Have the past 35 years really been as great as Philip Hammond says?

While others have commented on the political merits and otherwise of the Chancellor’s speech to the Conservative Party Conference this week, I want to contest the underlying economic substance.

The narrative runs that over the past 35 years the secrets of prosperity have been unlocked. (The Chancellor recognises that there have been significant differences in approach over the same 35 years, which he describes as varying degrees of “enthusiasm”.) But woe betide anyone who plans to depart substantively from this underlying doctrine.

But the data (helpfully made readily available by the Bank of England) suggest the opposite. Over the past 35 years, prosperity has increasingly slipped through our fingers. Real earnings, economic growth, unemployment, inequality and even the very conventional measures of productivity and the public finances all performed worse over the past 35 years than they did in the ‘bad old’ 35 years before that.

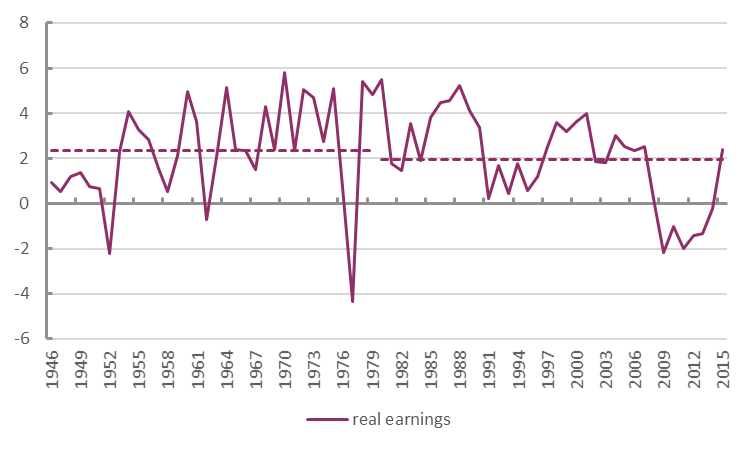

Exhibit A: Real earnings

The speech is surprisingly thin on evidence. One of the few concrete claims (the others were an inflation figure for the UK in 1975, an inflation figure for Venezuela, and a claim around inequality: all discussed below) the Chancellor offered was the following: “35 years in which we have seen real living standards almost double in this country”. The actual figure, as discussed below, is 90 per cent.

But the question is not whether the Chancellor is being generous in his rounding up. It’s not about what living standards have done over the past 35 years, it’s about whether doubling in 35 years is better or worse than the norm.

The chart shows one crucial measure of living standards: real earnings. Earnings don’t determine all of living standards, levels of employment and social provision matter too. But they do have by far the biggest influence. Real earnings grew by 1.97% a year over the past 35 years. In contrast, the previous 35 years saw an annual growth rate of 2.36%.

Real earnings, % growth

(As above, the source for all data in this post is the Bank of England historical spreadsheet. Real earnings are derived as AWE deflated by the CPI. The Bank data extend to 2015, so the Chancellor’s 35 years is 1980-2015, and the 35 years before that 1945 to 1979 – which is in fact 34 years but including 1944 is not sensible.)

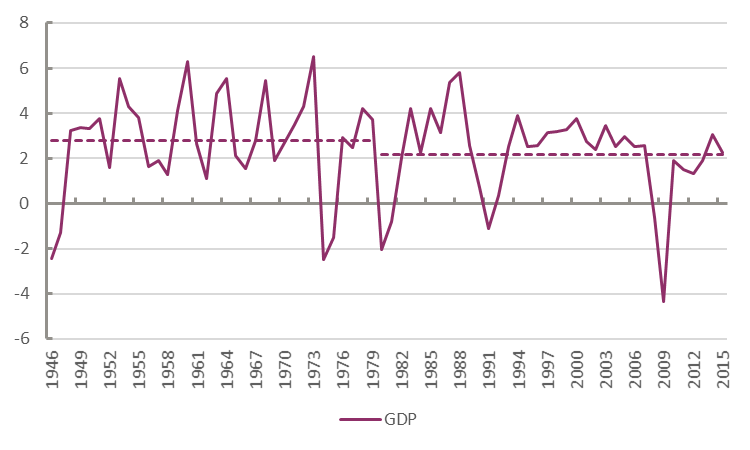

Exhibit B: Economic growth

Since 1980 GDP has grown by 2.1% a year. Ahead of 1980 it grew by 2.6% a year.

GDP, % growth

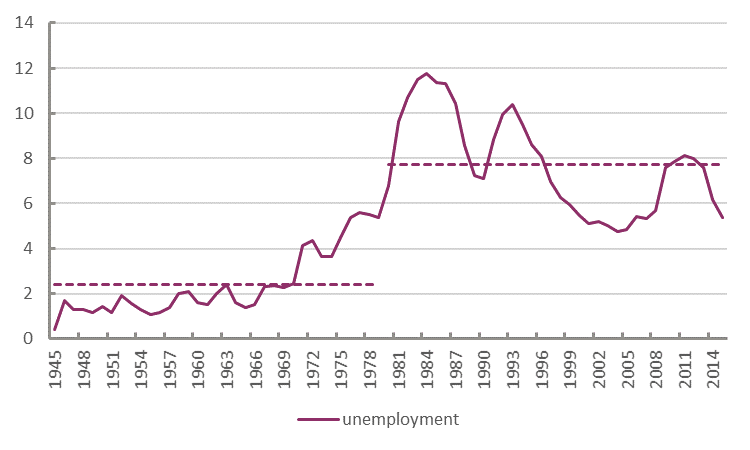

Exhibit C: Unemployment

The unemployment rate has averaged 7.7% since 1980. Up until 1980 the average was 2.4%.

Unemployment rate, %

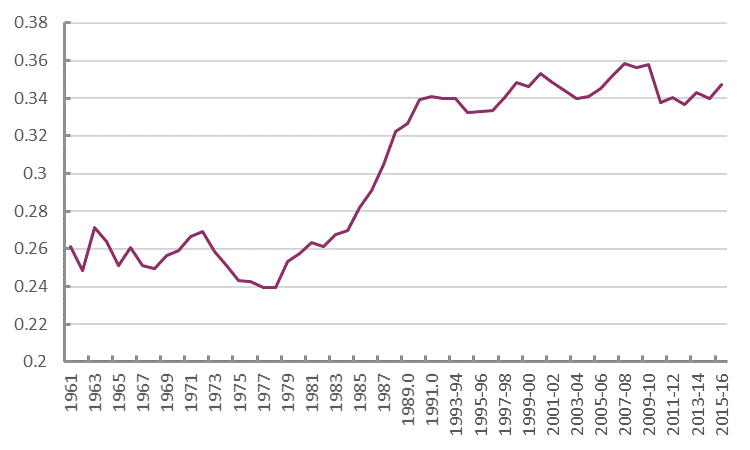

Exhibit D: Inequality

The other figure celebrated by the Chancellor was an improvement in inequality (“we can be proud that under this Conservative Government, income inequality in this country has fallen to its lowest level in over three decades”). Maybe so, but the major cause of this has been levelling down following the financial crisis, rather than an uptick in the fortunes of the bottom half of the population (see my earlier post).

On a longer view (as the IFS figures below show) the pre-1980 years were characterised by improvements in inequality to a low point at the end of the 1970s; over the post-1980 years, the position was decisively reversed.

Gini coefficient (GB)

Source: IFS

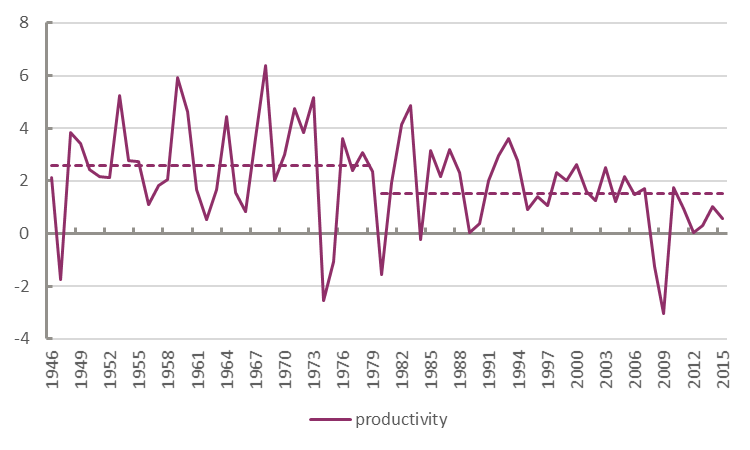

Exhibit E: Productivity

Commentators are expending vast energies on (unsuccessfully) explaining why productivity outcomes have been so poor in recent years. Why not ask instead why they used to be so much better? Since 1980 productivity (per worker) has grown by 1.5% a year; ahead of 1980, it grew by 2.6% a year.

Output per worker, % growth

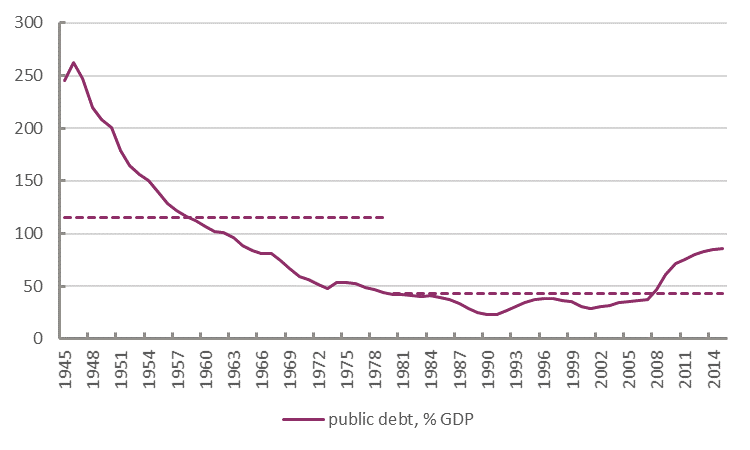

Exhibit F: The public debt

Hardly surprisingly, public debt as a share of GDP was higher in the 35 years following the Second World War. But the key point is that it fell in every year from 1946 to 1973. Over the past 35 years, the experience has been the reverse. Quantitatively: over 1945-1979 the public debt ratio fell by 5.9 ppts a year; since 1980 it has risen by 1.2 ppts a year.

Public debt, % GDP

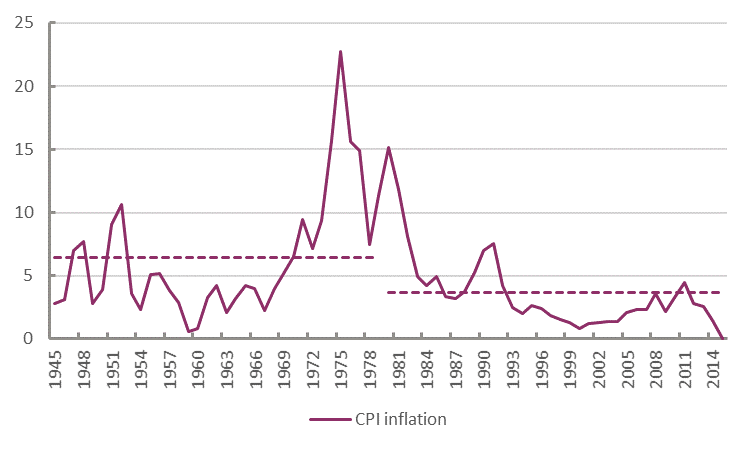

Exhibit G: Inflation

The Chancellor’s bottom line was of course the inflationary crisis of the 1970s. Here the difference is apparently clear-cut in his favour, averaging 3.6% since and 6.4% before 1980. There are, however, plenty of ‘buts’. If the 70s are removed, the pre-1980 average at 4.1% is not greatly different to the post-80 outcome (and of course the latter is assisted by the deflationary tendencies since the financial crisis).

CPI inflation, %

And there were far more economic factors at play in the 1970s than usually recognised:

- global inflationary pressures generated by the Vietnam war,

- excesses following domestic credit liberalisation under the Bank of England’s ‘competition and credit control’ (dubbed – ‘all competition, no control’), and

- wider domestic policy excess under the ‘Barber boom’ (Barber was Chancellor to Edward Heath’s Conservative government – note from the GDP chart that they scored the record annual GDP growth figure in 1973).

But even leaving this aside, it is seriously unbalanced to assess everything solely on inflation outcomes. The winner of a football match is not the team that commits the fewest fouls.

More importantly, with the financial crisis of 2007-08 and the disastrous aftermath, all bets on the right model for the economy should now be off.

Even if inflation was the inevitable result of the pre-1980 years, the charge could now be that private debt deflation was likewise for those after 1980.

But the real point is that it is time for a considered and impartial reappraisal of post-war policy – and how we can learn from it. Not for crude and tired mudslinging around the market and the state.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox