It’s still too early to raise interest rates - here's why

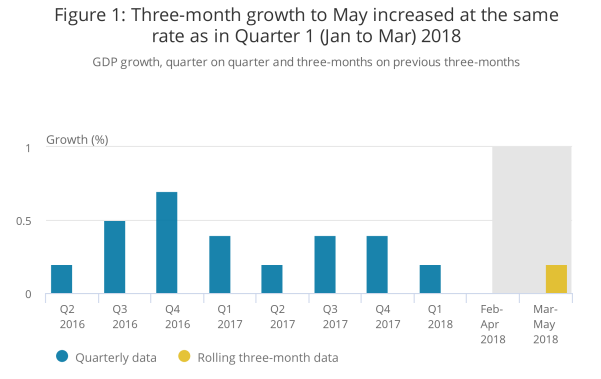

The new monthly estimate of GDP figures published by the ONS today shows “rolling three-month” growth standing at 0.2 per cent from March to May.

At face value this is a near stagnant growth rate – as the headline on the ONS chart puts it, it’s the same rate as quarter one:

New measure, old story

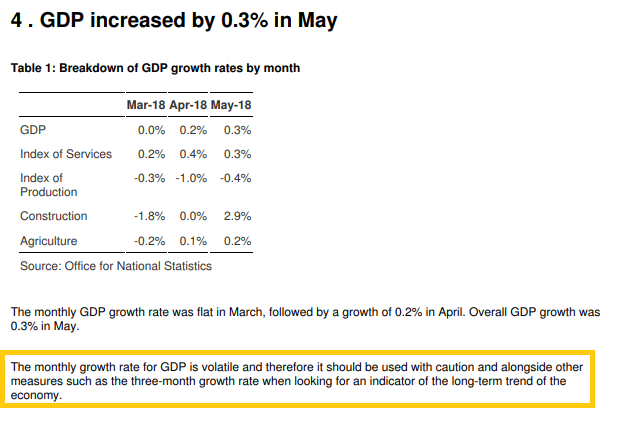

This month the ONS has changed the way that it measures GDP.

So today’s release compares the latest three months with the previous three months, rather than the standard quarterly measure.

On this basis GDP rose by 0.3 per cent into May, following a rise of 0.2 per cent into April.

The new measure means we can chart the evolution of GDP growth more often, but there’s also likely to be more focus on individual monthly figures instead of the rolling three-month average.

The ONS commentary includes a small table and offers only a few sentences on the new measure (including the health warning we’ve highlighted below).

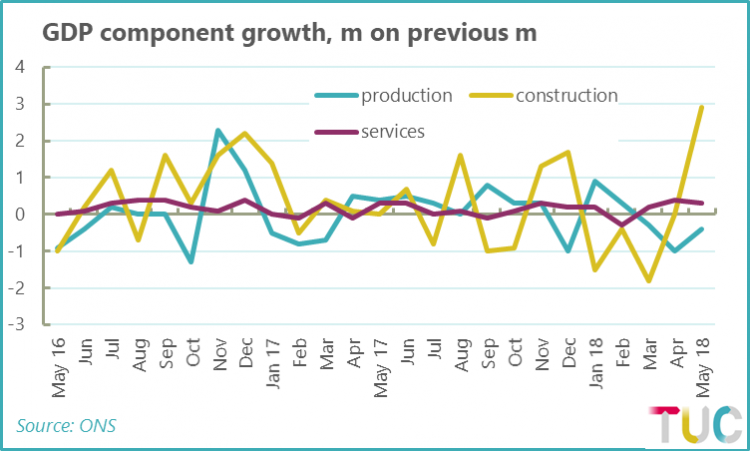

The ONS is right to urge caution, since most of the GDP increase over the last three months is down to a massive surge in construction output (as well as a reduced decline in production).

Here are the month-on-month growth rates, showing construction in all its implausible glory:

Let's not forget that the quarter one estimate of GDP growth was revised up from 0.1 per cent to 0.2 per cent largely because of revisions caused by problems with the construction figure.

On this basis it’s hard to take the latest monthly movement completely seriously, despite claims of “improvements”.

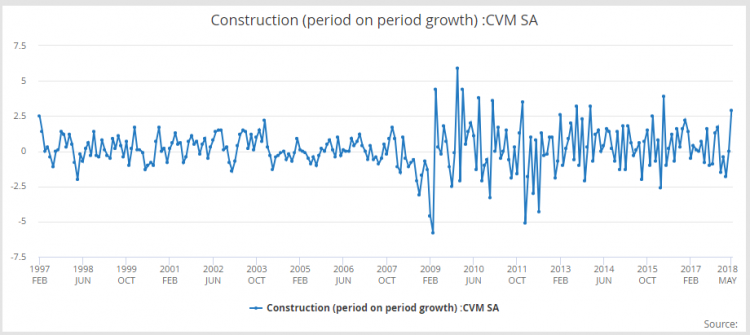

A longer overview of the noise that pollutes the monthly construction data is very telling:

The problem is that monthly measures are subject to erratic volatility that is often meaningless to understanding the underlying picture.

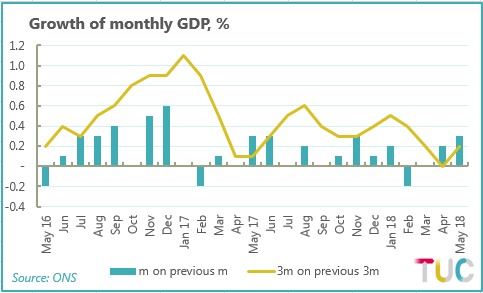

Take a look at this chart showing monthly growths and the rolling three-monthly growth figure for GDP:

It shows that two consecutive positive months don’t always mean underlying strength. Notably May and June 2017 came to nothing, while November and December 2016 marked the end of an expansion.

The ONS has always been able to calculate some kind of monthly measure of GDP because the output measure is based on monthly sources and monthly indices in their own right (index of production, index of services etc).

But up until now they have resisted this temptation.

On the one hand, the change means that we will now have to wait until 10 August for the first full estimate of GDP for the second quarter, which is a couple of weeks later than under the previous arrangements.

On the other, this estimate will include expenditure and income information sooner than previously.

So the fair thing to do is to reserve judgement about whether the new measure is clearer or not.

Too soon for a rate rise

These changes have been introduced at a time when the Bank of England has an itchy trigger finger on interest rates.

Yet we’re clear that the case against raising rates is still strong.

Growth was always likely to improve from the dismal Q1 figure, and it’s hard to see any underlying strength in the latest figures.

Meanwhile, wage inflation is faltering, underlying price inflation is weaker than expected and yesterday’s BCC business survey showed reduced price pressures.

In short, there remains no justification for pulling that trigger any time soon.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox