Why we shouldn’t be worried about inflation right now

At the moment we fear for the livelihoods of the 800,000 employees who have lost work since the start of the pandemic. We fear that too many of the 3.4 million on furlough will not find an easy passage back to work. We fear for the victims of fire and rehire. We fear for those whose unjustly low living standards have been exposed by the pandemic.

That’s why the talk of ‘runaway’ inflation right now should be taken with a pinch of salt. Fears of inflation mustn’t be used to stop government taking action to support the economy.

Who’s talking about inflation?

The message of the so called ‘inflation hawks’ is that we need to act now on inflation to prevent it getting worse. As always in situations when the facts are less clear cut, the rhetoric gets out of hand. So prominent among today’s hawks, the departing Bank of England Chief Economist Andy Haldane deployed a vivid metaphor owed to a hard-right economist:

"Friedrich [von] Hayek once referred to inflation as the tiger whose tail central banks hold, usually with trepidation and ideally from a safe distance. If central bankers wait to see the whites of this tiger’s eyes before acting, they risk having to run like the wind to avoid being eaten."

While Andy Haldane, and others talking about inflation are quick to point out they know it’s not the 1970s, they can’t help referring to it. But as we set out here, it’s really not the 1970s:

- the inflation story doesn’t add up after oil is taken into account

- repeated mis-readings of the economy have led to phantom inflation scares

- labour market conditions have long stood in the way of decent pay

The danger of all this hysteria is to detract attention from the possibilities of building back better, and from the necessity of continued government support for the economy and jobs way beyond the end of lockdown.

1. The inflation story doesn’t add up after oil is taken into account

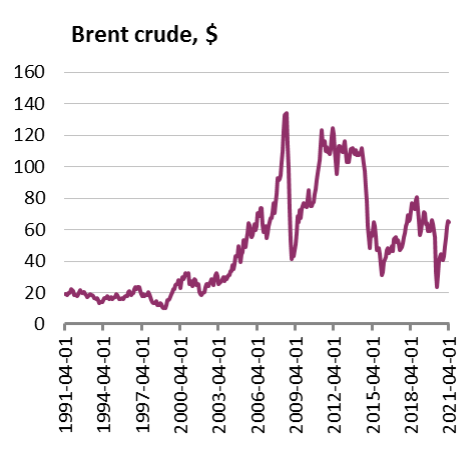

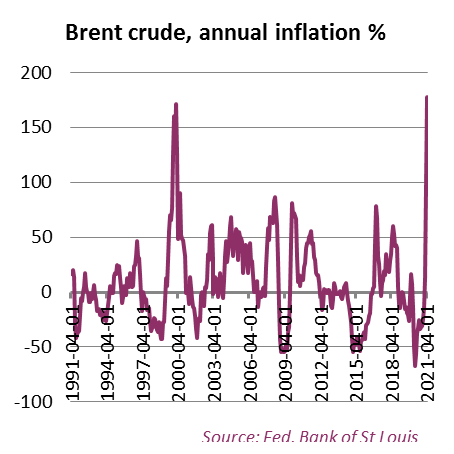

It is no coincidence that the inflation hysteria reached a crescendo following the April inflation figures. April last year was the start of the global lockdown, and Brent crude (i.e. the global oil price) hit its lowest for nearly 20 years (since Feb 2002). Since then the oil price has come back into line with outcomes ahead of the pandemic (top chart below).

In fact the annual increase of the price of Brent crude into April 2021 was the highest for 40 years (bottom chart), not because the price is now high but because it was very low last year.

.

.

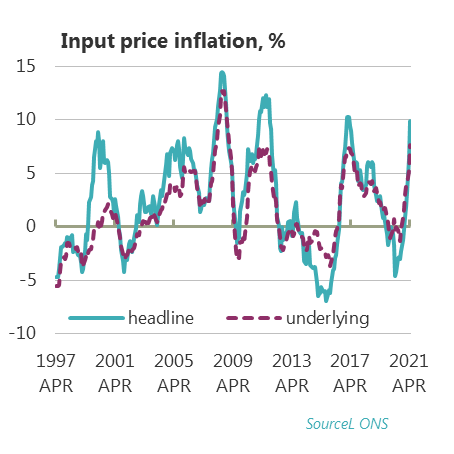

Brent crude inflation works into national economies via the factory gate and petrol pump.

In the UK we see the former via producer price inflation. On input prices (top chart below), headline inflation of 15% is marginally lower than the three previous peaks since the global financial crisis (GFC). Underlying input price inflation (excluding the purchases of food, beverages, tobacco and petroleum industries) of 7.6% is pretty much exactly in line with the two previous peaks.

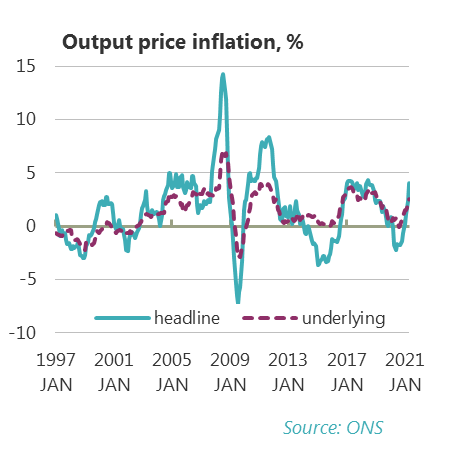

Then on output price inflation the headline figure of 4% is around the level of the previous peak and well below the other two peaks since the GFC. The underlying output price figure of 2.5% is well below even the most recent peak of 3%.

Beyond putting into perspective this latest peak is the more fundamental point that each of these previous three episodes of increased inflation’ since the GFC have been incredibly short lived (even following the EU referendum induced sterling devaluation).

.

.

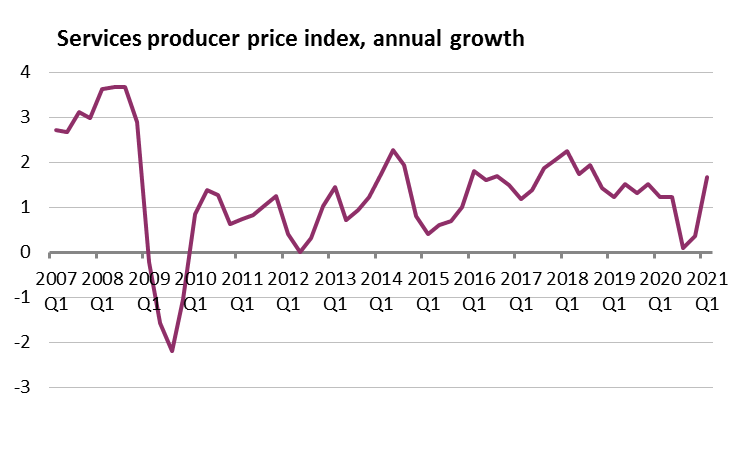

Given the small size of manufacturing in the UK, producer prices are perhaps less significant than service producer prices. Here again there is nothing remarkable to report, with the services producer price index (SPPI) in Q1 (the data are quarterly) returning to just above where it was a year ago (1.7% in latest v 1.5% in 2019Q4). Again the present peak is below the previous three peaks since the GFC.

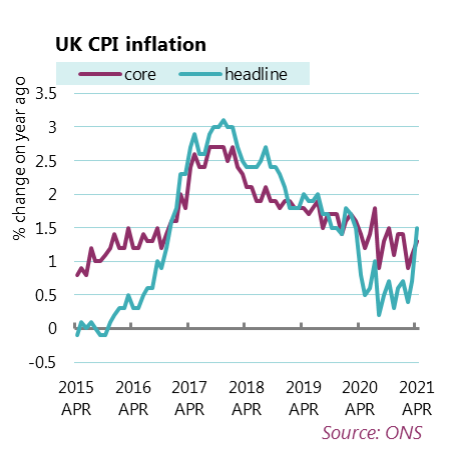

Central banks of course target CPI inflation not producer price inflation, and here the core measure – excluding food, alcohol, tobacco and energy - tells the real story.

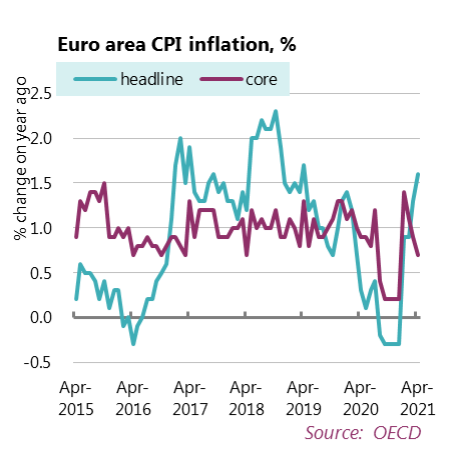

In the UK while the headline measure jumped to 1.5% in April, the core measure of 1.3% was exactly in line with outcomes over the past year (top chart). In the euro area, core inflation actually fell (bottom chart) and stands at only 0.7%.

.

.

2. Repeated inflation scares

The charts above show all episodes of (marginally) increased inflation since the GFC proving incredibly short lived.

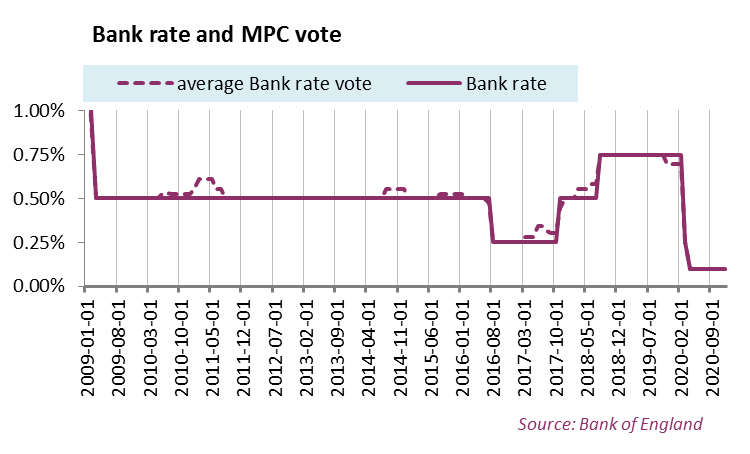

But repeated inflation scares have been characteristic of the post-crash economic discourse. To illustrate, the chart below shows the average Monetary Policy Committee vote (in dotted) against the actual rate of interest. So little bumps reflect when some members start calling for rate rises, but rates only change when the solid line moves.

Ahead of the temporary rate reduction around Brexit, there were three occasions when the hawks bared their claws. In 2010 – at the start of austerity – Andrew Sentence led the way to be joined by Martin Weale and then Bank of England chief economist Spencer Dale. A year later they had all backed down as austerity plunged the euro zone into crisis. In 2014 Weale had another go, to be joined by new member McCafferty, but backed down when global deflation loomed (!). McCaffery briefly went solo in 2015.

Finally after the emergency Brexit policy ended, the hawks got their way and rates rose to 0.75%. But even then policy was on the verge of being reversed before the pandemic hit – committee member Saunders had voted for a cut at the end of 2019 in parallel to decisive cuts in the US from 2.5 to 1.75 over the second half of 2019.

Repeated fears of inflationary pressures come in my view from misreading economic conditions.

The Bank and Treasury insist that the crisis was caused by the public living beyond the means of the economy. Instead the economy has been operating beyond the means of the public.

The crisis was caused at global level by purchasing power falling way too far short of production (see here for fuller account). Actions since then have served to intensify not resolve this situation. Rather than inflation, the constant threat is from private debt (which results from company sales falling short of expectations and households borrowing to say afloat). These are not conditions when higher inflation can be sustained, as Sentence, Weale, McCafferty and Dale have discovered.

3. Labour market conditions have long stood in the way of decent pay

The bottlenecks in recruitment – apparently in agriculture, hotels and restaurants, transport/distribution – that are so prominent in the headlines tell us more about the economy pre-pandemic than they do about the prospects for pay rises in the future.

The pandemic came on the back of the longest period of real wage stagnation for 200 years, and a sharp rise in insecure work. A rise in pay and conditions is long overdue but by no means secure. There are still 3.4 million people on furlough, and employee jobs are down 800,000 - it’s hard to argue that we’re suffering a labour shortage that will lead to an automatic rise in pay and conditions without government action.

Martin Sandbu on FT Alphaville cautions against emphasis on “what is unusual rather than what is representative”. Less widely reported are fire and rehire policies for example at Weetabix and British Gas, with industries taking advantage of the pandemic to undermine pay and conditions.

To add insult to injury the government is operating to make union organising that might strengthen the position of workers more difficult, has signed trade deals likely to put additional pressure on workers, and has of course again delayed the long awaited employment bill that might have protected workers.

Rather than focusing on unfounded fears of inflation, government should be thinking about how to get workers the pay rise and secure jobs they so richly deserve.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox