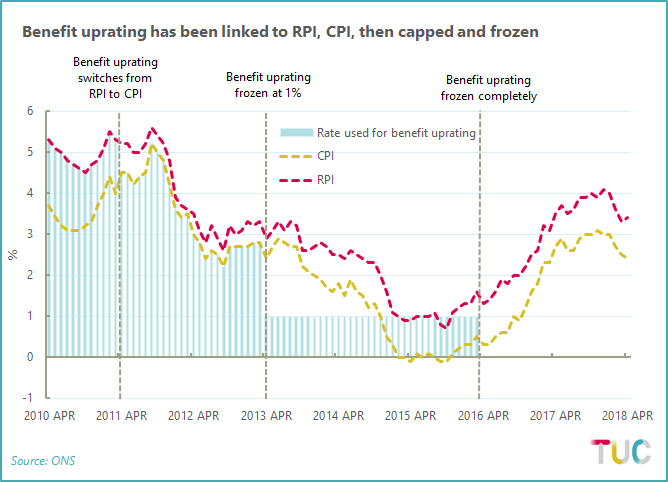

Inflation measures don’t just shape how we view the economy, they shape the decisions that ministers take.

The government is happy for RPI to be used for student loans, but less RPI-friendly when making decisions about public sector pay and benefit uprating (the amount that benefits increase by each year).

In the latter case (and with public sector pay until recently), the government abandoned inflation altogether and imposed a freeze or cap instead.

Going forward

The inconsistent use of CPI, RPI and CPIH is obviously a problem.

It’s fine to use a certain measure if you can justify your choice, but “we want to make more money from you” isn’t a justification, nor is “we want to make these stats look better”.

Consistency is also key. It seems unfair that the ONS considers the RPI so bad that it’s not even deemed a statistic, yet companies can still increase prices in line with it and refer to this as “rising prices in line with inflation”.

The ONS doesn’t have the power to tell people what measure to use, and it still rightly publishes RPI for legacy reasons such as existing pensions agreements . Yet more transparency from companies about which measure it is using and why would be a good thing.

Unfortunately, discussions around inflation are often intentionally abstract, involve too many acronyms, and make endless references to complex formulas.

The consequence of confining these important discussions to drab economic seminars is a lack of public understanding that does no one any good.

Instead, we should boil this debate down to two simple questions.

First, why do organisations use lower inflation rates when they’re paying us but a higher one when we’re paying them?

And second, how long are we going to allow them to keep doing this?

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox