The fiscal cost of insecure work

The TUC brings together more than 5.5 million working people who belong to our 48 member unions. We support trade unions to grow and thrive, and we stand up for everyone who works for a living. Every day, we campaign for more and better jobs, and a more equal, more prosperous country.

The TUC is concerned about the prevalence of insecure work, most importantly because of the impact it has on workers. But it also has an impact on the economic stability of the country and on the public finances.

We have documented this in publications on the extent of insecure work, the increasingly abusive way employers use insecure contracts and the disproportionate concentration of Black and minority ethnic workers on zero hours contracts.1

There are 3.6 million people in various forms of insecure work, a figure that has remained stubbornly high since surging after the Great Financial Crisis.

The current government came to power in 2019 promising to make Britain “the best place in the world to work”.

Yet ministers have so far failed to deliver the employment bill that featured in the first post-election Queen’s Speech in 2019. This should be the vehicle for measures that would discourage employers from pursuing exploitative working arrangements and hand more power and security to working people.

One of the consequences of widespread insecure work, according to new figures produced for the TUC by Landman Economics, is to deny public services of tens of billions of pounds a year.

And the public finances remain hugely vulnerable to fluctuations in the numbers of those in insecure forms of work.

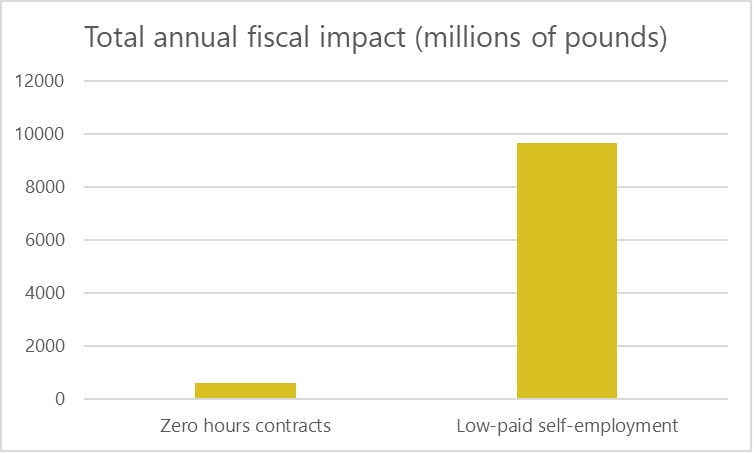

The analysis shows that the Treasury takes in around £10 billion less a year from those in low paid self-employment and on zero hours contracts than if they had been employed.

This is close to the £10.9 billion extra revenue that the government will take in in the current financial year by increasing National Insurance bills.2 It is also similar to the £11.1 billion that the UK spends on overseas development aid and would amount to 38 per cent of England’s adult social care budget.3

This reduction is due to a combination of lower earnings, different taxes and higher social security payments.

On top of this, our analysis shows that public finances are hugely sensitive to changes in the number of those in insecure work.

The need for urgent action to support decent jobs has been thrown into stark relief by new figures showing that a 1 per cent rise in those in insecure work, in the form of low-paid self-employment and those on zero-hours contracts, as a proportion of the workforce could knock off nearly £1 billion (£940 million) off the public finances

This is enough to pay for 1,100 magnetic resonance imaging scanners or to educate nearly 150,000 English school children for a year.4

These two elements show how crucial it is that the government gets to grips with insecure work.

Over recent years there has been a consensus established that reform is needed. Key policies, such as legislating to give workers adequate notice of shifts and compensation for cancelled shifts, enjoy both employer and worker support.5

Yet, despite repeated promises, the government is expected not to include a long-awaited employment bill in next month’s Queen’s Speech.

- 1 TUC. July 2021. Jobs and recovery monitor – insecure work. TUC www.tuc.org.uk/research-analysis/reports/jobs-and-recovery-monitor-insecure-work; TUC and Race on the Agenda. June 2021. BME workers on zero hours contracts. TUC www.tuc.org.uk/research-analysis/reports/bme-workers-zero-hours-contrac…

- 2 Miller, H. 5 April 2022. “Three things to know about National Insurance contributions and the upcoming changes”. IFS https://ifs.org.uk/publications/15929

- 3Brien, P., Loft, P. 5 November 2021. “Reducing the UK’s aid spending in 2021”, House of Commons research briefing https://researchbriefings.files.parliament.uk/documents/CBP-9224/CBP-92…; Bottery, S., Jefferies, D. March 2022. Social care 360. Kings Fund www.kingsfund.org.uk/publications/social-care-360/expenditure

- 4 Sibieta, L. 21 October 2021. Comparisons of school spending per pupil across the UK. Institute for Fiscal Studies ifs.org.uk/publications/15764; Dunbar, J. 21 September 2016. “Is a hospital a useful unit of spending?”, BBC News website www.bbc.co.uk/news/magazine-37383918

- 5Sanderson, B. 17 December 2018. “Letter from Bryan Sanderson to the Secretary of State for BEIS, Department for Business, Energy and Industrial Strategy https://tinyurl.com/2p9b42kf

What is behind the fiscal impact of insecure work?

There are two components.

Firstly, there is an earnings penalty for insecure work. Self-employed workers and those on insecure contracts like zero-hours contracts earn considerably less than employees more generally.

This feeds through to the public finances because lower earnings mean that the government receives less in income tax and national insurance contributions. Also, workers on lower earnings receive more in social security payments.

Secondly, the treatment of self-employed workers for income tax and national insurance purposes means that a self-employed worker pays less tax than an employee on comparable earnings.

This analysis seeks to estimate the size of the fiscal gap that results from consistently high levels of insecure work. It therefore models what the impact on the public finances would be if zero-hours contract workers and those self-employed workers in the lowest two earnings quintiles were in conventional employed work. It also models the impact of a 1 per cent rise in the share of the workforce of those in insecure work.

Earnings penalty

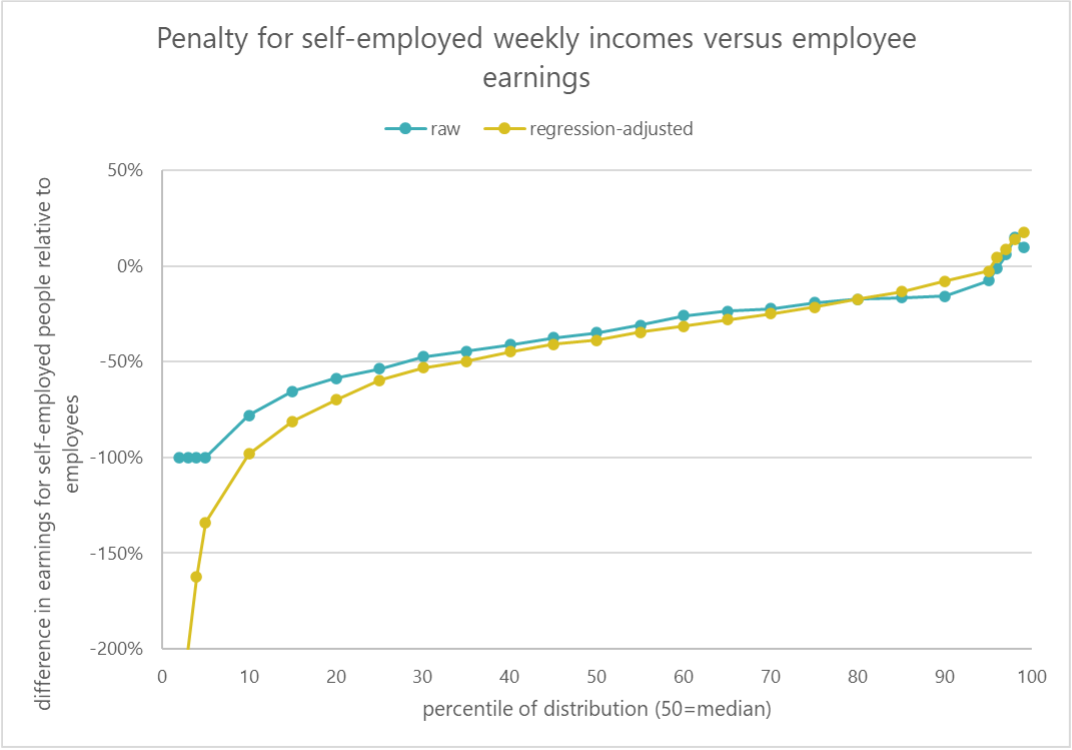

Analysis of official data shows that there is a heavy earnings penalty for those in insecure work across the distribution of weekly incomes from work. The only exceptions are the highest-earning self-employed workers.

At the median, which is the middle of the earning distribution, weekly earnings for those on zero-hours contracts is 59 per cent lower than for those not on such contracts. The median zero-hour contract workers is paid £200 a week, compared to £490. Across the whole distribution of earnings, the gap ranges from 70 per cent to 46 per cent and is particularly high for groups towards the lower end of the earnings distribution.

When controlling for factors such as age, gender, qualifications, occupation and industry, the median pay penalty falls to 6 per cent.

A similar picture is found for the self-employed. The median self-employed worker earns £300 a week. This is 35 per cent less than the £460 earned by the median employee. When controlling for factors such as age, gender, qualifications, occupation and industry, the median pay penalty for self-employed workers rises to 39 per cent.

This difference in earnings means that self-employed workers in the same earnings quintile contribute less in tax and national insurance payments. It also means that they receive more in social security payments.

Differences in taxation

The key difference in the way the government taxes employees and the self-employed relates to national insurance.

Employee earnings are subject to class 1 employee and employer national insurance contributions.

But self-employed workers are registered as sole traders pay class 4 national insurance contributions at a much lower rate.

Meanwhile those self-employed people who have set up their own company do not pay national insurance on dividends paid out of company profits.

Those dividends also face a lower rate of income tax. Over the personal allowance, the income tax rate on dividends is 8.75 per cent at the basic rate, 33.75 per cent at the higher rate and 39.35 per cent at the additional rate.

This compares to 20 per cent, 40 per cent and 45 per cent for those paying income tax on earnings.

Estimating the size of the fiscal gap

The size of the fiscal penalty due to insecure work has been estimated for the TUC using data from the UK Family Resources Survey and the Landman Economics tax-benefit model.

It looks at data from the second quarter of 2016 to the second quarter of 2021 and considers the distribution of the earnings of low-paid self-employed workers and those in zero-hours contracts.

It considers the extra tax receipts that would accrue to the Treasury, and the reduce social security expenditure, if that same distribution of workers was in employed work.

Results

1. The annual gap

The analysis shows that the Treasury takes in around £10 billion less a year from those in low paid self-employment and on zero-hours contracts than if they had been employed on conventional contracts.

This is because those self-employed in the bottom two quintiles are contributing £9.7 billion less a year to public funds than if they had been in employment.

The majority of this gap (£5.1 billion) is accounted for by lower receipts of national insurance. But the Treasury also receives £3.2 billion less in income tax. And low-paid self-employed workers receive £1.3 billion more in universal credit and other benefits than their equivalents in employment.

These calculations assume that such workers are operating as sole traders. The impact would be even higher if they were operating through their own company.

For those on zero-hours contracts, the fiscal gap is £614 million. Around 69 per cent of this is due to the Treasury receiving less in income tax and national insurance. The rest is accounted for by higher universal credit and legacy benefit payments.

This is money that is not available to spend on important public services such as schools, hospitals and social care.

2. The sensitivity of the public finances to insecure work

We have also calculated the fiscal impacts per percentage point of self-employed and zero-hours contract workers in the working population.

This gives a sense of how vulnerable the public finances are to rises in insecure work.

This shows that for a percentage point rise in low-paid self-employment and zero-hours contract work as a share of the workforce, nearly £1 billion (£940 million) would be denied to public services thanks to the impact of low pay and differences in taxation treatment.

Around £720 million of this would be accounted for by the effect of low-paid self-employed. Zero-hours contracts would knock the remaining £220 million off public finances.

Insecure work isn't voluntary

This shouldn’t be dismissed as the effect of people taking on the forms of work that best suit their lifestyles.

The case is often made that many people prefer casual contracts. Sometimes it is argued that this gives workers the flexibility to balance their work and other responsibilities.

But polling conducted for the TUC among those shows that for most zero-hours contract workers this flexibility is purely theoretical. It tells us that:

- employers are increasingly scheduling and cancelling shifts at the last minute, with 84 per cent of zero-hours contract workers offered work at less than a day’s notice

- the main reason workers take on zero-hours work is because it is the only work available

- insecure work is pushing risk onto workers: more than half of insecure workers, including three quarters of people on ZHCs had their hours cut due to the pandemic.6

Self-employment can be a valuable and productive form of work. Millions of union members work as actors, musicians, technicians, tour guides and in other occupations in legitimate self-employment. But in recent years, employers have also sought to use false self-employment as a way to reduce their responsibilities – both to the exchequer and to workers. Much of this work is low paid – and previous work has estimated that nearly half (47.7 per cent) of the self-employed are paid below the minimum wage. While not all of the low-paid self-employed will be in false self-employment, many of them will not be there by choice.

Conclusion

Insecure work doesn’t only disadvantage those directly subject to it, it drains the public finances of important funds.

This is due to a combination of low wages, and the structure of the taxation system. The former is by far the most important element.

Previous analysis by the TUC7 has shown that only a small proportion of the fiscal gap would be closed if there was reform of the tax system to align more closely the treatment of self-employed and employed workers.

Repeated governments have promised action from Theresa May’s commissioning of the Taylor Review to Boris Johnson’s promise to make Britain the best place in the world to work.

This report shows how important action is for the public finances. Including an employment bill in the Queen’s Speech would be a start. The Bill must include:

- a ban on zero hours contracts through a right to a normal-hours contract and robust rules governing adequate notice of shifts and compensation for cancelled shifts

- an entitlement for all workers, including agency workers, zero-hours contract workers and casual workers, to the same floor of rights currently enjoyed by employees

- a statutory presumption that all individuals will qualify for employment rights unless the employer can demonstrate they are genuinely self-employed

- penalties for employers who mislead staff about their employment status.

Methodological note

The size of the fiscal penalty due to insecure work has been estimated for the TUC by Landman Economics using data from the UK Family Resources Survey and the Landman Economics tax-benefit model.

The Landman Economics analysis uses data from the second quarter of 2016 to the second quarter of 2021 and considers the distribution of the earnings of low-paid self-employed workers (those in the bottom 40% of the earnings distribution) and those on zero-hours contracts.

Rather than just modelling the impact of an increase in self-employment at the average (mean or median) self-employed incomes and ZHC earnings, the methodology used here takes account of the distribution of earnings of the self-employed and ZHC workers. The earnings penalty for low-paid self-employed workers and employees on ZHC contracts is estimated at each point of the distribution, controlling for a range of employee and job characteristics including gender, age, age of youngest child (interacted with gender of the worker), ethnicity, region, qualifications, occupation and industry.

The model estimates considers the extra income tax receipts and National Insurance Contributions that would accrue to the Treasury, and the reduced social security expenditure, if the workers in low-paid self-employment or on ZHCs were instead employees on permanent contracts.

- 6See TUC 2021

- 7Landman, H. 2017. The impact of increased self-employment and insecure work on the public finances, TUC www.tuc.org.uk/research-analysis/reports/impact-increased-self-employme…;

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox