Workplace pensions: coverage rises but system still not fixed

Nearly three in four employees are now in a pension scheme, just five years after we reached a record low of less than half.

This is a rare story of public policy success that has survived changes of government and the financial crisis.

But under the headline statistics there remains an enduring story of pensions haves and have-nots.

Some 73 per cent of employees were in a workplace pension scheme in 2017, according to the Annual Survey of Hours and Earnings data published today. This is a dramatic turnaround from 2012 when membership of workplace pension schemes had dropped to 46%.

The difference has been made by automatic enrolment. Rolled out since 2012, this requires a worker to actively opt out of saving in a workplace scheme, and obliges their employer to put some money in.

It has had the most dramatic impact in the private sector. Back in 2012, fewer than one in three (32 per cent) private sector employees was building retirement savings. Now two in three (67 per cent) are.

This narrows the gap with the public sector where 89 per cent of employees are in a workplace scheme.

But we should still be worried about those slipping through the net.

The vast majority of low earners working for the private sector are not building up savings for old age. Just 27 per cent of private sector employees earning between £100 and £200 a week is building up savings. This compares to 81 per cent in the public sector.

The problem is caused by the so-called earnings trigger that means that someone only has to be automatically enrolled when they earn more than £10,000 from a single job.

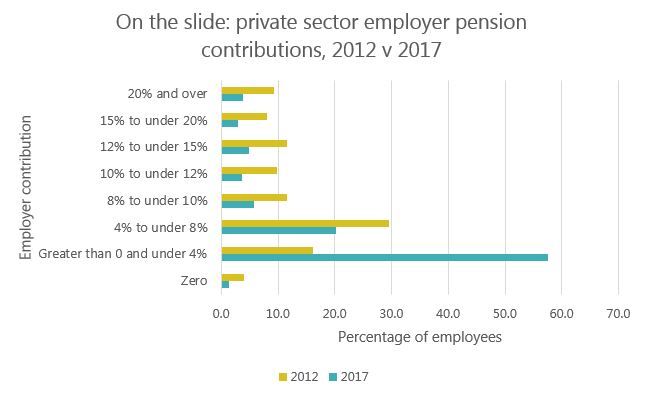

Official figures also suggest strongly that huge numbers of employers are putting in the minimum pension contributions required by law.

Some 57.6 per cent of employees in the private sector are having the equivalent of less than four per cent of salary contributed to their pension savings by their employer.

Around two-thirds (65.6 per cent) of employees are putting in more than zero but less than four per cent.

This is well below the amounts that will allow their employees a reasonable standard of living in old age.

Most estimates suggest something between 12 per cent and 16 per cent of wages need to be saved for a reasonable retirement.

Automatic enrolment will today quite rightly be hailed as a success.

Whether it is seen as such in 30 years will depend on whether today’s workers reach retirement with workplace pensions that will give them a reasonable standard of living.

Unless urgent action is taken to bring more low earners into the pensions system and ensure those who are auto-enrolled are building enough savings, this will not be the case.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox