The Inflation game – RPI wins in court but pensions still in danger after Carney comments

The courts have effectively sided with members of the public in a long-running dispute over how companies and governments account for price increases.

Rejecting a case brought by BT, Mr. Justice Zacaroli ruled on 19 January that the telecoms giant could not use the Consumer Prices Index (CPI) measure of inflation instead of Retail Prices Index (RPI) when determining pension payments. Due to its exclusion of owner-occupier housing costs and a different method of calculating average rises, CPI is typically lower than RPI.

But this is very much not the end of the debate, with the forthcoming White Paper on defined benefit pension schemes, which could allow employers or trustees to impose changes in inflation measurement, likely to be the next scene of battle. In the meantime, yesterday the Governor of the Bank of England has added his voice to the chorus of disapproval on RPI.

Switching to cheaper uprating

This debate is of interest far beyond the dusty corridors of the Office for National Statistics and the courtrooms. For, it has a direct impact on the cash in our pockets.

Government, in the name of austerity, and companies have developed (since 2010) a habit of choosing the inflation measures that best suit their interests. So when the state makes payments to the public, these are typically linked to CPI. For example, public sector pensions, benefits, changes to tax thresholds. But when the public pays the government, the use of (the higher) RPI is commonplace such as with the duties on alcohol and tobacco and student loans.

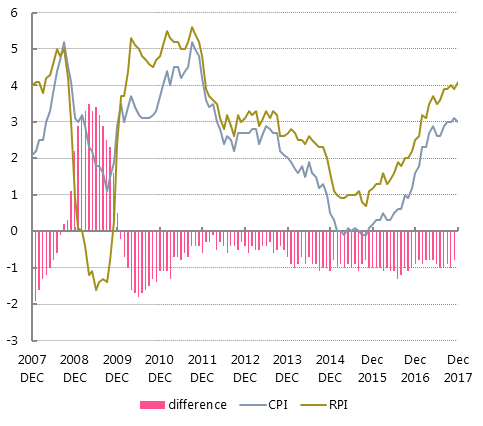

CPI v RPI annual inflation, per cent

Interestingly, companies are getting a better deal from the government than the public. Water companies use the RPI to uprate prices (though this may change). At the latest Budget, the government switched the uprating of business rates to CPI, so reducing business costs.

Companies themselves can also want to use uprating to their own advantage, in particular when it comes to pension schemes and the indexation of entitlements or payments. Here, however, the public can have some protection, depending on the wording of scheme rules. In some cases, the position is clear-cut, and companies can pick and choose among inflation measures. In other cases, the wording is such that they cannot. In others the position is ambiguous.

The BT case turned on the interpretation of the pension scheme rules which said pensions should be uprated by the RPI unless RPI ceased to be published or had “become inappropriate”.

On the first, RPI is still published. On the second, the ONS and the statistical regulator have deemed it “fundamentally flawed” (for background on this debate see TUC commentary here and here). If the ONS were right, then BT could switch the pension to CPI.

Expert witnesses queued up on each side. The head of the Institute for Fiscal Studies and ubiquitous economics commentator Paul Johnson argued the ONS position, having himself played a key part in the development that position though the ‘Johnson review’ of consumer price statistics (see here). On the other side was former FT Statistics Editor and member of the Council of the Royal Statistical Society Simon Briscoe. In December, trade union Prospect, which has campaigned hard on this issue, reported his statement:

Mr Briscoe argued that the significance of RPI's reported flaws was overstated and applied more to its use for macro-economic purposes than as a measure of inflation as experienced by pensioners. He concluded that RPI is the best index available to measure inflation as experienced by pensioners of occupational pension schemes.

In the end Mr Justice Zacaroli sided with Simon Briscoe and found that the RPI had not become inappropriate.

On the Professional Pensions website, Mr Justice Zacaroli’s remarks taking aim at the government’s general approach are reported:

This mirrors exactly the view of the TUC. Based on technical arguments that have been championed in particular by UNISON, we very much agree with Briscoe that the flaws of the RPI are overstated.

(Slaughter and May, the law firm that acted for BT scheme trustees provides more detail here.)

This is a big deal. The judgment not only protects the retirement income of pensioners, but is also important to those of us who consider the attack on the RPI ill-judged and insufficiently robust. But the battle to ensure inflation measures operate in the public interest continues.

The Treasury Select Committee and the coming government proposals on private pensions

Presumably coincidentally, also on 19 January the Treasury Select Committee published commentary on the government’s decision to switch the uprating of business rates to CPI. More generally they argued:

The RPI is no longer a National Statistic and its deficiencies are numerous. The Government has acknowledged that using the statistically-flawed RPI to uprate the Business Rates multiplier is unfair on businesses. Having acknowledged this, the Government should now discontinue the use of RPI for any indexation purpose where legally possible.

Trade magazine Professional Pensions, for its part, argued that the BT judgment

… will add to pressure on the government to provide a statutory override of indexation for occupational defined benefit (DB) pension schemes. This is particularly acute where many have found they are unable to swap to the generally lower Consumer Prices Index (CPI) because of the precise wording of their rules.

Effectively the government is being asked to remove legal protections that prevent members’ accrued benefits being watered down.

A coming flashpoint is the (possibly spring) publication by the Department for Work and Pensions of a “White Paper on Security and Sustainability in Defined Benefit Pension Schemes”. In the Green paper issued at the start of 2017 the government tackled this this argument, but was cautious:

274. However, allowing all schemes to move from RPI to CPI or to move to statutory minimum indexation only (including removing any pre April 1997 indexation) would have significant impact on members’ benefits. CPI has been lower than RPI in 22 years out of the last 27 years (and in 9 years, out of the last 10 years) up to 2015, and so would in all likelihood represent a reduction in members’ benefits. Many schemes also pay indexation above the statutory minimum.

The TUC position was clear:

“There is no case for permitting cuts to members’ benefits without their consent,” we said. “This includes changes to rates of indexation and revaluation. Giving schemes with RPI inflation uprating in their rules the ability to switch to CPI for uprating without member consent, would cost an average affected DB scheme member £20,000 over their retirement.”

In short, if you want members to accept a lower level of inflation increase than they were promised, then you have to make that case to them.

Maybe Mark Carney’s statement at the Treasury Select Committee that the RPI has “known errors” will help swing the balance. But it is not clear that the public would agree with his statement reported in today’s Financial Times that “most would acknowledge [that it] has no merit”. And, as the BT case showed, some experts disagree too.

In the meantime, trade unions will stand firm against attempts to fix the rules of the inflation game.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox