Bleak global economic outlook does not bode well for workers

Next week in his Spring Statement, the Chancellor will be reporting on the UK economy. Yesterday the OECD offered their assessment of the world economy : “It does not look very good”, was how Laurence Boone (OECD chief economist) put it.

The Chancellor should take note on policy response: “believe me this is urgent”. Yet the OECD proposed action is hamstrung by still requiring austerity for most countries. Let us hope this is not the case for the Chancellor next week.

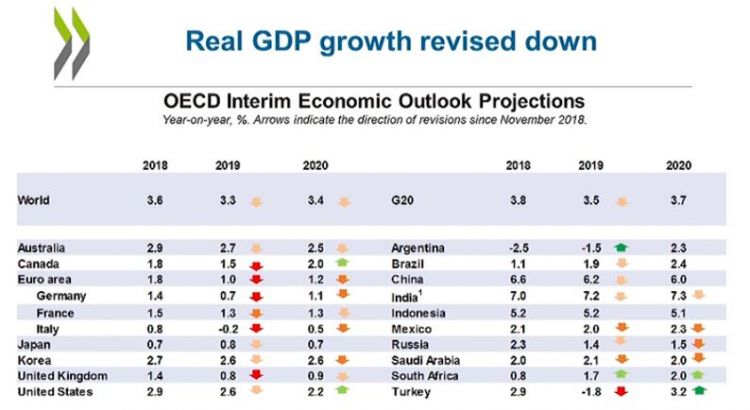

- Growth

Across the board reductions in growth forecasts are on the table below (the use of a new dark red arrow to distinguish ‘sharp reductions’ was noted). Much of the discussion focussed on Europe and China, but the declines are worldwide.

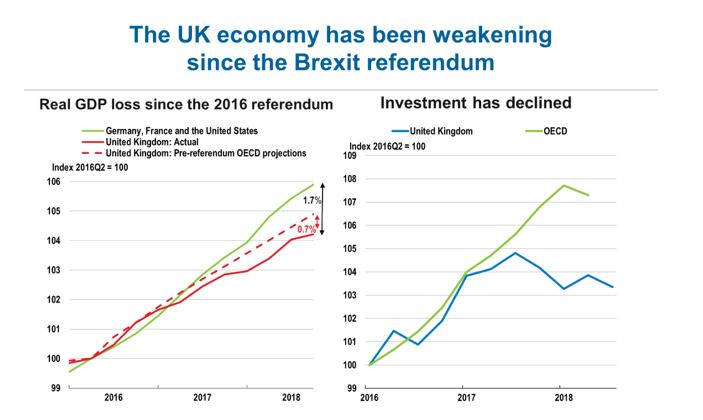

- Brexit

There’s a special mention for the UK, where no deal “remains a serious downside risk and source of uncertainty in the near term”. Charts show UK GDP weakness relative to like economies (left) and investment weakness relative to OECD as a whole (right).

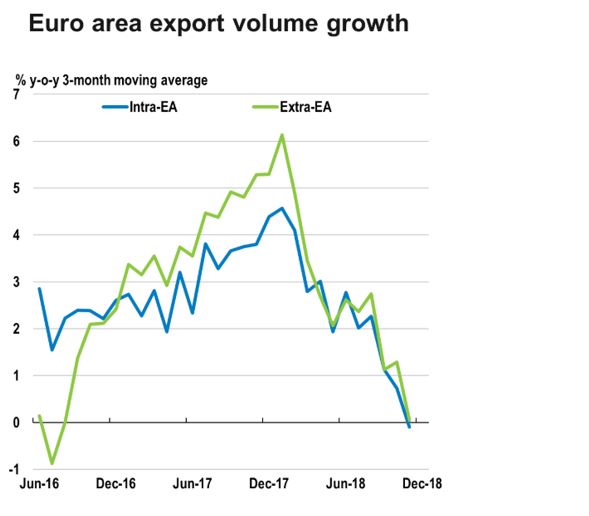

- Trade

Global trade has slumped – the chart below shows EU export growth. Boone gave an idea of linkages involved, with China a key market for German exports (affecting exports ‘extra the EuroArea’), and Germany a key market for other EU countries (affecting ‘Intra-EA’). Obviously this amounts to another prop for the UK gone.

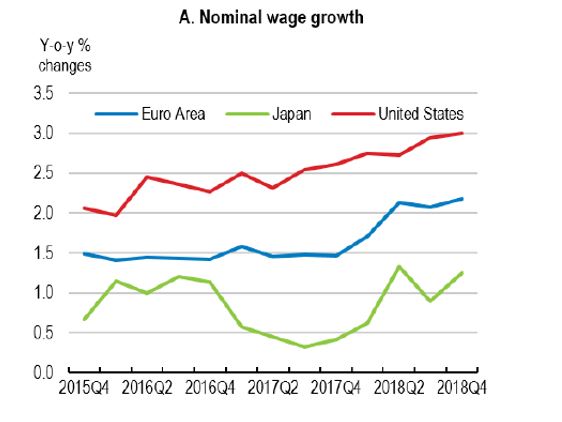

- Wage revival under threat

As the chart below shows, wage growth has been “starting to strengthen” (albeit marginally and from a very low level) and the same has been broadly true of the UK. But the sense from the wider economic story is that these more positive (or at least less negative) outcomes belong to the past. On the overall situation, Boone remarked that it was “all the more worrying that the labour market was recovering really well and wages were starting to pick up”. Overall the OECD offer only that labour markets are “resilient for now”.

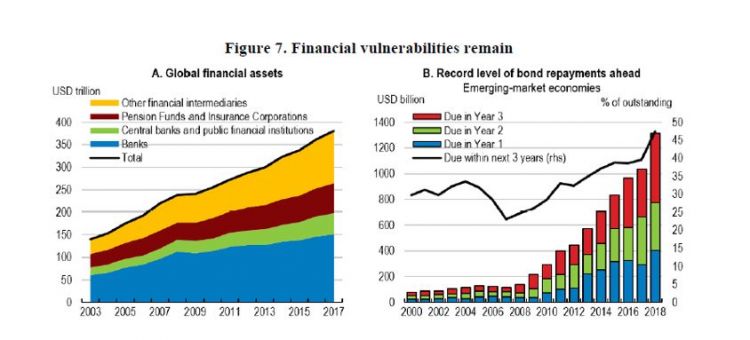

- “Significant financial vulnerabilities remain”.

The OECD continue to voice concerns about the more esoteric, but doubtless incredibly important, areas of corporate debts and asset markets. They warn that global corporate bond markets have doubled in size and the quality of debt is “continuing to decline”. On the right (debts) chart, record repayments will be due in the next three years (black line). The US$ 1 trillion market in leveraged loans is particularly vulnerable.

On the left (assets), the risks of default have shifted to “more lightly regulated non-bank financial institutions” – i.e. ‘pension funds and insurance companies’ and ‘other financial intermediaries’. For obvious reasons, this is particularly worrying.

The OECD remarks echo comments made at the latest meeting of the UK Financial Policy Committee of the Bank of England that were published on Tuesday . They warned of a “synchronised slowing in both the global and domestic economies, which could expose existing debt vulnerabilities” and a “tightening in global financial conditions in late 2018, which had the potential for a rapid change in global risk appetite”, as well as a specific concern of “continued signs of reduced demand for UK assets relative to international peers , consistent with Brexit-related uncertainty”.

- Fiscal policy imperative

Despite the seriousness of the situation, the best the OECD can do is call for countries with low public debt to spend (specifically Germany, the Netherlands, Austria, Ireland, Finland, the Slovak Republic, Slovenia and the Baltic States).

But those countries with high debt are those that suffered the most austerity. Until it is recognised that austerity policies are a key factor in the present predicament, there can be no real hope. All countries – including the UK – must up government spending. Now.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox