Fixing the safety net: Next steps in the economic response to coronavirus

This report sets out what the government must now do to protect jobs, provide proper sick pay for all and protect the livelihoods of those who lose their jobs.

Protect jobs

Government should build on the welcome job retention schemes by:

- Increasing the flexibility of the scheme to support short-time working. One solution would be to allow that where unions and business have agreed, firms should be able to furlough workers for a minimum of one week rather than three.

- Clarifying that employers can reclaim 80% wage costs for pregnant workers on medical suspension

- Working with unions representing self-employed people to fix the gaps in the self-employed income support scheme.

Sick pay for all

- Government should urgently increase the weekly level of sick pay from £94.25 to the equivalent of a week’s pay at the Real Living Wage – around £320 a week.

- Government needs to act now to remove the lower earnings limit for qualification for sick pay, and ensure everyone can access it, no matter how much they earn.

Fixing our social safety net

- Suspend any conditionality requirements with Universal Credit, as well as parts of the application process.

- Remove the savings rules in universal credit to allow more people to access it.

- End the five week wait by converting emergency payment loans to grants.

- Raise the basic level of Universal Credit. We believe it should reach £260 a week.

- Significantly increase Child Benefit payments.

- Ensure no-one loses out by removing the benefit cap, and the requirement that anyone who experiences a change of circumstance transitions onto Universal Credit.

- Remove the minimum hours requirements in working tax credits.

- Introduce a wider package of support for households, including a fully funded council tax freeze, an increase in the hardship fund and a wider package of support for renters.

Work with unions and business

- Since the start of the coronavirus outbreak, the TUC has called for government to set up a taskforce bringing together unions, government and business to work together to help address the crisis. This remains the best way to collectively address the huge challenges we face, from ensuring safe working to protecting jobs.

Introduction

The last few weeks have seen an unprecedented change in the economic situation of the UK. Since the Prime Minister announced a full ‘lockdown’ on the 23rd March, economic activity in the UK has been rightly restricted in the service of protecting public health.

The TUC has clear priorities throughout this crisis. First, to ensure that public health is protected. Second, to protect workers’ jobs and livelihoods.

Following calls from the TUC and unions the government has announced welcome schemes to try to keep people in work. Protecting jobs must be the first step to protecting incomes and ensuring the country can get back on its feet when the crisis subsides. We set out further steps to improve these schemes below.

But there is still more to do to ensure everyone who is sick gets the income support they need and support the livelihoods of those who do lose their jobs.

Our safety net has been dramatically undermined after years of underinvestment. The UK has avoided mass unemployment since the recession of the early 1990s, and the devastating unemployment of the early 1980s. Those experiences left deep scars, which we are still seeing the legacy of today. It is vital the government does everything it can to keep people in work now.

But even in the 1990s, our safety net was stronger. In 1993, the last time the unemployment rate went over 10 per cent, the basic rate of unemployment benefit was worth around a fifth of average wages . In 1984, when unemployment was over 11 per cent, the benefit was worth a quarter of the average wage. And in 1979, it was worth 30 per cent of the average wage. Today – even after the recent increase in the rate by £20 a week – the basic rate of universal credit is worth around a sixth of average weekly pay (17 per cent).

The UK system also compares poorly to the support provided internationally. In most European countries, unemployment benefits are related (at least in the initial period of unemployment) to previous wages to cushion income shocks, ranging from 60 per cent of previous wages in Germany to 90 per cent in Denmark.

This report sets out what the government must now do to:

- Protect jobs

- Provide proper sick pay for all

- Protect the livelihoods of those who lose their jobs.

We particularly focus on fixing the social safety net in this report, building on our previous reports on sick pay, a job retention scheme, and support for the self-employed. It calls for the government to urgently raise the basic level of universal credit. Restoring ‘replacement rates’ to the level seen before the long dismantling of the safety net began in the 1980s, would mean increasing the payment of universal credit to £165 a week – around 30 per cent of average wages.

But we think the government should be more ambitious to protect against this income drop. We recommend raising the basic rate of universal credit for this period to the value of 80 per cent of weekly earnings at the national living wage – or £260 a week.

1. Protecting workers’ jobs

Keeping workers in their jobs and being paid wages is the best way to protect their incomes, and to ensure that the country can get moving as swiftly as possible once the public health crisis is over.

Following calls from the TUC and wider trade union movement, the government announced a Job Retention Scheme on the 20th March, and a Self-Employment Income Support Scheme on the 26th March. Below we set out brief details of each scheme, and how they can now be improved to support more workers.

Initial data suggests there is likely to be a high take up of the schemes; a survey of over 600 businesses by the British Chambers of Commerce found that “almost half of respondents (44 per cent) expect to furlough at least 50% of workforce in the next week.”1

The TUC believes it is imperative that businesses use these schemes rather than make people redundant. As we set out in our last report, 2 Government has also introduced a range of support for businesses affected by coronavirus which should enable them to keep workers on.

The Job Retention Scheme

The Job Retention Scheme is designed to prevent redundancies for businesses affected by coronavirus. It will reimburse 80 per cent of furloughed workers’ wage costs, up to a cap of £2,500 per month. Key features of the scheme are:

- It is backdated to the 1st March. Workers who have been made redundant since then can be rehired and furloughed.

- All workers on a PAYE payroll are included provided they were in work on the 28th February 2020. This includes those on zero hours contracts or in agency work;

- Firms must gain the agreement of workers who they furlough, using collective consultation mechanisms (including through trade unions) where necessary.

- Employers can – and the TUC believes should – top up workers’ wages to 100 per cent.

The TUC welcomed the introduction of the scheme, and the constructive engagement we have had with government. However there are still some areas where we are urgently seeking clarity:

How the scheme can support short time working

Many unionised workplaces are keen to negotiate short-time working schemes, in order to keep business operating, staff in work as far as possible, and skills maintained.

At present, our understanding is that the Job Retention Scheme may allow for some retention of workers – with for example, one half of the workforce off for the minimum three week furlough period, followed by the other half.

However, further flexibility, mirroring other European schemes, would help more workers stay in their jobs, and keep business running. One option to achieve this would be that where unions and business have agreed, firms should be able to furlough workers for a minimum of one week rather than three.

Clarity that employers can reclaim 80% wage costs for pregnant workers on medical suspension.

If pregnant workers cannot work because of health and safety risks, the law stipulates they should be suspended on full pay. The government should extend the job retention scheme so that employers can reclaim 80 per cent of these workers’ wages. However, it is, and should remain, a legal requirement that employers continue to pay the affected pregnant workers full pay based on their usual earnings not contractual pay.

The self-employed income support scheme

The self-employed income support scheme will support people who had a self-assessment tax return for 2018/19, who make the majority of their income from self-employment, and whose profits are below £50,000, based on an average of their last three years of income (or the maximum number of years available).

Self-employed people will be paid 80 per cent of their incomes up to a maximum of £2,500 a month, and unlike those who are employed will be able to continue some economic activity.

The complexity of dealing with self-employment reflects the fragmentation and casualisation of the labour market over the past decade. Many self-employed people have been forced into complex pay and employment relationships by employers seeking to minimise both their tax liabilities and responsibilities for the workers who keep their businesses running. These include workers in construction, the creative industries and journalism, and many other sectors.

Unions have raised a number of issues with the self-employed income scheme including:

- People who have multiple engagements where they are paid through PAYE may not have an employer willing to furlough them, but cannot access the self-employment income support scheme.

- Those who have started self-employment in the past year have no form of support.

- Those who may have taken time out due to maternity or other caring responsibilities in the previous year may see the level of support they can claim for diminished.

- The delay in implementing the scheme until June will leave many workers facing financial hardship.

Government should start urgent discussions with unions representing self-employed workers on how best to address these and other issues.

But for workers who fall through the gaps it is even more important that the additional support provided through universal credit is fit for purpose.

2. Sick pay for all

The Job Retention Scheme guidance is clear that those who are sick should claim sick pay, rather than seeking to be placed on furlough. But the current low levels of sick pay will mean that many workers still face an impossible choice: go to work when sick or see a dramatic fall in their income.

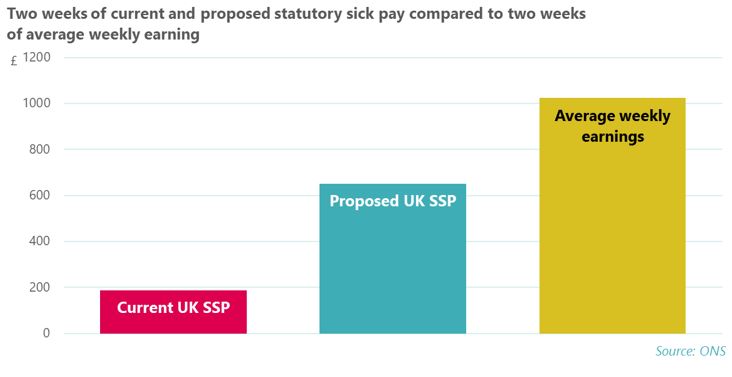

Average weekly wages are around £500, meaning that someone receiving sick pay of £94 a week would see their income fall by over £400. The Health Secretary, Matt Hancock, admitted on Question Time that he couldn’t live on £94 a week. The government should not expect workers to either.

- 1 British Chambers of Commerce, 2nd April 2020 ‘BCC Coronavirus Business Impact Tracker: First results show heavy toll on UK business communities as majority of firms face cash flow crisis’ available at https://www.britishchambers.org.uk/news/2020/04/bcc-coronavirus-business-impact-tracker

- 2 TUC (2020) Fixing the safety net: What next on supporting working people’s incomes? Available at https://www.tuc.org.uk/research-analysis/reports/fixing-safety-net-what-next-supporting-working-peoples-incomes

Government should urgently increase the weekly level of sick pay from £94.25 to the equivalent of a week’s pay at the Real Living Wage – around £320 a week.

In addition, almost two million people are not eligible for sick pay, because they earn too little to qualify. 70 per cent of these workers are women.

In response to this problem, the government has increased the support available via universal credit – available to people who don’t get sick pay – to £94 a week.

But claiming benefits remains complex, and as we set out further below, some people may miss out because their savings are too high, or because their household income pushes them over the income threshold – for example due to having a partner still in work.

Government needs to act now to remove the lower earnings limit for qualification for sick pay, and ensure everyone can access it, no matter how much they earn.

1. Fixing our social safety net

The best way to protect people’s incomes is to keep them in work. But we know that many more people are already having to turn to the social security system.

The Department for Work and Pensions has said that 950,000 applications for universal credit were made between 16 March, when people were advised to work from home, and the end of the month. The department would normally expect 100,000 claims over this period.3

Not all of these claims will be from people who have lost their job – many may have seen hours drop. But the huge scale of the increase shows how vital social security will be in supporting people through the crisis.

Even before the pandemic began in the UK, it was clear that our social safety net was broken. In 2019, the UN Special Rapporteur on extreme poverty published a report on poverty in the UK. In it, he explains how years of austerity policies have ‘systematically and starkly eroded’ our social safety net, with ‘tragic social consequences’4

.

These consequences are clear in the most recent poverty data. The number of people living in poverty in the UK is at a record high of 14.5 million. This includes 4.2 million children. The majority (56 per cent) of those living in poverty live in a working household. Among children in poverty, a shocking 72 per cent are living in a house where at least one parent works 5

And nearly half of those in poverty, 6.9 million people are from families in which someone has a disability.

Foodbank use is also at a record high. The Trussell Trust, a charity that runs over 1,200 food bank centres, reports that it experienced its busiest ever mid-year period in 2019, as demand for food banks soared by 23 per cent compared to the previous year 6

. 2019 also saw unsecured debt per household hit a new record high of £14,500 7

and debt charities reporting being busier than ever 9

.

Unless changes to our social security system are made, this situation will likely worsen as job losses, as well as gaps in the existing schemes put forward by the government, lead to more people becoming reliant on a patchy and punitive social security system.

Four main issues have already come to the forefront in the context of coronavirus:

1.Payments are too low.

A benefits freeze has been in place since 2016, which has meant that most working-age benefits have stayed at their April 2015 level for the past five years. Benefits were also capped at 1 per cent for the three years before this. While the freeze will end in April 2020, damage has already been done. Weekly income support for a single person is currently £73.10, and has been at this level for five years. These real cuts to benefits payments have caused a cost of living crisis for those on benefits. The Joseph Rowntree Foundation estimates that the freeze will have pushed 400,000 people into poverty by the time it finally ends this April 10

.

And the level of support available to those who lose their jobs compares poorly to that which people received in previous recessions.

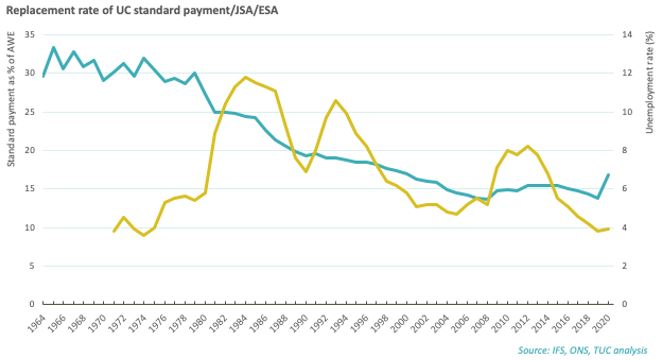

The chart below shows the level of unemployment benefit as a proportion of average weekly earnings on the left axis, and the unemployment rate on the right axis.

- 3 BBC News 1st April 2020 ‘Coronavirus: Nearly a million universal credit claims in past two weeks’ available at https://www.bbc.co.uk/news/uk-politics-52129128

- 4 Report of the Special Rapporteur on extreme poverty and human rights, Office of the High Commissioner for Human Rights. Available at: https://ap.ohchr.org/documents/dpage_e.aspx?si=A/HRC/41/39/Add.1

- 5 Poverty is defined as being in relative low income after housing costs. Households Below Average Income statistics, Department for Work and Pensions. Available at: https://www.gov.uk/government/statistics/households-below-average-income-199495-to-201819.

- 6 Mid-year stats, The Trussell Trust. Available at: https://www.trusselltrust.org/news-and-blog/latest-stats/mid-year-stats/

- 7 TUC analysis of the UK Economic Accounts data published by the ONS. Data available at: https://www.ons.gov.uk/releases/ukeconomicaccountsoctobertodecember2019 [/fn}, as the number of insolvencies grew to their highest level since the recession

Individual insolvency statistics, October to December 2019. GOV.UK – The Insolvency Service. Available at: https://www.gov.uk/government/statistics/individual-insolvency-statistics-october-to-december-2019 - 9 StepChange reveals record number seeking debt advice, StepChange. Available at: https://www.stepchange.org/media-centre/press-releases/stats-midyear-2019.aspx

- 10 End the benefit freeze to stop people being swept into poverty, JRF. Available at: https://www.jrf.org.uk/report/end-benefit-freeze-stop-people-being-swept-poverty

As the chart clearly shows, even after the £20 increase in the basic rate of universal credit announced on the 20th March, replacement rates fall well below the last time we saw large scale unemployment during the early 1990s recession, and the devastating unemployment of the 1980s.

These bouts of unemployment left deep scars. It’s vital that government does everything it can now to keep people in work. But even in the 1990s, our safety net was stronger. In 1993, the last time the unemployment rate went over 10 per cent, the basic rate of unemployment benefit was worth around a fifth of average wages. In 1984, when unemployment was over 11 per cent, the benefit was worth a quarter of the average wage. And in 1979, it was worth 30 per cent of the average wage. Today – even after the recent increase in the rate by £20 a week – the basic rate of universal credit is worth around a sixth of average weekly pay (17 per cent).

The UK system is also strikingly less generous than in most other European countries, where unemployment benefits are related (at least in the initial period of unemployment) to previous wages to cushion income shocks, ranging from 60 per cent of previous wages in Germany to 90 per cent in Denmark.

Unemployment benefit rates in selected European countries as of July 2019

|

Country |

Basic amount of unemployment benefit |

|

Austria |

55 per cent of daily net income prior to unemployment (with minimum payments) |

|

Belgium |

55 per cent of previous salary for single people |

|

Denmark |

90 per cent of previous gross earnings up to a maximum of €2,527 per month |

|

Germany |

60 per cent of previous net earnings for those without children |

|

Italy |

75 per cent of monthly earnings up to €1,329 per month |

|

Spain |

70 per cent of monthly earnings for first 180 days, then 50 per cent |

|

Sweden |

80 per cent of reference income for first 200 days, up to maximum €94 a day, then 75 per cent |

|

The Netherlands |

75 per cent of last daily wage for two months, then 70 per cent |

Information taken from MISSOC – where more information is available on eligibility requirements and how payments are calculated see www.missoc.org

2.The five-week wait for universal credit is too long.

New universal credit claimants must wait five weeks for their first payment. Advance loans are available, but these must be paid back out of future benefits payments. As set out above, benefits payments are already too low, and the loan repayments push these payments even lower.

3.Too many people may miss out because they have savings.

Universal credit is not available to those with savings of over £16,000. This not only complicates the application process, but may mean that many people are unable to get help. This may particularly affect self-employed people who may have been saving to purchase new equipment – for example a van or new camera equipment.

4.The service is struggling to cope with the demands from new applications.

The surge in new claimants for universal credit is creating enormous pressure for those processing applications, especially as staffing numbers are affected by coronavirus.

The government has announced some changes to social security

In terms of measures directly related to social security, the basic amount of universal credit has been increased by £1,000 per year. This means the weekly amount is now £94, matching the statutory sick pay (SSP) rate. Eligibility for Universal Credit has been widened, with self-employed people no longer needing to meet a minimum income floor in order to qualify for the benefit.

As well as this, housing benefit has been increased. The local housing allowance has been increased so that it covers up to 30 per cent of the market rent in the local authority, restoring the position prior to the Welfare Reform Act in 2012 which dramatically cut Housing Benefit alongside many other forms of support. 1

The government has also introduced a £500 million hardship fund for local authorities, which it has clarified is to be used to provide council tax relief to vulnerable people and households. The money is intended to be used by councils to reduce the 2020/2021 council tax bills of working age people receiving Local Council Tax Support, as well as any further discretionary support.

The government has also announced that it will stop deductions for some forms of benefit debt, but will continue to recover advance payments within universal credit. 2

What still needs to be done

The government now needs an urgent plan to fix the safety net and support those who do lose their job.

An emergency rehaul of universal credit

We are calling for six measures to be put in place:

1. Suspend any conditionality requirements with universal credit, as well as parts of the application process. Applications for universal credit are being delayed by the need to carry out a telephone appointment with a work coach. The requirement to hold a phone interview should be suspended, in addition to any work-related conditionality within the Universal Credit system.

2. Remove the savings rules in universal credit to allow more people to access it.

3. End the five week wait by converting emergency payment loans to grants. As there is usually a five-week wait for the first universal credit payment, emergency payment loans are available to those who are struggling. These loans, however, must be paid back from future payments. Repayment of these loan pushes already low benefits payments even lower. Any existing emergency payment loans should be converted to grants, and the advance payment system should now be used to make the first payment (as a grant) as soon as possible.

4. Raise the basic level of universal credit. In future, we would like to see a more earnings-based model, but this is too difficult to introduce swiftly. We therefore propose a higher rate, paid quicker, under the current system. £260 a week represents 80 per cent of the national living wage, or 47 per cent of total average weekly earnings, which we believe is a reasonable replacement rate. Even to restore the basic level to its pre 1980s replacement rates would require the current rate of £94 to be almost doubled to £165 a week. For existing claimants, payments can be topped up automatically, and the benefit cap should be lifted to account for this. While we propose £260, we do realise there are other suggestions out there, such as the NEF’s support for using the Minimum Income Standard of £221 per week[1] The JRF have called for the single person’s allowance to be raised to £150, at a cost of £5billion for three months. 3

5. Significantly increase Child Benefit payments. Child Benefit is the simplest, quickest and most effective way to get money to households with children. The level has long been too low. This payment would also recognise the additional costs many parents will face with having children at home because schools are closed.

6. Ensure nobody loses out as a result of these changes. As previously mentioned, the benefits cap should be lifted so that these increases do not just mean a change in the composition of the benefits someone receives. As well as this, no one on legacy benefits should lose the protection of the managed transition to UC as part of this change. 4

7. Remove the minimum hours requirements in working tax credits. Families still claiming tax credits must work a minimum number of hours to be eligible. This rule should be removed with immediate effect so workers who have had their hours cut as a result of this crisis do not lose out on their entitlement to tax credit payments as well.

While these emergency measures are temporary for however long coronavirus lasts, we do not expect a return to the current system after these measures end. Instead, this is the start of a wider conversation of how we reform universal credit: a policy that has persistently proved its critics correct and already pushed too many people into poverty and hardship.

A wider package of support for households

Alongside this, we reiterate our call for a wider support package that helps household finances, with a particular focus on reducing household costs.

We have called on government to create a coronavirus response taskforce, made up of unions, businesses and government agencies. We suggest the government consults this taskforce on the best way to get financial support to households.

Our suggested measures include:

- A fully funded council tax freeze, as well as council tax debt payments. This will provide financial relief for households, as well as guarantee councils still get the money from council tax. The freeze will also allow councils to use the hardship fund for more discretionary support, rather than council tax bill deductions

- The £500 million hardship fund must be substantially increased. The current level is insufficient and will need to be expanded in order to help everyone affected by coronavirus

- A package of support for renters.

- 1 Minimum income guarantee, NEF. Available at: https://neweconomics.org/uploads/files/MIG-new.pdf

- 2 JRF 26th March 2020 ‘Updated corona virus briefing: we need a lifeline to help people keep their heads above water’ https://www.jrf.org.uk/report/coronavirus-we-need-lifeline-help-people-keep-their-heads-above-water

- 3 See for example, EHRC (2018) ‘The cumulative impact of tax and welfare reforms’ available at https://www.equalityhumanrights.com/en/publication-download/cumulative-impact-tax-and-welfare-reforms

- 4 See DWP press release here: https://www.gov.uk/government/news/recovery-of-benefit-overpayment-suspended

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox