A Better Recovery

Measures to contain the coronavirus have shut down or reduced activity across major parts of the economy. The government has provided large-scale support for jobs and livelihoods, including the job retention scheme that is now supporting over a quarter of employees. New initiatives have been funded, including emergency hospitals and the provision of accommodation for homeless people.

Despite the scale of support, the crisis has meant an abrupt rise in unemployment and a sharp fall in GDP growth. When restrictions begin to be lifted, there is a danger that the economy gets stuck in severe recession. Over the course of lockdown, some companies have closed and others have announced major redundancy programmes. And the economy was fragile even before the pandemic hit, with excessive corporate leverage, excess in asset markets, trade tensions and uncertainties around Brexit. [1] With tax revenues falling sharply, the sum of the parts will be an increase in the deficit and the public debt.

But we should not see the economic outcomes of the lockdown as inevitable. Government action during this period has shown what is possible, and government will need to act decisively to protect against the risk of recession and even depression.

The lesson of the UK’s economic history is that investment is the most effective way to deliver growth following a recession, and to restore the public finances. We failed to learn this lesson in 2010 with devastating results. This time must be different.

The approach outlined in this report is aimed at supporting workers and businesses in the transition from lockdown, but also in the longer term to create decent work and a fairer society. Achieving this change will mean that GDP will be higher; unemployment will be lower; wages and incomes higher; and government action on climate change will stimulate innovation and create decent jobs. In turn, the higher tax revenues this enables will help government to pay off its debts. In the meantime, with the cost of borrowing at record lows, government should see all talk of austerity as a dangerous distraction from the real task at hand; to build a better economy and a fairer society.

The impact of the pandemic

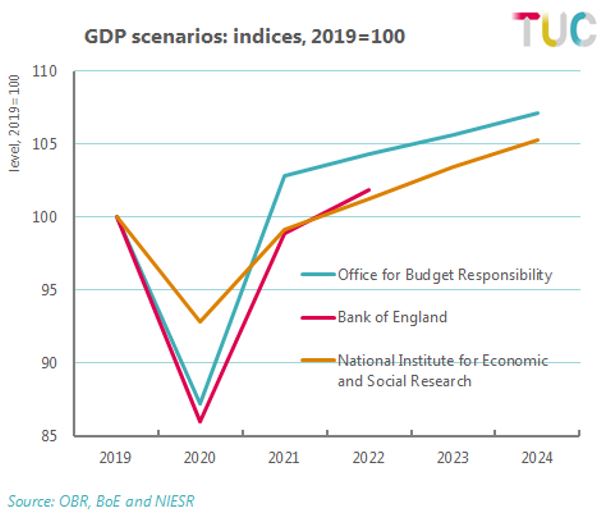

As the lockdown continues, various economists are setting out forecasts for the UK and global economy. The UK Office for Budget Responsibility (OBR) has published a ‘scenario’, which provides a starting point to assess the potential impact. [2]

At the simplest level this and other scenarios start with judgements about which industries are affected by the lockdown and to what extent, and do the same across categories of expenditure. Using this approach, for example, the OECD estimate UK output has been reduced (temporarily) by around a quarter and consumer spending by a third.

The OBR scenario shows real GDP falling by 35 per cent in the second quarter, but bouncing back quickly. Unemployment rises by more than 2 million to 10 per cent in the second quarter, and it recovers lost ground more slowly than GDP does. Average earnings take a big hit in 2020 (-7 per cent), but bounce back the following year (+18.3 per cent) and get back to (post-crisis) norms of 1-3 per cent in the following years.

These projections then translate to a reduction in government taxation revenues, projected at £130bn lower than expected at the Budget. The cost of government measures to support workers and businesses is estimated at £120bn. So, there is a sharp but temporary increase taking public borrowing to £300bn in 2020–21; this is 15 per cent of GDP, by far the highest figure outside war years.

While the increase to the deficit is a one-off, public debt rises to 95 per cent from 78 per cent of GDP in 2020-21 and is sustained at this level into the future. While borrowing rises however, the cost of servicing this borrowing is expected to fall. The Resolution Foundation show that the impact of low interest rates and a flight from risky assets is that: Despite the debt-to-GDP ratio more than doubling in the most extreme scenario, the proportion of government revenue devoted to paying debt interest actually falls below the pre-outbreak forecast under all three scenarios [modelling different courses of the pandemic]. 7

Most published scenarios are broadly consistent with the OBR view, and in general show rapid recovery and very broadly pre-crisis trends restored.

Figure 10: Comparison of GDP scenarios

Achieving the recovery

The OBR and Bank of England models shown above do not say whether the rapid recovery they forecast is contingent on government support continuing into the recovery phase. The TUC believe that the measures we set out in this report are essential steps towards delivering that recovery, and a more effective economy.

A changed economic model is desperately needed. Even apart from the effects of austerity, the model that culminated in the global financial crisis was gravely flawed. Extreme inequalities of income and wealth, regional disparities, high levels of private debt, financial instability and repeated recessions in manufacturing were just some of the symptoms of a broken system, even before the insecurity and inequality we set out above was thrown into sharp relief.

This model saw decades of downward pressure on workers’ wages, not least through gradually undermining the strength of trade unions, lowering the level of effective demand. The importance of wages to economic conditions was made eloquently by Baron Morris of Handsworth (GS of the TGWU from 1992 to 2003) in the House of Lords debate on the 150th anniversary of the TUC:

The late Henry Ford was visiting one of his factories in Detroit. His guest for the day was the late Walter Reuther, president of the United Automobile Workers. Henry Ford was describing how he had automated the factory and boasted that the robots would not be asking for a pay rise and that he could rely on their accuracy. Walter Reuther, the trade union leader, replied,

“Yes, Henry, but they won’t be buying any of your damn cars either”

In the run up to the global financial crisis, ever-rising private debt reflected the consequence of production outstripping incomes and purchasing power (at both the national and international level). [3] Policymakers continue to interpret the global financial crisis as meaning the public were living beyond the means of the economy, but instead the economy has been operating beyond the means of the public. In the past this situation has been understood as ’over-production‘ or ’underconsumption’. A decade of austerity exacerbated the crisis, resulting in weak growth, the crises of pay and poverty, and further exacerbating private debts. Repeated failed attempts to tighten monetary policy were further indicative of a misreading of economic conditions, mistaking weak demand for weak supply-side conditions most recently when central banks backtracked from planned interest rate rises in the wake of financial market turbulence in autumn 2018.

Ahead of the pandemic there was growing recognition of the scale of global of global indebtedness, especially corporate debts – including those in emerging market economies. The Systemic Risk Council (comprised of ex-central bankers and academics) warned:

Covid-19 strikes the world at a time when too many corporations around the world are over-indebted, and after a period during which persistently favorable market conditions caused traders to take aggressive positions, exposing them and the system to spikes in volatility, let alone a collapse in asset values

The action taken by governments to manage the exceptional impact of the virus has shown that change can happen quickly. That change should build on what we have learnt from the last century of economic history.

Lessons from history: the tale of three recoveries

The great depression of the 1930s exemplifies the failure of the economic system that was constructed after the First World War. When the war ended, government spending was cut in two waves (the second infamously known as the Geddes’ Axe, after the minister responsible); interest rates were set high to reward creditors; and the sterling exchange rate was fixed high to protect and encourage overseas asset holders. The result was the most disastrous decade for the British and global economy in modern history.

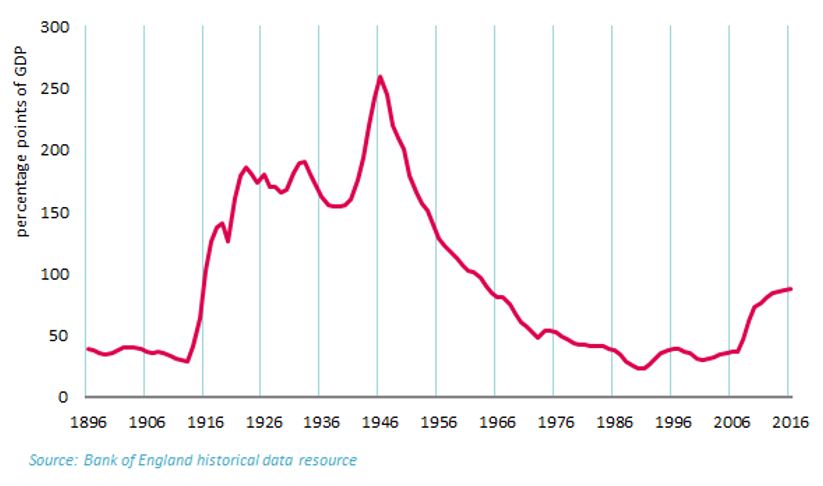

The approach after the Second World War was wholly different. Debt stood at 250 per cent of GDP; but rather than retrench, the war economy was simply repurposed and aggregate demand sustained rather than restricted. The Attlee government implemented decent social security, the NHS, built homes, extended education, supported the arts, and delivered a programme of nationalisations. The private sector was advantaged by these social advances. The unemployment rate was between one and two per cent, and wage rises were material but not inflationary (in part because of an agreement between trade unions and government that held until the Korean War). Rather than balance, the government’s books were brought into decisive surplus. Rather than stagnate, the public debt began to fall, and continued to fall for the next three decades.

Public sector net debt as percentage of GDP

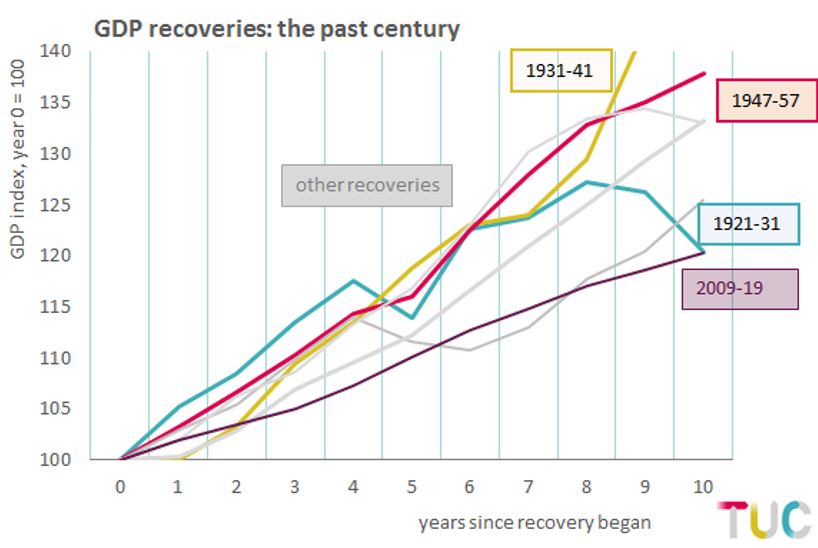

GDP recoveries over the past century

This changed economic approach and the government’s decisive programme of investment in social infrastructure led to material changes in economic performance. Many have sensed a parallel between the lockdown economy and war, but the most important parallel is with the transition to peace. Only after the Second World War were commitments to the heroic efforts of workers and soldiers honoured.

Post-financial crisis austerity was based on the same doctrine that was deployed after the First World War. GDP statistics from the trough of the recession to the present (2009-2019) show the worst recovery for two centuries. [5] It is unsurprising but very striking that the only ‘recovery’ in the past century that is in the same ballpark is the decade of after the First World War (Figure 3). Conversely, the recovery from the Second World War is at the top of the pack. (Though the expansion into the Second World War moves the 1931-41 recovery very clearly into the front.)

Just as after the First World War, austerity policies over the 2010s may have reduced the deficit, but no material dent was made to the public debt ratio and the UK went into the coronavirus crisis with the public finances in much worse shape. In October 2007, just ahead of the global financial crisis, the Treasury was looking at an outturn for public sector net borrowing in 2006-07 at 2.3 per cent of GDP. In March 2020 the comparable figure was 2.1 per cent, imperceptibly different. But in 2006-07 debt was estimated at 38.5 per cent of GDP; in 2019-20 the figure was double at 80.6 per cent (even on a favourable measure that excludes extensive subsidies to the financial sector). [6]

Even in its own terms, austerity failed, as harsh public spending cuts led to lower incomes, weakened demand, lower tax revenues and weaker economic growth. It is flawed economic systems and policies that are not affordable, even on the narrow view of the public sector finances.

Creating a fairer and more sustainable economy

Learning from our history suggests that how a better economy can be paid for is the wrong question. Instead, we should ask how to finance the transition to that better economy. And this is where coronavirus learning comes back in: given the finance was found for emergency measures through the pandemic, finance can be found to construct a new economic model.

Some may contend that the cost of borrowing will rocket and Britain will lose credibility in global markets. But public debt has steadily risen over the past decade, and in parallel interest rates have fallen to record lows. As the Financial Times put it in its succinctly titled editorial ‘Now is not the time to worry about the UK debt burden “ There is no sign of a debt crisis and little prospect of bond vigilantes singling out the UK while all major governments are running unprecedented deficits. In fact, the cost of borrowing has fallen further during this crisis .” [7] Plainly Bank of England asset purchases have been critical in this situation. The ideal must be an economic model that finally permits debt decisively to fall, and the facility to be gradually withdrawn.

Government spending to put in place a new economic model will provide necessary support to the economy as restrictions are lifted. Increases in public sector pay and employment will be quick-acting and will help rebuild confidence in the private sector. The jobs guarantee, collective bargaining, improved conditions at work, strengthening of benefits and improved pensions will also support demand as well as fostering a more positive working environment. In the medium-term just transition, lifetime learning and addressing supply chains will strengthen the economy as well as protecting the environment and improving the economic security of the UK.

With the imperative to sustain aggregate demand, questions of tax are immediately less pressing. But in the medium term, there are wider questions of who pays and how government debts are repaid. The way income and wealth are taxed in this country helps fuel inequality, and reforms to taxation are needed as supplementary means to tackling inequality, promote green growth and secure forms of employment.

This is not to underestimate the complexities as the lockdown is gradually undone. While demand will be deficient, supply will also be contained given likely restrictions on movement and operations in the workplace. The TUC is calling for a National Recovery Council, replicated at sectoral and regional level so that unions and employers can work together with government to approach strategically and handle collectively the coming challenges.

Under the Attlee government that came after world war two the economy was changed from a bad system to a better one. Large scale social and economic reform was achieved and found affordable. The same should be true today.

[1] Eg FT editorial, Saturday 2 may – “Markets Are Out of Step With Economic Reality”. www.ft.com/content/7aed2eae-8bac-11ea-9dcb-fe6871f4145a

[2] OBR (April 2020) The OBR’s coronavirus analysis https://cdn.obr.uk/The_OBRs_coronavirus_analysis.pdf

[3] TUC (2019) Getting it Right This Time: lessons from a decade of failed austerity https://www.tuc.org.uk/sites/default/files/2019-10/Gettingitrightthistime1.pdf

[5] Geoff Tily (11th February 2020) The Worst Decade For Growth in Two Centuries www.tuc.org.uk/blogs/worst-decade-growth-two-centuries

[6] Figures from the OBR historical forecasts databank https://obr.uk/data/

[7] Financial Times Editorial Board “Now is Not The Time to Worry About The UK Debt Burden” www.ft.com/content/f4512808-9517-11ea-abcd-371e24b679ed

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox