Jobs and recovery monitor - bonuses

While workers are told to exercise pay restraint the same does not appear to apply to city workers.

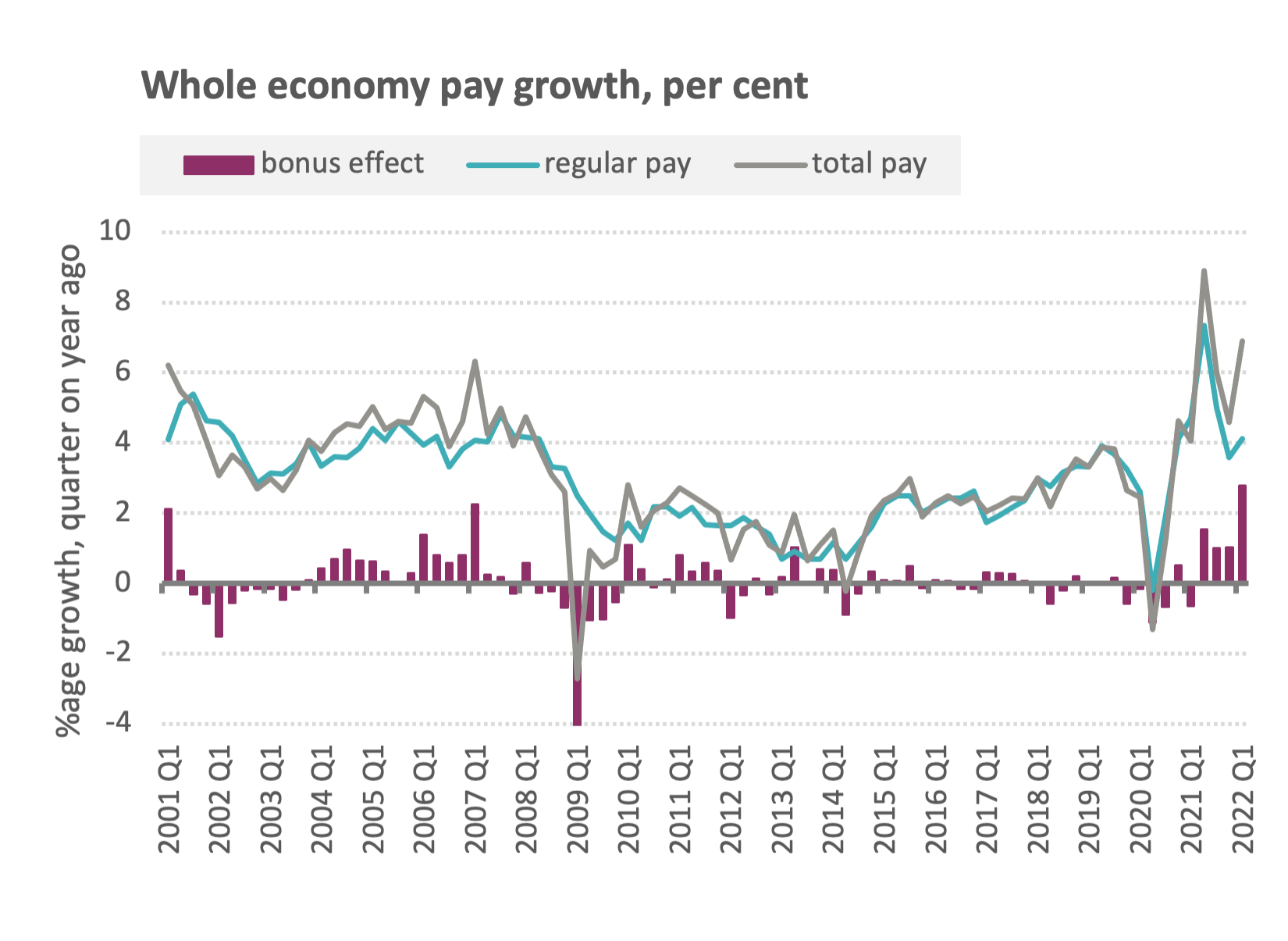

Overall in the first quarter of first quarter of 2022 pay grew by 7 per cent including bonuses and 4.2 per cent excluding bonuses.

The bonus effect of 2.8 percentage points is the largest quarterly bonus effect on records that extend back to 2000.

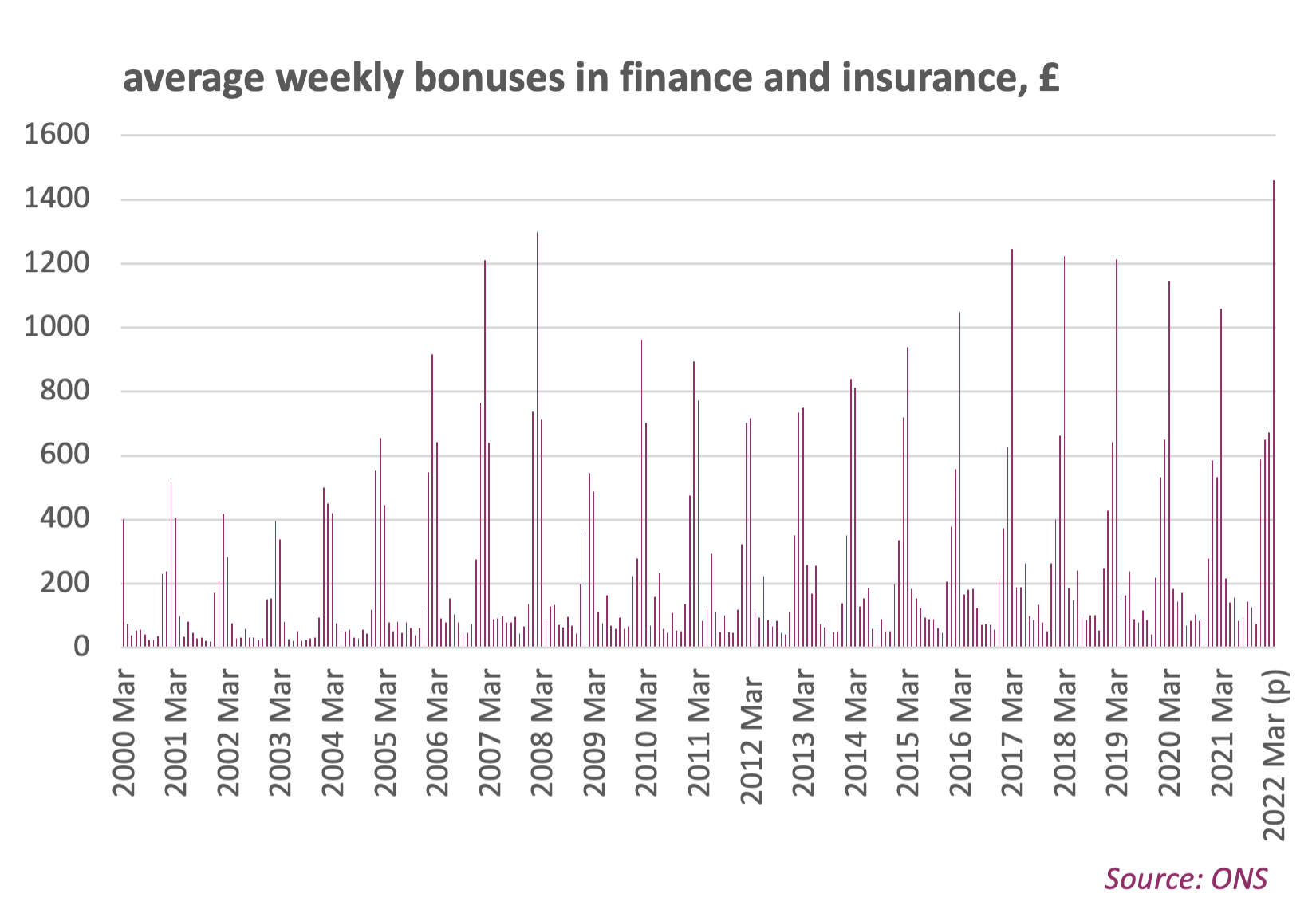

The main driver is city bonuses, in March 2022 at their highest level since records began. And over the 2021-22 financial year as a whole accounting for nearly £18bn.

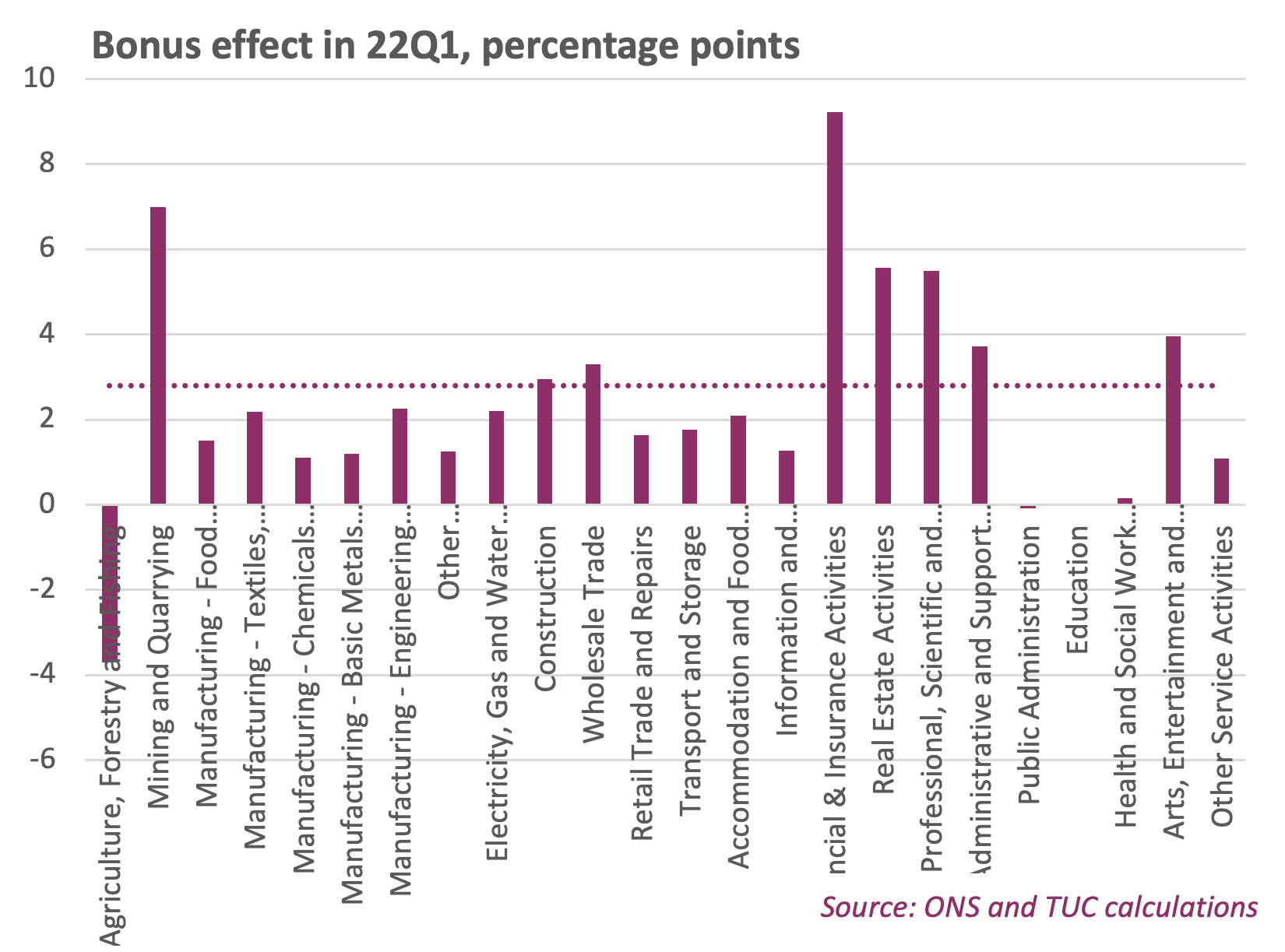

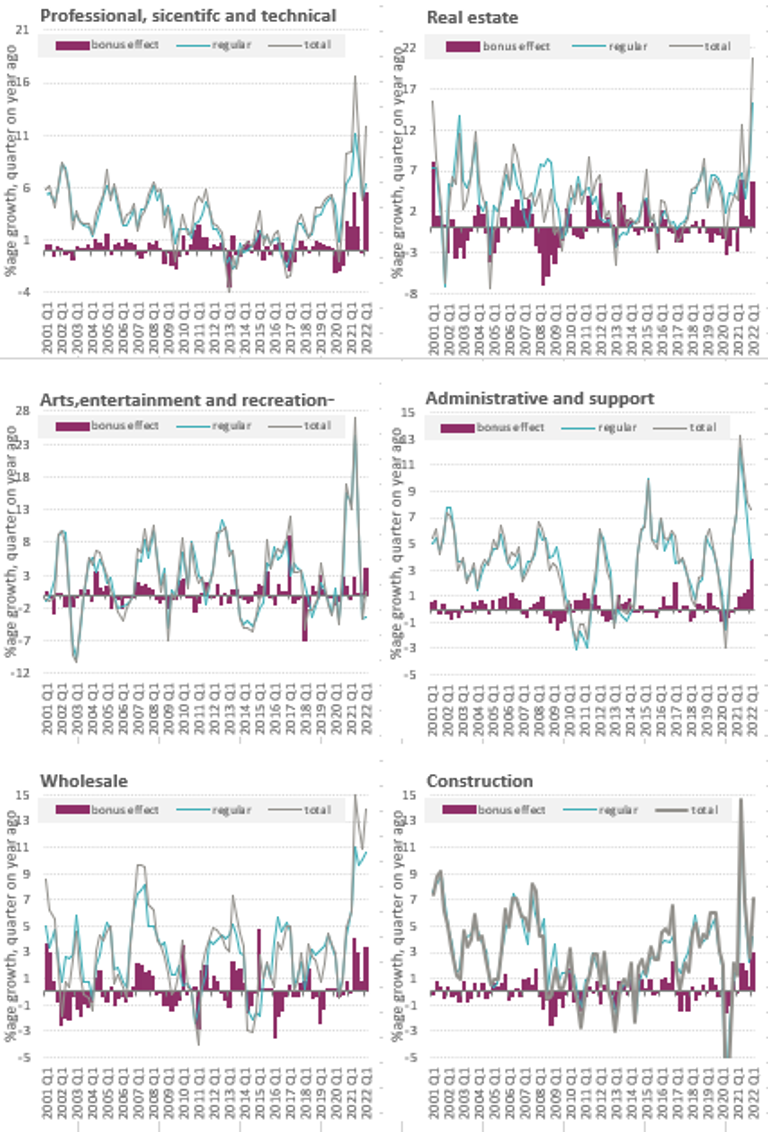

Big and in many cases record bonus effects are also evident in a number of industries, especially professional and scientific, real estate, arts and entertainment, administrative and support services and wholesale trade and construction.

While bonuses in the city are business as usual, the wider effects are likely to reflect employers seeking to reward workers without consolidating pay rises. Such inherently one-off actions are hardly consistent with the fears of a wage price spiral.

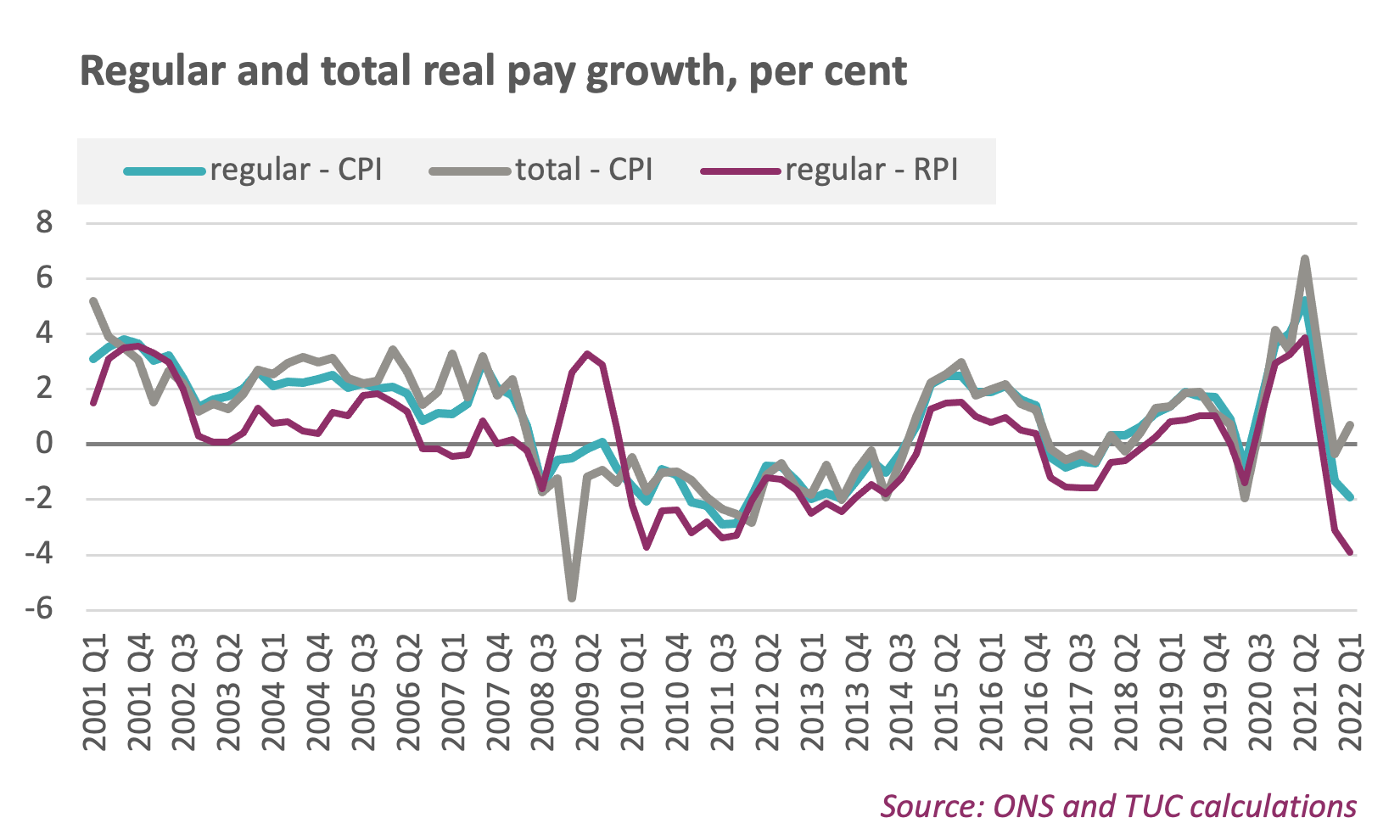

In the meantime regular pay in real terms (CPI basis) is declining by an annual rate of 1.9 per cent the worse decline since 2013. (On the RPI the real decline of 3.9 per cent is the steepest on record.)

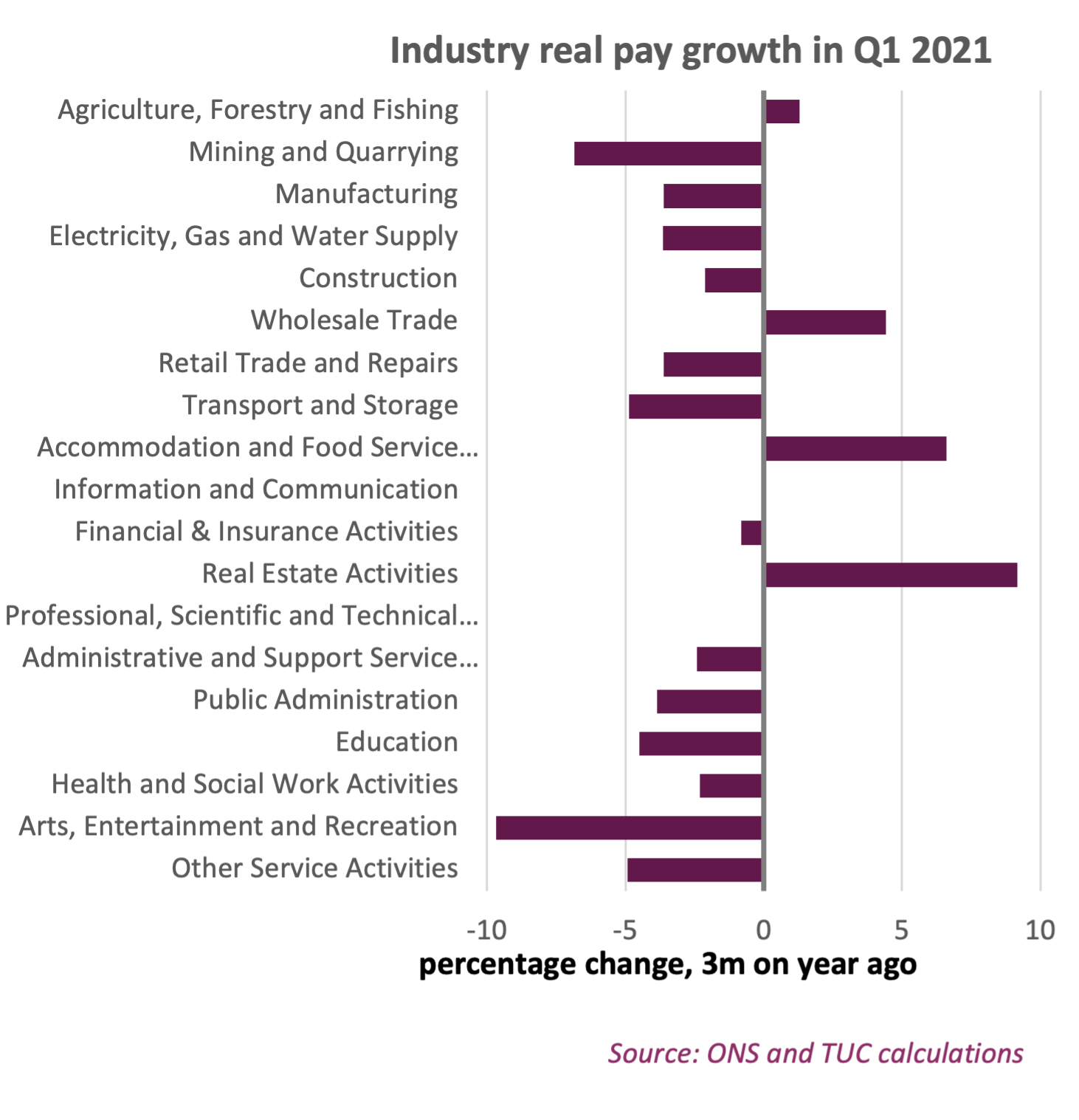

Regular pay in real terms is falling in all industries except agriculture, wholesale, accommodation and food, and real estate activities.

The TUC continue to regard the risk of recession as far greater than the risk of a wage price spiral, as rising prices eat into take home pay and further damages spending in the economy. And TUC deputy general secretary Paul Nowak reacted strongly against the governments’ accusation that higher pay for workers will push up inflation.

“These claims are nonsense. Making sure people can afford to pay their bills and put food on the table is not going to push up inflation. Inflation is being driven by rising energy costs, not pay demands. Key workers in the public sector have endured a decade of wage cuts and freezes. At a time when staff shortages are crippling frontline services this would be a hammer blow to workers’ morale.”

No claims are more ludicrous than those appealing the 1970s. With unions under attack for more than four decades, the annexe to this briefing looks at the consequent change in the labour share since the Second World War. Rather than attacking workers the government should be strengthening the position of unions so pay cuts can be resisted and spending in the economy supported.

-

Unions should have access to workplaces to tell workers about the benefits of union membership and collective bargaining (following the system in place in New Zealand).

-

Workers should have new rights to make it easier to negotiate collectively with their employer.

-

We need new fair pay agreements which allow unions to negotiate across sectors,, starting with social care.

The government needs to clamp down on greedy bonus culture by putting workers on company pay boards and introducing maximum pay ratios.

The key driver is city bonuses, but bonus payments are high in a number of industries.

Bonuses in the city

March is the key month for city bonuses, and in cash terms this year was an all-time high. Average weekly bonuses in the finance and insurance sector of £1,460 – they were previously largest in February 2008, just ahead of the global financial crisis. Compared with last year bonuses in the first quarter were up 28%, six times faster than regular pay growth of 4.2 per cent.

In monthly terms the latest figure amounts to a bonus pool of roughly £5.9bn. Over financial year 2021-22 as a whole, city bonuses were worth around £18bn.1

While the finance sector includes a broad range of workers, likely the highest paid are enjoying the lion’s share of these bonuses. However there may be an element of non-consolidated pay rises for those in less lucrative roles. Note while these figures are not in real terms, the cash amounts are relevant context when the government has announced additional support of £15bn partly funded by a windfall tax (or ‘energy profit levy’) of £5bn.

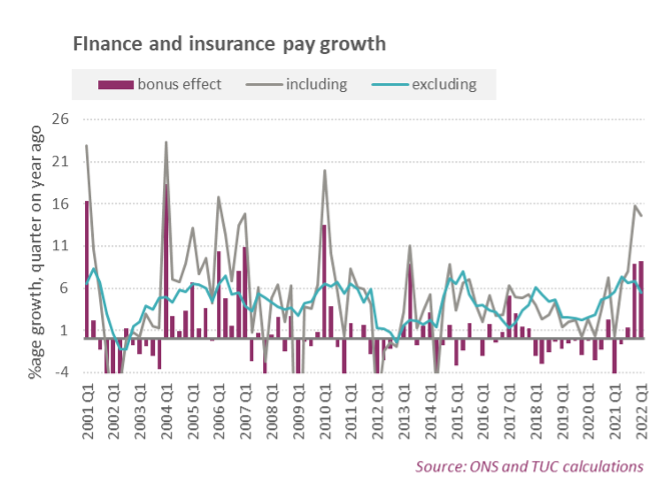

Looking at pay growth in the finance and insurance sector, in 22Q1 pay including bonuses pay grew by 14.6 per cent in 22Q1, down very marginally from 15.7 per cent in 21Q4. The bonus effect of 9.2 ppts was the highest since 13.5 ppts in 2010Q1; though massive bonus effects were common before the global financial crisis and higher than the latest figure in each of 2001, 2004, 2006 and 2007.

- 1 Using the LFS employees measure and adjusting with the employment weight for the finance and insurance industry to get 930,000 employees, and multiplying by £1,460 adjusted to a monthly basis by 52/12; and then correspondingly for the annual figure.

Bonuses in other industries

As with the headline pay figures, high bonuses were a feature in a number of industries – see first chart below for 22Q1 effects and then the selection of detailed charts. Apart from finance (as above) and mining and quarrying (which is very small) large bonus effects were a feature across the following industries:

- Professional, scientific and technical (5.5 ppts) where there has been a big bonus effect throughout the pandemic and the same peak once before in 21Q2. But ahead of the pandemic bonus effects much smaller, with the peak at only 2.9 ppts in May 2011.

- Real estate where there has again been a big bonus effect through the pandemic related to the surge in house price growth; episodes of high bonuses are not unusual but bigger effects have come only in 2021Q2 and 2001Q1.

- The bonus effect of 3.9 ppts in arts and entertainment bonus is the second highest quarterly figure on record, with the peak of 9 ppts in Q1 2017.

- In administrative and support services the bonus effect of 3.7 ppts is an all-time high by a long way, previously the peak was 2.0 ppts in 2017 Q1.

- The wholesale trade bonus effect of 3.3 ppts while high has been higher on several occasions (2001, 2010, 2015, 2021)

- The construction bonus effect of 2.9 ppts is an all-time high

- While bonuses in accommodation and food were a little lower, the peak in the current quarter of 2.1 ppts is way above the previous peak of 1.5 ppts and a low level of bonuses normally.

Overall some of these industries are well paid, but the analysis supports the evidence cited by the Bank of England’s ‘agents of firms using “mid-year top-ups to pay settlements or one-off bonuses to compensate workers for higher inflation and to retain staff, especially in sectors where there was strong demand for skills”.2

Headline pay growth and inflation

The actual impact for households depends on both pay and inflation. The Bank of England are now warning inflation will peak slightly above 10 per cent in 2022Q4 (MPR, p. 5). In 2022Q1 CPI inflation was 6.1 per cent and RPI inflation 8.4 per cent.

Again bonuses mask the underlying position. For real regular pay, annual growth fell to -1.9 per cent in 22Q1 from -1.3 per cent in 21Q4. For real total pay, annual growth rose a little to 0.7 per cent from -0.3 per cent. The decline in real regular pay was the steepest since 2013Q3 (-2 per cent). On an RPI basis real regular pay fell 3.9 per cent, the steepest decline on record.

- 2Bank of England, Monetary Policy Report, May 2022 [MPR] p. 80; ‘UK employers turn to bonuses to avoid inflationary pay deals’, Financial Times, 12 May 2022.

Industry story

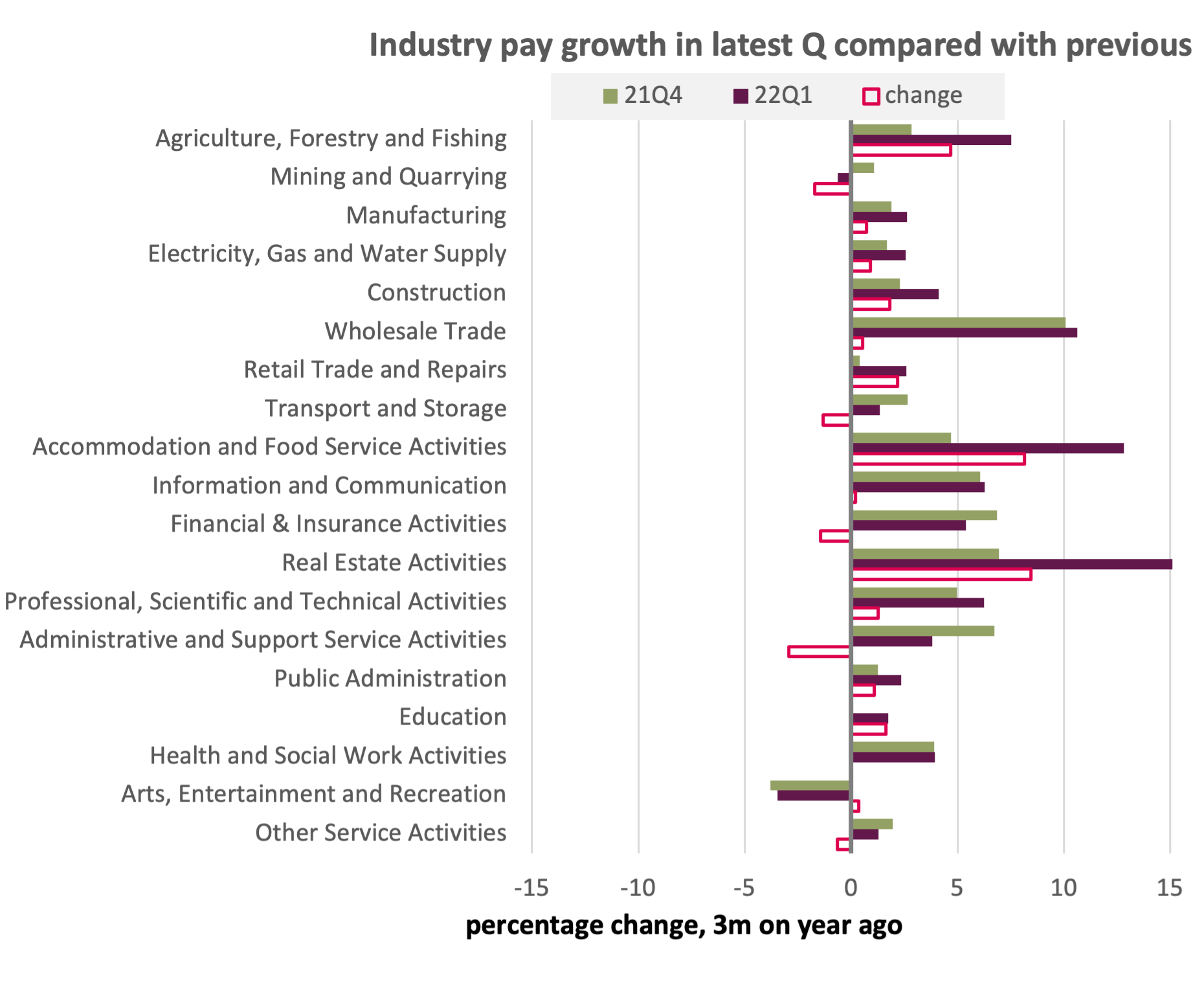

Beyond the headlines, figures by industry show high and rapidly rising pay growth still the exception rather than the rule.

The chart below shows regular pay growth in 22Q1 compared with 21Q4. For the majority of industries (11 of 19) pay growth is still below four per cent. Pay is both high and rising in only a handful of sectors: agriculture, accommodation and food services and real estate activities.

The policy debate

Even the Bank of England recognise continuing risks, with Governor Bailey conceding "We are now walking a very tight line between tackling inflation and the output effects of the real income shock, and the risk that that could create a recession and pushes too far down in terms of inflation …".3

At the Treasury Committee Bailey and his colleagues repeatedly stated that the labour market accounted for only 20 per cent of the above target inflation,4 and the Bank have long emphasised the inability of domestic action to deal with a global cost inflation. The TUC has said from the start that the risk of a wage price spiral is much lower than the risk of recession. The Bank seem now to suggest that they are proceeding with caution, but the argument for caution is more an argument to not raise rates.

There is no wage price spiral. Regular pay growth is weak in many industries, with high pay growth the exception not the rule. High bonuses further exemplify the ability of firms still not to reward workers properly with consolidated and sustained pay rises.

The Bank have too much relied on a pay rise in theory, when that same theory has failed for at least a decade. Above all it has been repeatedly shown that falling rates of unemployment do not lead to higher pay growth, instead they have been supported by low pay growth. This should not be the natural state of affairs, but it is the reality engineered by policymakers in the post global financial crisis world. Similarly while labour has been withdrawn since Brexit and during the pandemic, withdrawn labour is also a feature of all recessions and can quickly reverse when economic activity picks up pace.

And now the Bank find underlying pay growth of only 4 per cent which might rise to 5 per cent (MPR, pp. 61-62). So at best pay growth will be half the forecast peak in inflation, and real pay will therefore decline by five per cent. This is not a wage price spiral this is a collapse of real pay.

The Bank now forecast a record decline of 1¾ per cent in real (post-rax) household disposable incomes, noting “apart from in 2011 … the largest contraction since records began in 1964” (MPR, p. 15). And now their so-called central view is for negative GDP outcomes over the first three quarters of 2023. In effect they now admit they are setting a course to a (mild) recession.

Rather than seek justification for restraint when pay is already caving in, policymakers should be helping to support pay and so support the economy. Every extra pound that must be paid to energy companies is a pound that will not be spent in the shops.

The Bank make the important point that inflation is hitting hardest the poorest, to the extent that even the Chancellor has finally been forced to take action. But to bemoan such inequities while standing in the way of pay rises exemplifies the contradictions of a system that has for at least 40 years has favoured the wealthy at the expense of workers.

It is hardly surprising that the Governor’s telling workers to exercise pay restraint caused such outrage.5 Late in the day the Bank conceded that firms could instead put up pay and take a hit on profits. But still MPC members talk tough, e.g. Dave Ramsden argued “households and businesses” need to recognise that “persistent high inflation in their own wage and price setting” will not be “tolerated”.6 But it seems on the other hand that City bonuses will be tolerated.

Pay for workers can and must be encouraged to rise.

First – even according to the zero-sum mindset that defines policy thinking7 – firms could increase pay and take a hit on profits. The labour share in the UK has fallen significantly over the past 60 years, from 59 per cent in the two decades after the Second World War to 48 per cent in the five years ahead of the pandemic. The hit on profits might be absorbed as lower dividend payments, which have for the past decade risen rapidly as pay has stagnated.8

Second – outside the zero-sum mindset – a pay rise will further advantage the economy. Treating workers properly should lead to productivity or supply side gains. And, likely more importantly, higher pay will mean demand is strengthen rather than reduced.

Third – pay and prices might be allowed to rise together so that firms and households are both immediately advantaged – this has been called ‘running the economy hot’. Under these conditions any disadvantage is to the wealthy, with asset values hit by higher inflation but workers and firms protected (though asset holders might also be protected as in the case of index-linked gilts - in this case by the taxpayer). Increasing interest rates now risks privileging wealth over workers.

Fourth is the wider concern that financial fragilities mean the (global) economy is less able to cope with interest rate rises. Since the global financial crisis, central banks have repeatedly tried to tighten (or ‘normalise’) policy, but have retreated when financial markets reacted badly in 2009, 2013 and 2018. The latter retreat was underway when the pandemic struck; at the time a ‘systemic risk council’ of great and good bankers and academics remarked:

Covid-19 strikes the world at a time when too many corporations around the world are over-indebted, and after a period during which persistently favourable market conditions caused traders to take aggressive positions, exposing them and the system to spikes in volatility, let alone a collapse in asset values”.9

Last weekend, the Financial Times headlined “Wall Street stocks hit bear territory”, with the “S&P 500 … down 20 per cent from the record high reached on January 4 – the typical definition of a bear market”. They cite a fund manager: “The strong consensus narrative is that growth goes down from here, there is a recession in the foreseeable future …".10

The emerging disarray in financial markets plays into the fundamental concern that policymakers have not found a way forward from the global financial crisis, and instead keep falling back on old broken ways. The head of the IMF Kristalina Georgieva has called out a Bretton Woods moment,11 “to fight the crisis today – and build a better tomorrow”. Trade unions contend any such approach must reset the balance to labour from wealth.

The system that sacrifices the needs of the many to the interests of the few needs to be brought to an end.12 As trade unions have always understood, doing so is counterproductive both in terms of fairness and in terms of a better economy. The present inflation should not be one of a number of repeated excuses to avoid discussion of building back better.

Annex: Short-, medium- and long-term trends in pay and wage share: a review of recent literature

In this paper, I will discuss several factors affecting pay in the long, medium and short term, including inflation, employment rates, and productivity, and consider how the relationship between these factors and pay differs from economic convention. I will also examine how labour’s share of income has changed over time, and the divide that has opened between the highest paid and other workers.

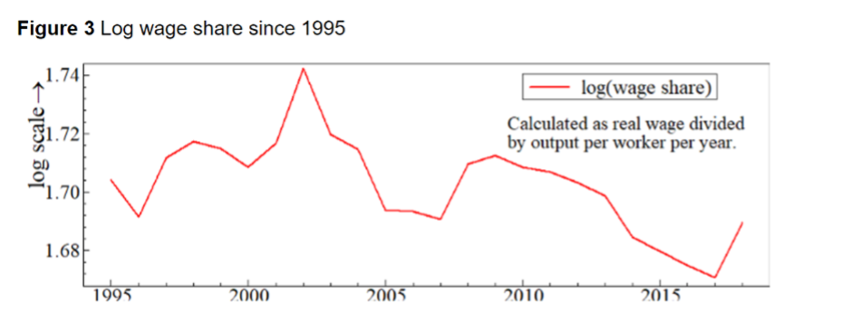

The fall of the wage-share over time

In economic literature, national income is divided between wages, profits and rents. Labour share is the portion of incomes which is earned through wages and salaries. Guerriero (2019) argues that this is more complete than household income as a measure of renumeration for labour as it includes all forms of renumeration, including bonuses, commissions, tips, allowances, and employers’ contributions to pensions. Labour share is also commonly used as a metric of the strength of the working classes as they are least likely to hold assets in profits, rents or dividends. An analysis of the labour share allows us to compare the returns going to workers against those going to capital.

- 3BoE walks tightrope between inflation and recession, Bailey says’, Reuters, 21 April 2022: https://www.reuters.com/world/uk/boe-walks-tightrope-between-inflation-recession-bailey-says-2022-04-21/

- 4“Q434 Sir Dave Ramsden … 80% of the overshoot is to do with first round effects—the shocks that have hit the economy—so you are talking about the behaviour of firms and bargainers in the labour market only for the other 20%. You are talking about a very small part of the inflation overshoot that we have seen”; https://committees.parliament.uk/oralevidence/10215/pdf/

- 5“In the sense of saying, we do need to see a moderation of wage rises, now that’s painful,” he said. “But we need to see that in order to get through this problem more quickly.” (Financial Times, 4 Feb. 2022)

- 6Shocks, uncertainty, and the monetary policy response’, speech by Dave Ramsden, 22 Feb. 2022: https://www.bankofengland.co.uk/speech/2022/february/dave-ramsden-speech-at-the-national-farmers- union-conference-2022

- 7 See Heather McGhee (2021) The Sum of Us: What Racism Costs Everyone.

- 8Over 2014 to 2018, dividends to FTSE 100 shareholders rose by 58.3 per cent while average UK worker wages increased by just 8.8 per cent (in nominal terms). ‘How the shareholder first business model contributes to poverty, inequality and climate change’, 2019, briefing note from High Pay Centre and the TUC: https://www.tuc.org.uk/sites/default/files/2019-11/Shareholder%20Returns%20report.pdf

- 9SRC Statement on Financial System Actions for Covid-19’, 19 Mar. 2020: https://www.systemicriskcouncil.org/2020/03/src-statement-on-financial-system-actions-for-covid-19/

- 10Financial Times, 21/22 May 2022

- 11 ‘A New Bretton Woods Moment’, October 15, 2020: https://www.imf.org/en/News/Articles/2020/10/15/sp101520-a-new-bretton-…

- 12TUAC have set out a fuller argument that is global in scope in a paper presented to the OECD liaison committee. https://tuac.org/news/oecd-tuac-liaison-committee-meeting-policies-for-framing-the-recovery-en-fr/

While there are concerns about the labour’s declining share of income across rich countries, the reasons for the decline are not fully understood (McKinsey & Company, 2019). A wide body of research has explored the decline and stagnation in labour share in the UK, leading to several competing explanations.

There are several competing theories explaining the fall in labour’s share of income over this period. A shift from labour-intensive to capital-intensive production may have been one of the drivers of this shift (OECD, 2015). Another significant factor is increasing wage inequality throughout the global north and the rising use of non-wage benefits (Teichgräber & Van Reenan, 2021).

The trade union movement believes that a significant factor behind the declining labour share is neo-liberal policies that have transferred power from workers to business owners. The strength of the trade union movement has helped to protect and expand the rights of workers across the world (Rosenfeld, Denice, and Laird 2016; Bivens and Shierholz, 2018).

The Labour Share in the UK

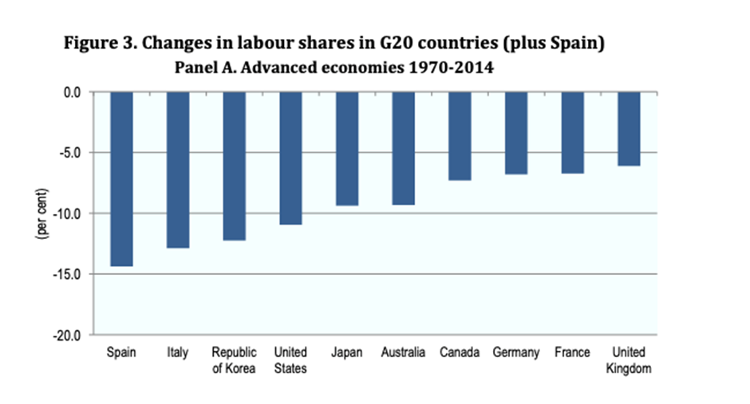

In the UK, this movement was in ascendency from the end of the Second World War until the 1970s. But since the 1980s, the weakening of trade unions and curtailing of employee rights has shifted national income away from labour to the detriment of wage-earners, including through successive anti-union pieces of legislation. This may have impacted labour share as union density has been shown to have a beneficial impact on incomes across society (Rosenfeld, Denice, and Laird 2016). Since the height of trade union strength around the 1960s and 1970s, the labour share in the UK has fallen by around 12 per centage points. In the 1960s, workers received 72p of every pound of UK GDP. By 2020, that had fallen to less than 60p.

One significant omission when calculating labour share is that it does not include income from self-employed labour. This is an important factor as the number of self-employed workers in the UK has increased rapidly since the turn of the millennium. While some of this is individuals who are genuinely self-employed, much of this is “bogus self-employed” in order to avoid taxation associated with employment either on the part of the employer or the employee. This has led to a significant undervaluation of the true labour share (Teichgräber & Van Reenan, 2021).

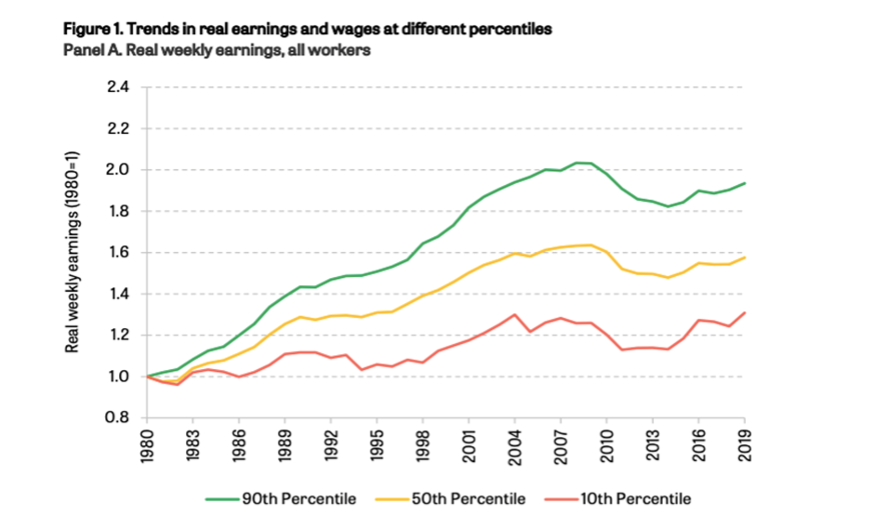

The growth of inequality

In addition to the overall fall in the share of national income going to workers, rising inequality between workers has meant that the ‘average’ worker has lost out. That can be seen in the gap between median wages (the wages of the average person) and productivity is much larger than the gap between mean wages (the average wage) and productivity. In other words, a larger proportion of labour income is going to the rich.

While the introduction of a national minimum wage in the UK has helped to close the inequality gap by raising pay at the lower end of the spectrum, it has not addressed the root causes of inequality or the runaway incomes of the richest in society.

Specifically, this growing divergence has included two distinct dimensions of inequality: the surge of compensation received by the top 10%—particularly the top 1.0% and top 0.1%—and the erosion of labour’s overall share of income and the corresponding growth of capital’s share.

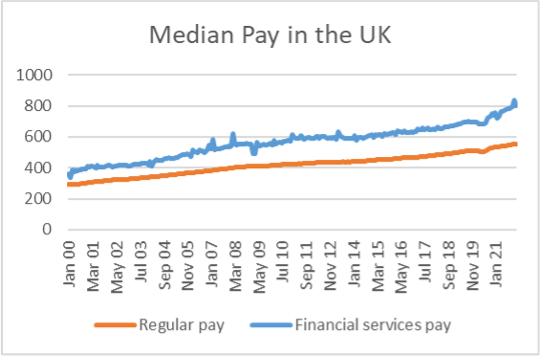

This has been partially driven by the growth of the financial services sector in the UK. This sector has experienced steady growth since the 1980s despite the financial crash and now accounts for 8.6% of GDP, most of which is concentrated in the City of London. The growth of the financial services sector mirrors the fall of manufacturing in the industrial heartlands, leading to greater regional inequalities. Furthermore, pay in the sector is well above UK median pay and it has seen stronger pay growth than the rest of the economy since the financial crash. Pay in the sector has also surged post-pandemic and the growth in bonuses in this sector has increased dramatically.

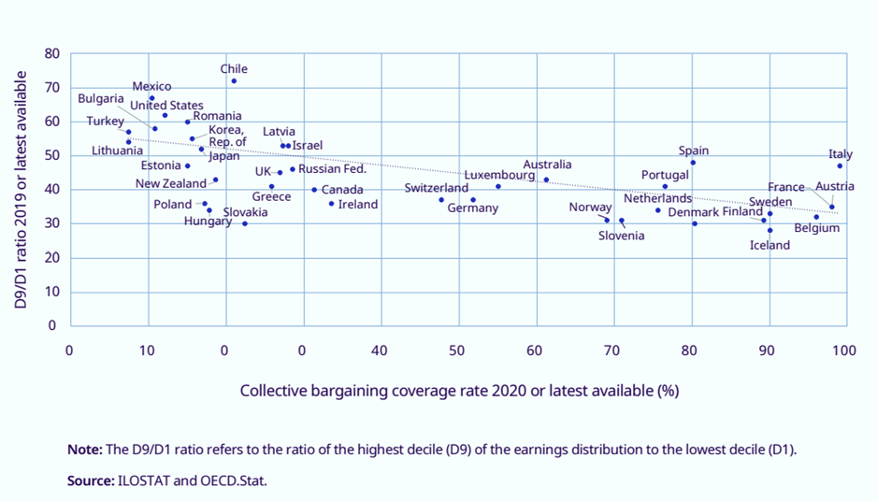

A large cause of the shift of national income away from labour to the detriment of wage-earners was the weakening of trade unions and curtailing of employee rights through the Trade Union Act. Trade Unions are a crucial factor in determining labour’s share of income, primarily through collective bargaining mechanisms. Evidence from Europe found that collective agreements both increased the pay of those at the bottom of the wage distribution and reduced pay inequality within organisations (Vaughan, Whitehead and Vazquez-Alvarez, 2018). Among high-income countries, those with coordinated bargaining systems and high collective bargaining coverage are associated with higher employment, a better integration of vulnerable groups of workers and lower wage inequality than those with fully decentralized bargaining systems (Garnero, 2020; OECD, 2019).

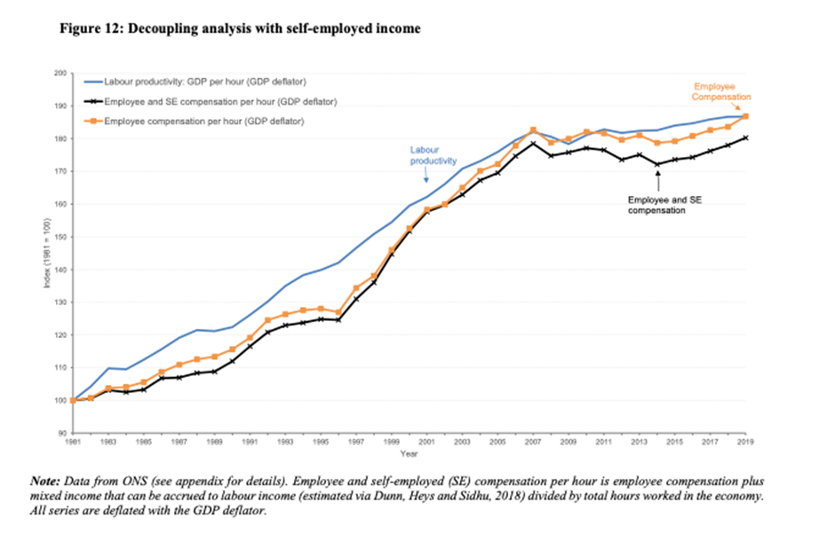

The untethered relationship between wages and productivity (1980s onwards)

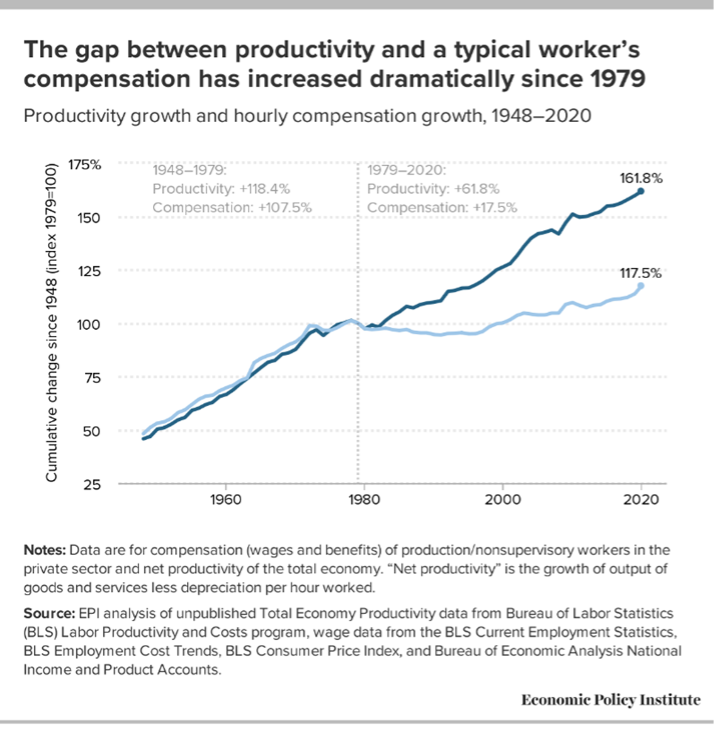

In a conventional growth economic model, wages are expected to rise with productivity. While there is historic basis for a direct link between wages and productivity across different countries and industries (Meager and Speckesser, 2011), the relationship has become untethered in the past fifty years in most advanced economies.

This is particularly prominent in analysis by the Economic Policy Institute (EPI) into the relationship between pay and productivity in the US. The EPI believed this was the result of policy decisions which allowed businesses and high earners to siphon wealth from the economy and prevented workers from reaping the rewards of productivity gains.

In the UK, this trend is less striking, but there has still been a widening gap between the hourly compensation of a typical (median) worker and productivity (Brill et al, 2017)—the income generated per hour of work—in recent decades as a result of anti-union sentiment and legislation.

This pattern has also been taking place in much of the developed world, with labour’s share of income steadily declining ever since in most countries in the Organisation for Economic Co-operation and Development (OECD, 2015). This is partially attributed to the rise of multinational firms as a result of globalisation, which has enabled business owners to extract greater profits by outsourcing labour and operations. Furthermore, these economic changes may have themselves precipitated political change away from class-based ideas of labour share, towards a greater focus on metrics such as social mobility (Krämer, 2010; Guerriero, 2019).

Low pay and high employment (2010 to current)

In the UK, the number of people in employment has been rising steadily following the financial crash to a historic high (with an exception of 2020-2021 as a direct result of the pandemic). In classical economics, this shortage of excess labour (through lower unemployment) would force employers to compete to attract staff, typically by offering higher pay settlements to workers. Instead, real wages did not rise at all during this period and labour’s share of income remained stagnant.

The increase in low-quality, insecure jobs helps to explains both pay stagnation in this period and the low levels of unemployment. This period is also characterised by the rise of the “gig economy” and zero-hour contracts, where workers did not have consistent working patterns or hours, but instead worked as and when their employer needs them. Analysis by the TUC found employment in the gig economy nearly tripled since 2016 and, according to the ILO, the number of digital labour platforms today globally is five times greater than it was a decade ago. This has created widespread underemployment in the economy, meaning that there is still a lot of slack in the job market, which is not reflected in employment statistics.

At the same time, self-employment rose rapidly in the UK. While this group is mostly compromised of the low-paid, gig-economy workers above, it also includes highly paid, professional contractors. The self-employment accounts for over a third of all employment growth since the onset of the financial crisis. The level and growth of solo self-employment in the UK are among the highest in OECD countries. The Institute for Fiscal Studies (IFS) also found that a prevalence of self-employed workers led to a downward pressure on wages. In addition, self-employed workers do not have many of the rights of workers in typical employment. In the past two years, there has been a fall in the number of self-employed workers, largely as a result of the pandemic pushing many into typical employment and changes to the taxation system which created greater parity in tax paid by self-employed and typically employed workers.

Poor pay growth during this time can also explained by the public sector pay freeze, whereby the pay of roughly 21.5% of UK employees were suppressed. The pay freeze lasted two years from 2010 – 2012 and workers experienced a real terms pay cut as prices rose by 8.8% between April 2010 and April 2012 as measured by the Retail Prices Index (RPI). As a result of this, workers were more than 6% worse off in real terms in 2012 than they had been two years earlier. This disproportionately affected women and Black and minority ethnic (BME) workers, who were more likely to work in the public sector. This pay freeze was followed by a pay restraint of 1% until 2016, causing workers in some professions experiencing a real term pay cut of 15% over this period. In addition, austerity involved a high volume of job losses in the public sector, which limited the bargaining power of these workers.

Research from Norway suggests that high union density corresponds with firms reporting higher levels of productivity (Barth et al, 2020), suggesting that improved levels of pay may have far-reaching benefits for the whole economy. The move towards more casualised, insecure work is also thought to contribute to low productivity levels, as shorter contracts led to a decrease in institutional knowledge. Alam et al (2020) found a symbiotic relationship between wages and productivity.

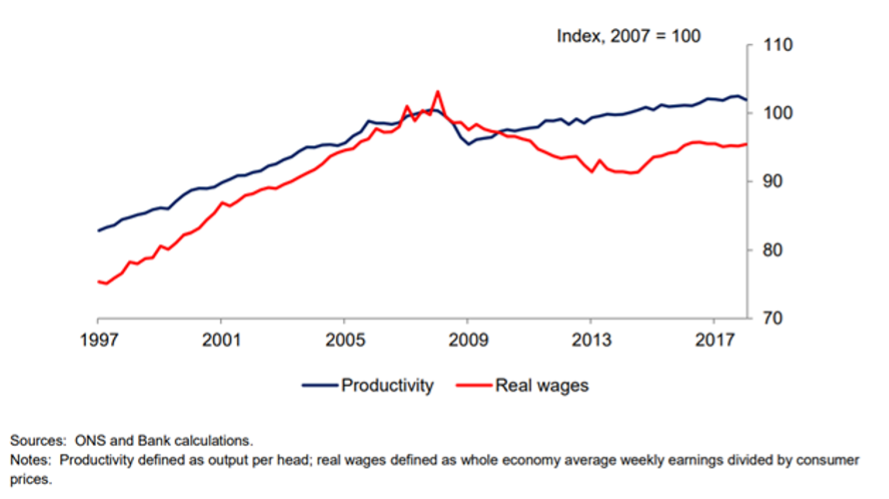

In the UK, productivity has stalled since the financial crash in 2007-08. There is a long debate on the possible causes of this, but it is likely due to austerity limiting government spending and dampening demand in the economy.

Despite this, the Government has adopted the rhetoric of a “high-skill, high-wage” economy, where workers are expected to benefit from increased productivity, particularly in the North of England. However, the recently published Levelling Up whitepaper contains little substance on addressing productivity, let alone any tangible solutions to redressing unbalanced relationship between productivity and wages.

Inflation squeezing wages (2020 to current)

At the same time, the Government further attacked the rights of organised labour through the Trade Union Act 2016 which severely impacted the ability of unions to campaign and carry out industrial action. This stripped workers of a key piece of leverage and further impacted their ability to effectively negotiate pay settlements and has contributed to the deregulation of the labour market.

As we emerge from the pandemic, there are a high level of job vacancies and unemployment has dropped, reaching 4.1 per cent in the three months to November 2021. This has forced some employers to offer higher pay awards to both attract and retain workers, but, crucially, these pay awards have not kept pace with inflation.

At the same time, the employment rate remains around 1 percentage point lower than before the pandemic, providing a partial explanation for the fact that total hours are 3 per cent below their early-2020 peak. According to the Institute of Employment Studies (IES, 2022) 38 per cent of the reduction in labour market activity can be attributed to a smaller population (lower net migration and demographic changes, potentially including excess deaths) but the majority is explained by greater inactivity, particularly among older workers.

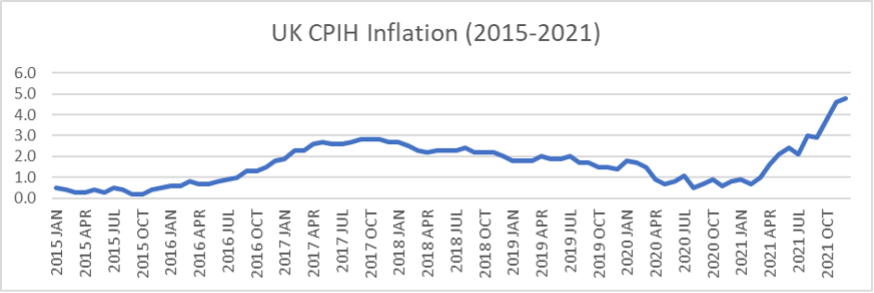

Inflation is the most recent factor which may affect pay. Due to a combination of supply-side factors (not least energy), inflation in the UK has soared and CPI is currently 5.5% - its highest rate in 30 years. This has created an immediate cost of living crisis which has been exacerbated by the war in Ukraine leading to higher oil and gas prices. Even more worryingly, it is forecast to rise to over 7% in spring 2022. As demonstrated below, this is a departure from the low and steady levels of inflation which have characterised the past few decades in the UK.

When inflation is high, it is crucial that workers and unions secure pay rises to prevent pay from falling in real terms. This is particularly important in the private sector, as pay rises in the public sector are now decided by pay review bodies. However, union density in the public sector has decreased over this period and remains stubbornly low in the areas where the need for better pay is greatest.

While there has been anecdotal evidence of recent higher pay settlements, there is nothing to suggest that wages are rising across the board. Indeed, the evidence points towards a steepening decline in real wages. However, the economic climate presents short-term opportunities for Trade Unions to win headline-grabbing pay settlements, as has been the case for haulage and refuse collectors.

While public sector pay settlement processes are ongoing, government ministers have already signalled that public sector staff are unlikely to receive inflation-busting pay rises. Even the headline 3% pay rise for some NHS staff was only enough to keep pace with rising costs as a result of inflation at the time. NIESR expects private sector pay to rise by 5.6% in the first quarter of 2022, and while this is the highest increase in some time, it remains below inflation. There is also a tendency for pay growth forecasts to be overly optimistic.

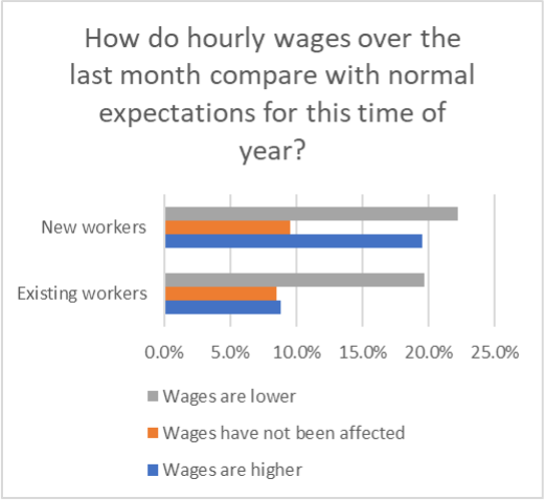

This pattern seems to carry over into the private sector too. In a business survey carried out by the Office of National Statistics (ONS) between 27 December 2021 and 9 January 2022, business owners felt that on balance hourly wages had fallen over the past year for both new and existing workers.

In addition, a report by the International Labour Organization (ILO) found that monthly wages fell or grew more slowly in the first six months of 2020 in two-thirds of countries for which official data was available, and women and the low-paid were disproportionately affected. Unfortunately, they predicted that this trend would continue in the short-term, undercutting wages further.

Furthermore, The Global Wage Report 2020/21 shows that not all workers have been equally affected by the crisis. The impact on women has been worse than on men. Estimates based on a sample of 28 European countries find that, without wage subsidies, women would have lost 8.1 per cent of their wages in the second quarter of 2020, compared to 5.4 per cent for men.

Furthermore, the ILO speculates that statistics may not accurately reflect the current economy as substantial numbers of lower-paid workers have lost their jobs and so have skewed the average since they were no longer included in the data. Indeed, while unemployment is only 4.1%, the level of economic inactivity is much higher at 21.2%. Young people (those aged 16 to 24 years) have been particularly affected by the coronavirus pandemic, with the employment rate decreasing and the unemployment and economic inactivity rates increasing by more than other age groups (ONS).

Conclusion

When examining these factors, it is clear to see that the levers of free market economics have failed to fairly allocate income to workers in the UK for almost half a century. Considering this, it is more important than ever that we have an empowered trade union movement to readdress the relationship between labour and capital. Next year the UK is expected to experience the biggest fall in living standards in more than 60 years (Office for Budget Responsibility, 2022).

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox